Taxation of life insurance business

2009 legislation introduces rules to deal with the taxation of life insurance business in connection with term life insurance and savings-related life policies.

Sections CR 1, CR 2, CW 59C, CX 55, DR 1 to DR 4, subpart EY, sections EZ 53 to EZ 63, IA 8, subpart IT, sections LA 8B, LE 2B, sections OC 2B, OC 20, OP 7(3), OP 17, OP 30(2), OP 33B, OP 44, OP 74 and section YA 1 of the Income Tax Act 2007

Significant changes have been made to the taxation of life insurance business. The changes update the rules to ensure that term insurance business is taxed on actual profits, as other businesses are taxed, and extend the tax benefits of the PIE rules to people who save through life products. The new rules tax life insurance business like other New Zealand companies but require separate calculations to reflect two bases of taxable income:

- a shareholder base (representing income derived for the benefit of shareholders); and

- a policyholder base (representing income derived for the benefit of policyholders).

Income and deductions will be recognised using ordinary tax principles, with the addition of special rules to deal with the unique timing and allocation issues inherent with life insurance products, particularly in respect of participating life policies.

Life insurer income will therefore be allocated between income earned on behalf of shareholders (the shareholder base) and income earned on behalf of policyholders (the policyholder base).

The shareholder base comprises the following items: risk profits, fees, share of participating profits, investment income on shareholder funds, and other income accruing to the life company, less allowable deductions. It will be taxed at the company rate, and be generally subject to ordinary rules for companies, including those for losses, continuity based on shareholding and memorandum account balances.

The policyholder base comprises investment income (less expenses) from policyholder funds, including the policyholders’ share of net investment income from participating policies (allocated to policyholders in reflection of their contractual entitlements). Excess deductions and surplus imputation credits converted to deductions are carried forward for deduction in next year’s policyholder base with no requirement to meet a continuity of ownership test.

The portfolio investment entity (PIE) exclusion for realised New Zealand and listed Australian equity gains has also been extended to policyholders in all life insurance savings products, which will then be taxed at the company rate of 30%. Life insurers can elect to attribute income in investment-linked products to each policyholder at their portfolio investment rate (19.5% or 30%).

The new rules also provide a transition period and rules for life insurance policies sold before the application date of the new rules.

Background

The new rules solve several problems that existed with the taxation of life insurance business in connection with term life insurance and savings-related life policies.

Taxing income from term life insurance business

Life insurance companies are companies that carry on a life insurance business and are registered under the Life Insurance Act 1908 to write life insurance policies.

Until the 1980s, the products most frequently offered by life insurance companies were the traditional whole of life and endowment products.1Since the enactment of the previous life insurance rules, term life insurance business has increased from being less than 10 percent of total industry premiums to now over 50 percent. Term life insurance is a pure risk product that pays out only on death (within the term of the policy). Term insurance policies do not contain a savings component in the premium which means they have more in common with general insurance (such as motor vehicle or home and contents insurance) than traditional savings-related policies.

The main problem with the previous rules is that calculation of taxable income was based on a formula that was not designed with term insurance products in mind. This formula has little connection with the profit earned from term insurance. The tax result under the previous rules is illustrated in Example 1.

Example 1: The problem with taxing term risk life policies under the previous rules

| Financial accounting | Under the previous rules | |

|---|---|---|

| Premiums | 100 | |

| Claims ( = Expected claims) | (45) | 0 |

| Investment income | 10 | 10 |

| Expenses | (40) | (40) |

| Premium loading (20% claims) | 9 | |

| Accounting profit/tax (loss) | 25 | (21) |

As shown in the example, if the life insurer has a loss ratio (claims ÷ premiums) of 45 percent, a $25 accounting profit translates into a $21 tax loss. In effect, life insurers were not being taxed on the profit they make on term life risk business, generating losses that may have reduced overall tax paid.

Savings

Under the previous rules, individuals who saved through life insurance products faced a higher tax burden than other savers who invested directly or through managed funds that become PIEs. This effect served to distort consumer decisions about the type of saving vehicle used and placed life insurance polices at a competitive disadvantage.

Other

There were a number of other issues, such as measuring continuity and use of conduit rules, caused by the imperfect measurement of ownership that did not recognise the policyholder base as an "owner." This is because the life insurer was taxed on all its income, policyholder and shareholder together. This meant that concessions that were aimed at non-resident shareholders of a company, such as the tax relief under the conduit rules, were also provided to the resident policyholders.

Key features

Under the new rules, the shareholder base consists of:

- profits from the risk component of premiums less risk claims net of reinsurance;

- net investment income from shareholder funds;

- shareholder share of participating policy profits;

- fees from investment management and other services;

- income from annuities;

- income determined under ordinary principles from any other sources;

- less risk expenses and any other allowable deductions; and

- plus/less changes in risk reserves.

