Choice of FIF calculation method

2012 explanation of the five FIF calculation methods and the general rules for choosing methods as outlined in section EX 46(3).

Sections EX 46, EX 47, EX 48 and EX 62

If none of the exemptions from the FIF rules apply (as discussed previously), the person has an attributing interest in a FIF.

Calculation methods

For each attributing interest in a FIF, the person must choose one of the five FIF calculation methods listed in section EX 44:

- the fair dividend rate method;

- the cost method;

- the comparative value method;

- the deemed rate of return method; or

- the attributable FIF income method.

Sections EX 46, EX 47, EX 48 and EX 62 limit a person's choice of calculation method.

Section EX 46 outlines the general rules for choosing each of the FIF calculation methods. Section EX 62 limits a person's ability to change from a method that they are currently using for a particular FIF.

Choosing the attributable FIF income method

Section EX 46(3) limits the attributable FIF income method to interests in FIFs that are companies (as opposed to FIFs that are foreign superannuation schemes or foreign life insurance policies).

Portfolio investment entities that hold interests in foreign companies cannot use the attributable FIF income method.

Section EX 46(3) also prevents a person from using the attributable FIF income method if they cannot obtain sufficient information to perform the calculations in section EX 50. Note that there are two types of information that may be relevant for the purposes of this requirement:

- If a person has sufficient accounting information to apply and satisfy the active business test in section EX 21E so that the FIF is non-attributing, they will comply with this requirement.

- If a person is unable to satisfy the active business test in section EX 21E, they will only comply with this requirement if they can access the more detailed financial information that would be required to calculate attributable income under the tax concepts in sections EX 21D or EX 18.

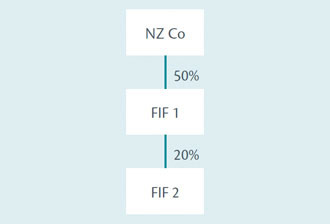

Generally, a person must hold a 10% or greater income interest in a foreign company in order to apply the attributable FIF income method. Note that this interest can be held indirectly through a CFC or another FIF that uses the attributable FIF income method. This is because the person's income interest is calculated to include an indirect income interest (see sections EX 50(4) and EX 10). For example, in the following structure NZ Co would have an income interest of 10% in FIF 2.

Example

A person with less than a 10% interest in a foreign company may nevertheless be able to use the attributable FIF income method if the foreign company is a CFC1 and a market value for shares in the CFC is not available except by independent valuation (for example, if the CFC is not listed on a stock exchange). In addition there are restrictions on the types of investors in the CFC.

Neither the person nor a person with an interest of 10% or more in the CFC can be:

- a listed company;

- a group investment fund;

- a superannuation fund;

- a unit trust;

- a portfolio investment entity; or

- a trustee of a trust with a beneficiary who is one of the above.

Example

John has 1% of the shares in a CFC. A listed company has 8% of the shares in the CFC. John is able to use the attributable FIF income method, but the listed company cannot. If the listed company had 10% or more of the shares in the CFC, John would not be able to use the attributable FIF income method.

Choosing the fair dividend rate method

If a person is unable to use the attributable FIF income method, or does not want to use this method, the main alternative is the fair dividend rate method.

The fair dividend rate method can be used for an attributing interest in a FIF that is an ordinary share and for which a market value is available. If a person cannot obtain a market value for an interest that is an ordinary share, they will generally use the cost method.

Choosing the cost method

The cost method calculates income in a similar way to the fair dividend rate method.

In order to use the cost method, the FIF interest must be an ordinary share and the person must not be able to obtain a market value for the interest except by independent valuation. If a person is able to obtain a market value without an independent valuation (for example, if the FIF is listed on a stock exchange), they will usually be required to apply the fair dividend method.

Non-ordinary shares

Persons with non-ordinary shares are generally required to use the comparative value method if they can obtain a market value, or the deemed rate of return method if they cannot obtain a market value. Non-ordinary shares are defined in section EX 46(10).

