PAYE subsidy for small businesses

2006 legislative changes enable Inland Revenue to subsidise the use of payroll agents to meet the PAYE obligations of small businesses.

Sections NBB 1 to NBB 7, OB 1 of the Income Tax Act 2004 and sections 3(a)(xiii) and 3(o), 185(1)(f) and (g), 185C, and 185D of the Tax Administration Act 1994

Changes have been made to the Income Tax Act 2004 and the Tax Administration Act 1994 to enable Inland Revenue to subsidise the use of payroll agents to meet the PAYE obligations of small businesses.

Under the new rules, the government will subsidise or partly subsidise the cost of an employer engaging a payroll intermediary. The subsidy will be available for up to five employees of a particular employer per month. To obtain the subsidy an employer must engage a listed PAYE intermediary. The listed PAYE intermediary will be eligible to receive a subsidy from the government.

Background

Consultation conducted by the government showed that many small businesses consider the time spent keeping up to date with PAYE and calculating deductions could be better spent running their business.

The PAYE subsidy proposal was a simplification initiative outlined in 2003 in the discussion document, Making tax easier for small businesses. It provides a subsidy to payroll intermediaries for meeting PAYE obligations on behalf of small employers.

"PAYE intermediaries" are Inland Revenue accredited incorporated or unincorporated entities acting as intermediaries between employers and Inland Revenue. Under the current rules, employers provide the intermediary with payroll information about their employees and the gross wages to the intermediary. The intermediary is then responsible for calculating the PAYE deductions, meeting all return filing requirements and paying both the employees and Inland Revenue.

It is expected that the subsidy will encourage small employers to use PAYE intermediaries for meeting their PAYE obligations. The foreseeable benefits of this include:

- the reduction of compliance costs for small businesses;

- improvement of the PAYE system in general

– payroll intermediaries would provide services to a large number of employers, using their skills and technology to increase the accuracy and timeliness of returns. The improved quality of the PAYE compliance will benefit employers whose exposure to penalties for non-compliance will be reduced; - the outsourcing of compliance obligations faced by small businesses will allow small employers to focus their efforts on their business, rather than compliance activities;

- an improvement in the timeliness of payments and quality of information supplied to Inland Revenue and the reduction in penalties imposed on small business.

To establish a subsidy regime, legislative changes have been made.

The decision on the final amount and structure of the subsidy will be set by regulation.

Key features

Listed PAYE intermediaries

New section NBB 2 of the Income Tax Act specifies the conditions that must be fulfilled for PAYE intermediaries to be registered as a listed PAYE intermediary. The significance of the registration lies in the fact that only "listed" PAYE intermediaries are eligible to receive a subsidy. The conditions for becoming a listed PAYE intermediary include the following requirements:

- The applicant is an accredited PAYE intermediary under subpart NBA of the Income Tax Act. This requirement suggests that a prospective listed PAYE intermediary must be able to comply with the requirements imposed on "accredited" PAYE intermediaries in addition to the requirements imposed by the new legislation.

- The applicant who has already acted as an accredited PAYE intermediary for an employer has done so in a correct manner.

- The applicant has available the administrative and IT systems necessary to perform the obligations of a listed PAYE intermediary.

Inland Revenue may specify a period for which a person is accredited as a listed PAYE intermediary.

New section NBB 3 of the Income Tax Act describes the ongoing obligations of listed PAYE intermediaries. The obligations include:

- continuing to maintain the status of, and perform the obligations imposed on, an accredited PAYE intermediary;

- continuing to perform the obligations imposed on a listed PAYE intermediary in section NBB 2(1)(c) to (g), as described above in relation to section NBB 2;

- maintaining the required administrative and IT systems;

- correctly returning the subsidy claim form;

- keeping the records necessary to verify the information contained in each subsidy claim form.

New section NBB 4 of the Income Tax Act describes circumstances when the listing of a listed PAYE intermediary can be revoked and the process that must be followed to achieve the revocation. Generally, the listing may be revoked if the intermediary fails to comply with the requirements imposed on listed PAYE intermediaries or ceases to comply with the requirements that are necessary for being given accreditation as a listed PAYE intermediary.