Ordinary provisions apply to shareholder base losses carried forward or subject to grouping, and to imputation credit and other remaining memorandum account balances carried forward.

The policyholder base consists of:

- net investment income from policyholder funds; and

- policyholder share of investment income (less expenses) from participating policies.

The shareholder base is taxed at the prevailing company rate. The policyholder base is ordinarily taxed at 30%, although life insurers may elect to attribute investment income from investment-linked products to each policyholder at their portfolio investment rate.

Any policyholder base loss is carried forward to the next income year. Excess imputation credits on the policyholder base income are grossed-up and applied as a loss against the policyholder base in the subsequent income year. In both cases there are no continuity requirements.

Sections EY 17, 18, 21, 22, 28 and 29 contain detailed rules on the allocation of income and expenditure or loss from profit-participation policies between the shareholder base and policyholder base.

In situations when the operation of new rules, particularly in subpart EY, gives rise to income or expenditure that would not be recognised by ordinary taxation principles, new sections CR 1, CR 2, DR 1, DR 2 and DR 4 ensure that the calculation of income and expenditure is consistent with the core principles of the Income Tax Act 2007.

Application date

The new rules apply from 1 July 2010. This date applies to the changes to the taxation of life insurance business and the application of the PIE taxation rules to all policyholder savings policies. The five-year grandparenting period also starts from that date.

To provide some flexibility, life insurers have the option to apply the new rules from the beginning of their income year if that year includes 1 July 2010.

When the application date bisects an insurer’s tax year, the insurer is required to complete a separate calculation for the period before the specified date and another for the period after.

Detailed analysis

The analysis of the new life insurance rules is in two parts. The first part deals with the operation of the new rules after the application date. The second part deals with the transitional rules and the effect of the grandparenting provisions.

Part I: The new rules

Scheme and operation of the new rules

The taxation base for life insurance business consists of the following elements:

- Shareholder base income, less allowable deductions, under the new life rules

- Other income (including general insurance) less allowable deductions

- Schedular policyholder base income, under the new life rules

- Life fund PIE income, less allowable deductions, attributed to each policyholder at their portfolio investment rate.

The recognition of income and expenditure under the Income Tax Act 2007 relies in the first instance on amounts that result from using generally accepted accounting practices. These amounts are then modified according to ordinary income tax principles to determine whether an asset is held on revenue account by the life insurer and whether any expenditure incurred is deductible. These amounts are then allocated under subpart EY to the two tax bases using formulas that are consistent with actuarial principles.

Section EY 1 sets out the core operation of the rules in subpart EY and provides for the taxation of life insurers on two separate bases. Sections EY 2 and EY 3 describe the general apportionment of income and deductions between the two bases. Section LA 8B provides some general rules for tax credits relating to the two bases. Parts L and O include tax credit rules and memorandum account rules specific to the two bases.

Section EY 1(3) prevents double counting of income or expenditure between the shareholder base and the policyholder base.

The shareholder base

Sections CR 2, CX 55, DR 1 to DR 4, subpart EY and section YA 1

The shareholder base comprises the following:

Risk income: The life risk components of life insurance products (excluding participating policies and annuities) will be taxed on the basis of their profits; being the difference between premiums less claims and expenses, including adjustments for certain reinsurance treaties. Reinsurance risk premiums paid and risk reinsurance claims received will be netted against such premiums and claims respectively, provided the reinsurance contracts were offered or entered into in New Zealand. Net risk income is adjusted for prescribed reserves (sections EY 23 to EY 27).

Fees: Fees and commissions from investment management or managing life insurance policies are treated as taxable income, whether explicitly charged or implicitly included in premium income (to the extent that the fees are not already included as risk income). Expenses incurred in deriving fee income are deductible.

Share of participating profits: The net return from participating policies is shared between shareholders and policyholders. Because of the complicated nature of these products, the allocation method is discussed under the heading "Participating policies".

Investment income: Amounts derived from investment income (less expenses) by the life insurer that has not already been included in the policyholder base becomes shareholder investment income. Sections EY 46 and EY 47 dealing with disposal of property have been repealed. One consequence is that the deeming of income arising from the disposal of property (other than financial arrangements) of the life insurance business has been removed. This means that whether a disposal of property by the life insurer is on revenue or capital account will have to be considered for particular taxpayers or circumstances under ordinary tax principles as amended by statutory provisions. The taxation of gains from the realisation of Australasian equities will be similarly treated.

Income earned from annuities: Net annuity income will continue to be determined using the old rules. Annuity premiums and claims are excluded from the shareholder base and annuity income is taxed using the formula in section EY 31(2). The terms of the formula are defined in sections EZ 53 to EZ 60. A positive amount is shareholder base income and a negative amount is a shareholder base allowable deduction. Net investment income arising from annuity is taxed in the shareholder base at 30%.

Deductions: The following deductions are allowed:

- Deductions will be generally allowed for expenditure or loss incurred for the cost of revenue account property in section DB 23. These deductions may have to be apportioned between the shareholder or policyholder base.

- Deferred acquisition costs, which are expenses connected with the sale of life policies – for example, commissions, will continue to be deductible under ordinary principles.

- Section DR 4 allows a deduction for the amount of expenditure or loss of a claim paid under a life insurance policy, or as an outstanding claims reserving amount under section EY 24.

- Deductions are also available for "premium payback amounts". Therefore, when an amount of life risk component premium is refunded in accordance with the terms and conditions of the relevant life insurance policy (or the discretion of the life insurer) that amount is deductible. The deduction is limited to premium payback amounts made at the end of the contracted policy term when those premiums have been previously returned as income under section EY 19(1) – subject to any transitional adjustments.

Other income and expenses: Other income and expenses determined under ordinary tax concepts are included.

Shareholder adjustment for reserves relating to non-participating policies – excluding annuities

Sections EY 23 to EY 27 and section YA 1

To reflect the unusual cashflows connected with certain life products, for example, premiums received upfront with large claim payments occurring later, life insurers use reserving methods to match revenue and expense recognition and to smooth profits.

New section EY 23 sets out the tax effects these reserves have on income and deductions relating to non-participating life products that are term insurance or savings products (that is, excluding profit-participation policies and annuities). Positive amounts are included as shareholder base income, while negative amounts constitute a deduction to the shareholder base. In other words, the movement in a reserve during the income year is; income if the reserve has decreased in value, a deduction if the reserve has increased in value.

Amounts calculated for the reserves must be actuarially determined for each class of policy. The rules relate to the calculation of reserves relating to premium income recognition, outstanding claims reserves, and capital guarantee reserves.

Premium income recognition - the unearned premium reserve and premium smoothing reserve sections - sections EY 25 and EY 26

For non-participating policies other than annuities, life insurers have the option of recognising premium income on an unearned premium reserve (UPR) basis or using a premium smoothing reserve (PSR) basis. The default option is the UPR. The choice of reserving method, once applied to a class of policies, is irrevocable - section EY 23(5) - except when the PSR can no longer be used, in which case the insurer reverts to the UPR method.

The PSR can only be used for:

- products which have premiums that are level (or substantially level for more than one year); or

- products which could result in a material mismatch in any one year between the incidence of life risk components and the timing of the premium payable, and the period is one or more years.

Life insurance policies may be grouped together under the PSR if the policies have the following in common:

- substantially the same contractual terms and conditions, other than the duration of the life insurance contracts; and

- substantially the same assumptions for pricing their life risk.

Unearned premium reserve: The UPR, calculated at the end of the current year under section EY 26, is based on the amount of premiums received in the current year (or an earlier year) net of related New Zealand-sourced reinsurance premiums paid that relate to unexpired life risk components and relevant costs.

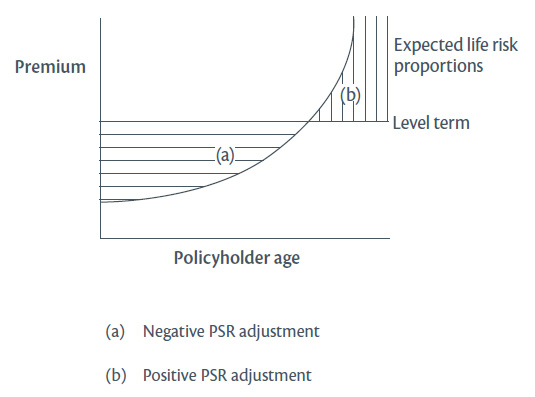

Premium smoothing reserve: The PSR in section EY 25 is designed to spread the recognition of premium income and tax over the duration of the level-term premium and single premium term policies. The PSR premium income should be calculated net of related New Zealand-sourced reinsurance premiums. The intent of the PSR is illustrated in diagram 1.

Diagram 1: Premium smoothing reserve

The line in Diagram 1 representing the 'expected life risk proportion", defined in section EY 25(6), represents the amount that would be the annual renewable term equivalent of the level term policy.

The "expected life risk proportion" could be determined using profit margins in a similar manner to a margin on services release of profits, or by reference to the probability of death in the year compared with the probability of death over the PSR period.

The outstanding claims reserve (OCR) – section EY 24

The OCR is a reserve held by an insurance company to provide for the future liability of claims which have occurred but which have not yet been reported to the insurance company or not yet been settled.

The new rules provide that life insurers are able to claim a deduction for movements in the OCR on life insurance policies, similar to the tax treatment to general insurers who sell general insurance policies.