In addition, section NBB 4 states that the Commissioner may give notice to a listed PAYE intermediary of his intention to revoke the listing and the reasons for the intended revocation. If the listed PAYE intermediary does not resolve the matters listed in the notice of intended revocation to the satisfaction of the Commissioner within 30 days, the Commissioner may give 14 days' notice of revocation. At the expiration of the notice of revocation, the listing of the listed PAYE intermediary is revoked.

The subsidy claim

New section NBB 5 of the Income Tax Act specifies that a listed PAYE intermediary subsidy claim form must be filed within one month of the date of filing of the employer monthly schedule to which it relates.

The Commissioner is allowed, within two years of receipt of the claim form, to make changes to the particulars of the form to correct any errors that the Commissioner may have found. The Commissioner would then give the listed intermediary 14 days' notice of the proposed amendments. An overpayment or underpayment that results from the amendment must be paid by the listed PAYE intermediary or the Commissioner within 30 days of the giving of the Commissioner's notice of the amendments. Alternatively, the Commissioner may elect to offset an overpayment against a claim for payment of the subsidy made after expiry of the 14-day notice period.

New section NBB 6 of the Income Tax Act specifies the conditions and the process that Inland Revenue will follow when paying a subsidy to a listed PAYE intermediary. A subsidy will be paid to a listed PAYE intermediary, working for a small employer, if the intermediary:

- has contracted with the employer for the provision of those services; and

- has met the obligations of the listed PAYE intermediary under subpart NBA of the Income Tax Act 2004, such as making the necessary tax deductions to the Commissioner and delivering an employer monthly schedule in relation to the employer; and

- files a correct subsidy claim form.

If it is satisfied that the subsidy should be paid, Inland Revenue will then pay the subsidy within 30 days of receipt of the following:

- the employer monthly schedule to which the listed PAYE intermediary claim form relates;

- payment of the PAYE deductions to which the listed PAYE intermediary claim form relates;

- the listed PAYE intermediary claim form.

The subsidy will be paid by Inland Revenue by electronic means. Within 14 days of the subsidy payment, Inland Revenue will provide the intermediary with particulars of the subsidy payment in electronic form.

Section NBB 6 also authorises the Governor-General to make regulations to prescribe the amount of the subsidy.

New section NBB 7 of the Income Tax Act governs the termination of an employer's arrangements with a listed PAYE intermediary. The section prescribes that either the employer or the listed PAYE intermediary may give notice of termination. The section also provides that if a listed PAYE intermediary ceases to act for an employer while still being in possession of the employer's funds, it must continue to act as a listed PAYE intermediary for the employer in relation to those funds.

Section OB 1 of the Income Tax Act defines a "listed PAYE intermediary claim form" as being in an electronic format and showing:

- the tax file number of the listed PAYE intermediary;

- the tax file number and name of each employer for which a subsidy is being claimed;

- the tax file number and name of each employee of each employer for which a subsidy is being claimed;

- the pay period to which the claim form relates;

- the pay frequency of each employee in that pay period;

- the number of source deduction payments made by the listed PAYE intermediary for each employee in the period to which the form relates; andLarger version of image

- the amount of subsidy that the listed PAYE intermediary is claiming for the period the form relates to.

{kind=link}

This information will assist Inland Revenue to calculate the correct amount of the subsidy that can be paid to the listed PAYE intermediary.

Example

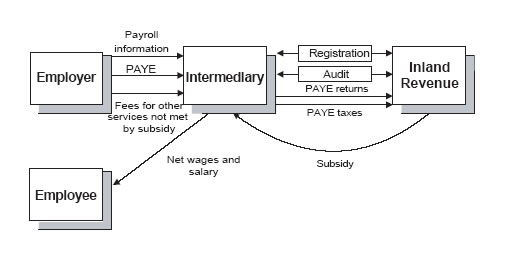

The interactions between employers, employees, listed PAYE intermediaries and Inland Revenue under the amended proposal are outlined in the diagram below:

[ Larger version of image | ]

Application date

The provisions apply from 1 October 2006.