One aspect of allowing the deduction is that the future claims (that is, claims recognised in the current accounting period that will be paid out in a future period) are discounted to their present value. The legislation (section YA 1) uses the term "present value (gross)" and means a present value calculation using the risk-free rate of return as the discount rate, gross of tax. If the whole discount period is less than a year the face value of the claim is used.

An appropriate risk margin is added to the estimated and actual values of life risk claims incurred and reported. However, where the amount of the claim is already known the appropriate risk margin would be zero.

The capital guarantee reserve – section EY 27

The capital guarantee reserve (CGR) applies to non-participating policies, excluding annuities, that have guarantees of capital invested or guarantees of minimum returns on capital invested. The reserve is the amount provided by the shareholder to top up the policyholder’s future claim under the guarantee.

If a policy has a guaranteed minimum return, the reserve will typically be drawn upon to "top up" the amount credited to policyholders in time of poor investment performance. In times of good investment performance, a portion of the investment return will typically be added to the reserve to support future crediting rates. The legislation provides that movements in the reserve result in shareholder base income if there is an increase in the reserve and a shareholder base allowable deduction if there is a decrease in the reserve. These adjustments are reflected in the policyholder base, whereby any amount of shareholder income becomes a deduction in the policyholder base and any amount of shareholder deduction is income in the policyholder base.

Shareholder injections to support the capital guarantee, while rare, will have a revenue character for the shareholder base. Such guarantees when paid by the shareholder may have a capital character for individual policyholders and are therefore not subject to tax in the policyholder base. To be consistent, the loss that caused the depletion of capital is not deductible in the policyholder base.

Movements in the CGR representing shareholder payments for products guaranteeing a minimum return (investment guarantee) that is in excess of zero percent on capital invested are properly treated as revenue amounts in both the shareholder base and policyholder base.

The policyholder base

Sections CR 1, CX 55, DB 23, DR 1, EY 1, EY 2, EY 4, and EY 15 to EY 18 and section YA 1

The policyholder base will consist of investment income earned on behalf of policyholders, less expenses. The amount of investment income allocated to policyholders from the total life insurer investment income is calculated under section EY 15 for non-participating policies (including annuities), less allowable deductions under section EY 16, and under section EY 17 for participating policies (discussed under the heading "Participating policies"), less allowable deductions under section EY 18.

Consistent with the operation of the portfolio investment entity (PIE) rules, changes to section CX 55 allow life insurers to exclude realised equity gains from New Zealand and listed Australian companies from tax on the policy holder base. The exclusion applies to the extent the amount is determined to be policyholder base income. A life insurer can also elect to register its fund of investment-linked products as a Life Fund PIE and attribute income to each policyholder at their portfolio investment rate; otherwise the income is taxed at 30%.

The policyholder base can carry forward unused tax deductions and these will not be subject to any continuity of shareholding rules. This is because the policyholder base is a proxy tax for each individual policyholder - thus changes of membership are not relevant. Surplus imputation credits can also be converted to deductions for the following income year. Policyholder net taxable investment income cannot be offset with losses or credits from the shareholder base, except in the case of transitional losses, which is discussed later in Part II of this item.

Non participating policies including annuities

Sections EY 2 to EY 4, EY 15, EY 16, EY 19, EY 20 and section YA 1

Section EY 15 prescribes the methods for determining what income is included in the policyholder base and provides bases of apportionment where investment income could be included in both the policyholder and shareholder bases. Section EY 16 contains mirror provisions for deductions to the policyholder base.

As a compliance simplification measure, when the life insurer has actuarially determined that the life risk is one percent or less of the premium or life reinsurance claim, it can choose to treat that amount as not relating to the life risk component, thereby including the entire premium effectively as the deposit of principal in respect of a policy (section EY 15(5)).

Allocation of investment income under the new rules

Investment income, and expenses and credits, have to be allocated to either the shareholder base or policyholder base, depending on whose benefit the investment income is derived. The new rules prescribe default methods of allocation, but allow the life insurer to use a different basis of apportionment if it is "actuarially determined" and is more equitable and reasonable. It is anticipated that many life insurers would apportion in a manner consistent with financial reporting where relevant.

The life insurer’s income from its life insurance business must be allocated to either the shareholder base or policyholder base. The allocation depends on whose benefit the income is derived. Section EY 1(2) provides that section EY 2 uses the taxable income in a life insurer’s policyholder base income and the life insurer’s policyholder base allowable deductions, to calculate its schedular policyholder base income. A life insurer’s schedular income derived by its life fund PIE is excluded from the schedular policyholder base income, along with deductions from that income.

Expenses allocated to life fund PIEs are recognised by section EY 2(6). These expenses are apportioned to the policyholder base, but excluded from schedular policyholder base income.

Section EY 4(1) provides a default basis of allocation for tax credits received. These amounts must be apportioned between the policyholder and shareholder bases in the same proportion as the policyholder base income. The same apportionment rules apply to shareholder base income. The section is intended to ensure imputation credits are allocated on actual policyholder base and shareholder base earnings.

The new rules also allow the life insurer to use a different basis of apportionment if it is "actuarially determined" and is more equitable and reasonable than the default basis.

Participating policies

Sections EY 17, EY 18, EY 21, EY 22, EY 28, EY 29 and YA 1

Specific rules deal with the treatment of income and expenditure arising from "profit participation policy" (as defined in section YA 1) business. A typical profit participation policy involves a group of members (policyholders) who pool their money together, generate income, self-insure (possibly with some outside reinsurance) and periodically formally increase their vested entitlement to the pool, usually by way of bonus allocations. Expenses associated with running the pool are met from within the pool.

"Profit participation policy" as defined:

- means a class of life insurance policy having

- a segregated or identifiable asset base; and

- policyholders who are entitled to a share of profits that is distributed to, or vested in, the policyholders from the asset base, and the policies provide for the entitlement; and

- a fixed formula, expressed in terms of a proportion of a policyholder’s share of profits from the asset base, that calculates a transfer to the benefit of the life insurer’s shareholders from the profits of the asset base, and that fixed formula is consistently applied:

- includes a class of life insurance policy that substantially meets the requirements of paragraph (a) and that has a guarantee by the life insurer that capital invested will be returned or that a minimum return on capital will be paid, if-

- the life insurer has irrevocably chosen that the class be treated as a profit participation policy; and

- the Commissioner receives a notice of the election before the start of the first income year to which it relates.

Paragraph (a) (iii) refers to what is commonly referred to as the "gate". The definition implies that shareholders obtain a positive profit from distributions. It therefore does not include life insurance policies such as investment-linked products, where the shareholder obtains no proportion of the policyholder’s share of profits from the asset base.

The basis for taxing participating policies comprises the following:

- Investment income less expenditure plus other profit

The new rules are designed to apportion net investment income between policyholders and shareholders in a way that recognises that part of the investment income is connected with policy liabilities (regarded as belonging to the policyholders) and part is connected with the existing surpluses (regarded as a source of future bonuses). Policyholders should, however, not be taxed on any other sources of gains when they are derived by policyholders trading among themselves. Therefore, any "Other Profit" is included in the shareholder base.

Premiums for traditional participating business are not treated as income under the new rules as these are, in substance, principal amounts invested. Similarly, claims paid under these products are not deductible. Premiums or life reinsurance claims that are incidental or minor, and included under the policyholder base under section EY 15(5), are not subject to tax under the shareholder base.

Treatment of income from disposal of investment shares - shareholder base

If income includes gains from realised Australasian equity the taxation of these gains, to the extent that they are allocated to the shareholder base, will be determined by ordinary tax principles.

Deductions and credits

The policyholder base (section EY 18) and shareholder base (section EY 22) have allowable deductions for profit participation polices equal to what they would have had under the income allocation formulas if:

- the life insurer is treated as having no assets other than the asset base; and

- item asset base gross income is treated as being the annual total deduction for the policies’ asset base.

Imputation and other credits will be apportioned between the shareholder and policyholder bases using the same ratio.

Taxation of participating policies sold before 30 June 2009 – separate rules

For policies sold before 30 June 2009, the date the bill was reported back to Parliament by the Finance and Expenditure Committee, life insurers are taxed using a simplified formula:

- Investment income less Expenditure

This change was made at the recommendation of the Finance and Expenditure Committee as a means of simplifying the application of the rules to existing participating policies (including policies sold after 30 June 2009) as a result of conversion rights (for example, whole of life policies converting to endowment policies). The more complex formula which takes into account Other Profit for policies sold on and after 1 July 2009 is intended to protect against any potential manipulation of taxable income associated with future participating life contracts.

Actuarial advice and guidance, "actuarially determined" and "best estimate assumptions"

Sections EY 6 and YA 1

Some of the calculations and apportionment of amounts required by subpart EY, particularly in connection with reserves, uses actuarial determinations and judgement. The term "actuarially determined" is defined in section YA 1.

A new definition of "best estimate assumptions" has also been inserted to provide that these judgements are consistent with professional actuarial judgement and that the assumptions underlying these judgements are not deliberately overstated or understated.

Section EY 6 allows Inland Revenue to seek the advice of the Financial Markets Authority or any other actuary on matters that are required to be actuarially determined under the new rules.

There is no requirement for sign-off from actuaries under the new rules. However, all working papers, methodologies and related documentation may be asked for by the Commissioner under the general powers already contained in the Tax Administration Act 1994.

Reinsurance

Sections CW 59C, DR 3, EY 5(8) and EY 12

The definition of "life insurance" includes reinsurance (section EY 14(3)) unless the context requires otherwise. Therefore, all the new rules dealing with life insurance generally also apply to life reinsurance.

There are, however, specific references to life reinsurance when calculating deductions under the shareholder base from insurance premiums and claims, in calculating reserving amounts, and under the policyholder base for profit participation. Section EY 12 defines "life reinsurance" as a contract of insurance between a life insurer and another person (person C) under which the life insurer is secured, fully or partially, against a risk by person C.

The term does not include a contract that:

- secures against financial risk unless, in the contract, it is incidental to securing against life risk; or

- is, or is part of, a tax avoidance arrangement.

The words "fully" and "partially" describe the extent to which the life insurer is secured against life risk; they do not describe the term for which the reinsurance is provided.

Sections EY 12(2) and (3) describe the meaning of "full reinsurance" and "partial reinsurance". Such reinsurance is limited to those contracts where the life insurer offered or was offered or entered into the life reinsurance policy or policies in New Zealand. If a life reinsurance policy is not offered or entered into in New Zealand, a deduction for the policy’s life reinsurance premiums is denied under section DR 3 and the policy’s life reinsurance claims are treated as exempt income under section CW 59C .

This means that all references to the relevant life reinsurance amounts in any of the calculations in the Act exclude the policies that are not offered or entered into in New Zealand.

There are two further express exclusions from the definition of "life reinsurance" that are also relevant when calculating taxable income under the new rules:

- general insurance, such as trauma insurance or non-life insurance policy riders such as total permanent disability benefits.

- financial arrangements – to ensure practical consistency with the definition of "life insurance policy" (which means a policy which states the terms under which life insurance is covered).

These exclusions are required to ensure elements of a contract that do not themselves qualify as life reinsurance are excluded from the definition. However, Inland Revenue considers that reinsurance of events related to life insurance (for example, policy lapse) are not excluded. Accordingly, reinsurance of lapses of policies and discontinuance profit (or loss), which are connected to life insurance, are also "life reinsurance".

Table 1 shows the effect of reinsurance transactions on a life insurer’s taxable income.

Table 1: Effect of reinsurance on taxable income

| Transactions | Gross income |

|---|---|

| Reinsurance commissions of $500,000 received under a contract of reinsurance. The total amount relates to the risk components of the claims paid. | +$500,000 |

| Life insurance premium paid under a contract of reinsurance of $1,500,000. | –$1,500,000 |

| $600,000 received under a profit sharing arrangement in relation to a contract of reinsurance. | +$600,000 |

| $300,000 recovered as a refund of premiums paid under a contract of reinsurance. | +$300,000 |

Life financial reinsurance

Some types of reinsurance in substance focus more on capital management than on risk transfer, and section EY 12(5) excludes such arrangements from the definition of "life reinsurance". It does so by defining them as "life financial reinsurance".

Premiums for a reinsurance contract that is "life financial reinsurance" are non-deductible to the life insurer, and the investment income is brought to tax by the life insurer under the financial arrangement rules.

The life financial reinsurance rules look to the substance of an arrangement - in particular, whether the arrangement is a financing arrangement rather than reinsurance. Reinsurance - for example, should involve the transfer of insurance risk from the ceding insurer to the assuming insurer. A transfer of insurance risk may have taken place under a contract of reinsurance when it is reasonably possible that the assuming insurer may realise a loss from the contract; or be exposed to a range of potentially adverse outcomes under the contract.

Non-residents - reinsurance

Section EY 48 provides that the Income Tax Act 2007 applies to life insurance business carried on by a non-resident in connection with life insurance policies that are offered or entered into in New Zealand and life reinsurance policies that relate exclusively to those life insurance policies.

Transfers of life insurance business

Ordinary tax rules apply for transfers of life insurance business. However, section EY 5(4) prescribes that where a life insurer (the transferor) transfers life insurance business to another life insurer (the transferee), the transferor does a part-year calculation for each class of policy in the transferred business. The transferee also does a part-year calculation for the transferred policies.

The transferee’s relevant opening part-year reserve amounts under sections EY 23 to EY 27 equal the transferor’s relevant closing part-year reserve amounts. The transferee’s relevant opening part-year reserve amounts are adjusted by adding life reinsurance value to the transferee’s opening, and subtracting from the transferor’s closing. The part-year calculations do not create any part-year tax obligations.

Part II: Transition

Grandparenting of term life products

Sections EY 30 and EZ 53 to EZ 60 and section YA 1

Overview of the transitional rules for term life products

Section EY 30 ensures that only existing policies contracted under the previous tax rules are grandparented and subject to transitional rules for a period of up to five years. The application of the previous life rules are therefore preserved for term policies sold before the start of the new life insurance rules. The start date for the transitional rules (the grandparenting start date) will, for most life insurers, be 1 July 2010, unless the insurer elects an earlier date.

The five-year transition period is directed at annual renewable term policies (also known as yearly renewable term, or age-related term policies).

If the policy is a single premium, level premium or guaranteed premium, it can be grandparented for the life of the policy or for the period for which the premium is guaranteed. These periods can be longer than five years.

Life insurers can elect out of transitional rules at any time - see section EY 30(6).

Life insurance contracts that materially change in nature - for example, when the level of life insurance cover provided is increased, are considered to be new contracts. New contracts should not enjoy the benefits of the previous rules over the grandparenting period.

Early grandparenting start date allowed

If a life insurer elects to apply the new rules from the beginning of its income year - which includes 1 July 2010, it can also make a further election that grandparenting will apply to policies entered into before the beginning of the same income year. If it does not make this election, grandparenting will apply to policies entered into before 1 July 2010.

Application of the grandparenting rules

Life insurers can elect that the grandparenting rules apply to:

- a product when it is "issued" (that is, the life insurer accepts the risk on the life of the individual); or

- when the policy is applied for and a deposit is received in respect of the application.

In either case, the event must have occurred before the grandparenting start-date.

A "deposit" has its ordinary commercial meaning as being a payment in advance to support a commercial transaction. For example, a debit authority by itself would not meet the statutory tests in section EY 30(2).

If an application is made and the deposit is received before the grandparenting start-date and the policy is ultimately not accepted, it would not be subject to grandparenting in any case.

Eligibility for grandparenting applies on a policy by policy basis. The calculation of the adjustment and the opt-out is done on a class of policy basis.

Special grandparenting rules for certain types of policies

Special grandparenting rules apply to the class of policies listed below:

- Single premium policies: The previous taxation rules will effectively apply for the life of the policy. Section EY 30(5)(a) applies to policies where one premium is only ever payable for the life policy.

- Level premium and guaranteed level premium policies: The previous taxation rules will effectively apply for the longer of five years or the period for which the premium is guaranteed. Section EY 30(5)(b) applies to policies where the premium cannot be changed over the period

- for example, $500 for each year over 15 years, or if the premium does not in fact change over the period.

Section EY 30(5) recognises the fact that although level term policies may, in some instances allow premiums to be changed at the insurer’s discretion, commercial constraints mean that the insurer does not increase the premium payable. - Group life master policies: Group life master policies are defined in section YA 1 as "a life insurance policy with multiple individuals’ life insurance cover grouped under it, if the group of individuals is identified in the policy and the general public are excluded". The previous taxation rules will apply to lives insured under these policies. Employer-sponsored policies and credit-card repayment insurance are excluded and have their own separate rules.

- Employer sponsored group policy: The previous life insurance rules will effectively apply to lives insured under employer-sponsored group life policies. Section EY 30(4)(d) requires that there is no savings element in the policy and that the substantive and material terms of the policy do not change on or after the grandparenting start-day. The guarantee period applies only to rates that are guaranteed at the time of application of the proposed life tax rules for a maximum of five years from the application date. Officials are continuing discussions with life insurers about the practical effect of these rules.

- Credit card repayment insurance: The previous life insurance rules will effectively apply to credit card repayment insurance (CCRI) policies that are master policies. The life cover for each life insured does not need to be in place before the grandparenting start-day. As the amount of cover provided by a CCRI policy fluctuates on a regular basis and, by month to month, the amount of cover could increase by a substantial percentage. The insurer has no control over these credit limit increases. Given the nature of CCRI policies, the 10 percent cover increase requirement to these policies is not applied. All CCRI policies therefore have grandparenting for five years from the application date.

- Life reinsurance: Life reinsurance is included in the definition of "group life master policy" in section EY 30(14). The effect of this provision is to look-through the reinsurance treaty for transition purposes so that the terms applying to the individual reinsured policy, as set out in the treaty, should determine the extent of transition rules applying for that policy. Section EZ 62 provides a special transition rule for life financial reinsurance contracts that are entered into before the date the life insurer applies the new rules for the first time. The maximum transition period for life financial reinsurance is the shorter period of the life of the contract or five years.

Table 2 summarises the operation of the grandparenting rules.

Table 2: Operation of grandparenting rules.

When grandparenting ceases to apply

Life policies sold before the grandparenting date will cease to be covered by the grandparenting rules if the policy is altered or modified in such a way that it is effectively a new policy. If the transitional rules cease to apply to a grandparented life policy, the new rules will have effect to that policy from the first day of the income year in which alteration or modification occurred.

There are, however, several situations when an event that creates a change or alteration will not result in the life policy being subject to the new rules:

- Reinstated policies: It is not uncommon for policies to lapse or be cancelled as a result of policyholders missing premium instalments. Under section EY 30(1)(a), policies entered into before the grandparenting application date but reinstated after that date continue to be subject to the transitional rules, provided that the reinstatements are made within 90 days of lapsing and that the insurer does not treat the reinstated policy as a new policy. The reinstated policy should have the same terms as the lapsed policy.

- Replacement policy when the life insurer is sold: A life policy that replaces an existing policy as a result of a life insurer being sold, or the life insurer selling its rights and obligations under the old policy, is treated as being issued at the same time as the old policy. The replacement policy is therefore subject to the transitional rules provided it has substantially the same term as the old policy – EY 30(1)(b).

- Certain increases in life cover: Grandparenting is not affected in situations when the amount of insured cover does not increase by an amount up to the greater of an annual CPI adjustment or 10 percent of the previous year’s amount – as described in section EY 30(2)(c). The date for considering if this threshold has been breached is determined by choosing the "cover review period". The "cover review period" starts on the first day of the life insurer’s income year, for a class of policies unless it has chosen an alternative date during the income year. The alternative date, once chosen, is irrevocable. If the insured cover is breached under this rule, the class of policies is subject to full taxation under the new rules from the beginning of the income year in which the breach occurs, irrespective of the day of the actual breach.

Calculation of transition adjustment for grandparented life polices

Grandparented policies are taxed under the new rules but are allowed a deduction equal to the amount calculated under the expected death strain formula (life) in accordance with sections EZ 53 to EZ 60 (which relate to the transitional adjustment for expected death strain) for the income year.

Tax losses carried into the new rules

Sections EZ 61, IT 1 and IT 2

Under the old rules, a life insurer may have losses carried forward from either or both the life office base and policyholder base. The new rules provide that the only life office base loss is carried forward into the new tax rules as it better reflects the income of the entire life insurance business.

For life insurers with a 30 June balance date, or for taxpayers with other balance dates that elect to enter into the new rules on the first day of the income year that includes 1 July 2010, the new rules allow the existing life office base loss at the end of their income year ending 30 June 2009 to be available for carry-forward and allocated as a shareholder base loss. The loss can be offset with the life insurer’s income (including, by way of election, policyholder base income subject to limitations as discussed below) and group company losses, subject to ordinary continuity and grouping rules.

Section EZ 61 effectively provides, on an annual basis, that the life office base loss carried forward is first applied against shareholder base income and any excess, up to the value of any base concession amount not yet used, can be elected to be deducted against any policyholder base income. The base concession amount is determined under section EZ 61 on entry into the new rules, and is the lower of the life office base loss carried forward and the policyholder base loss cancelled under section IT 1. The base concession amount is used up by election to be a policyholder base deduction amount.

Example 2, illustrates the use of tax losses under the previous rules that are carried into the new rules under section EZ 61.

Deemed sale

Section EZ 63

The previous life insurance rules provided that investment income in the life office base was calculated under ordinary rules, with some gains and losses being accounted for as taxable income when realised. Under the policyholder base, the reserve calculations had the effect of recognising changes in the value of investments on an unrealised basis. The effect of these rules had the potential to create timing differences when recognising income between the two bases.

To remove this difference, the new rules provide that investments taken into account in determining policyholder reserves for the policyholder base calculation under section EY 2 are treated as having been sold and reacquired at market value on entry into the new rules.

For investments in a PIE, that is not a "listed PIE" (as defined), the deemed disposal rule does not apply - section EZ 63(3).

Transitional year and end of transitional adjustments

Section EY 5

If a life insurer has a balance date other than 30 June and has not elected an early adoption of the new rules, the life insurer does part-year tax calculations for the income year bisected by 1 July 2010. The addition of the two calculations forms the assessment of tax for that income year.

Example 2: Carry-forward of losses into the new rules

The following example illustrates a typical tax calculation of a life insurer with a balance date of 30 June for the first income year under the new life rules. The life insurer has a range of products such as non-participating policies including annuities and capital guaranteed investment policies, participating policies, annuities, international shares, Australasian shares, PIE investments and a life fund PIE.

This illustration is intended to assist life insurers to interpret the new life rules and meet their compliance obligations by providing a suggested format for reconciliation of taxable income to the life insurer’s statutory accounts. It does not take into account all possible fact patterns and situations that could arise for a life insurer or reinsurer.

1 A frequently used way of describing life products is whether they are participating or non-participating policies. A participating policy (also known as a "with profit policy") is a policy entitled to participate in distributions of profit - as most of life and endowment policies are. Conversely, a non-participating policy (also known as "without-profit policy") does not participate in distributions of profit, examples being term life insurance and most unit-linked policies.