Deemed rate of return method

When a person has a non-ordinary share and cannot obtain a market value for that share, they are generally required to use the deemed rate of return method.

Choosing the comparative value method

Aside from non-ordinary shares, the only persons who can apply the comparative value method are natural persons and trustees of a trust for the benefit of a loved one or charity (see section EX 46(6)). If a natural person or a trustee of a trust for the benefit of a loved one or charity chooses to apply a comparative value method to any of their FIF interests, they cannot use the fair dividend rate method or the cost method for any of their other FIF interests. This implies that these persons must be able to use the comparative value (or the attributable FIF income method) for all of their attributing FIF interests.

When the comparative method is used for ordinary shares, the gains or losses on all of those shares are combined to produce an overall gain or loss for that year. If there is an overall loss across all of these holdings the person is considered to have zero income from these interests (see section EX 51(8)). In other words, the FIF losses cannot be used to offset other income.

However, if the comparative value method is used for non-ordinary shares, any losses on these shares can be used to offset other income. (Section EX 51(8) does not apply to non-ordinary shares.)

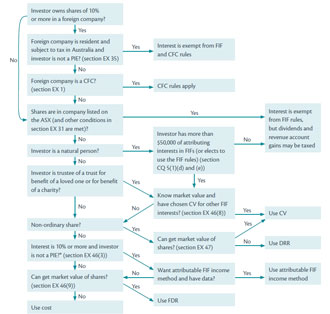

Summary diagram of main exemptions and limitations on choice of method

The following diagram summarises the main exemptions to the FIF rules and limitations that would apply to an investor's choice of calculation method under the new rules. Note the diagram does not include the rules in section EX 62 which limit an investor's ability to change from a method that they are currently using to a different method. The changes to section EX 62 are described below.

Note

This is a simplified illustration. In particular, it assumes the interest is a share in a foreign company and it excludes a number of the less commonly used FIF exemptions.

* Subject to certain conditions a person with a less than 10% interest in a CFC may be able to use attributable FIF income method.

Limitations on changing method

In general, once investors start to use a calculation method for a FIF interest they are required to continue using the same calculation method. Section EX 62 supports this approach by providing a set of rules that limit an investor's ability to change from a FIF calculation method that they are currently using to a different FIF calculation method.

Changing from the accounting profits method

A person who used the accounting profits method in the year preceding the repeal of this method can change to any other method (see section EX 62(2)(a)).

Changing to, or from, the attributable FIF income method

A person who used the branch equivalent method in the year preceding the repeal of this method can change to the attributable FIF income method (see section EX 62(6)(a)).

A person can change from the attributable FIF income method if sections EX 46(a) and (b) prevent them from using the attributable FIF income method, or if it is impossible to obtain enough information to continue to use the method. Note that this second condition could be met in cases when a person previously satisfied the active business test but now no longer satisfies the test and cannot access sufficient information to calculate their attributable income under normal tax concepts.

If the previous paragraphs do not apply, there are additional requirements that must be met before a person can change to, or from the attributable FIF income method. These requirements differ depending on whether it is the first time that the person has for, that particular FIF, changed to the attributable FIF income method (from a different FIF calculation method), or from the attributable FIF income method (to a different FIF calculation method).

If it is their first change, they only need to notify the Commissioner of Inland Revenue of the change, and the reason for the change of method.

If the person has already used their one "free" change that they are allowed for a particular FIF, but wants to change to, or from, the attributable FIF income method a second time, they must notify the Commissioner as above, but as part of their notification they must also be able to show that:

- there has been a change in circumstances that significantly changes the person's ability to obtain enough information to use the attributable FIF income method; and

- altering their income tax liability is not the principal purpose or effect of the change.

Changing to the fair dividend rate method

Taxpayers are generally able to change to the fair dividend rate method from the accounting profits method, the branch equivalent method or the deemed rate of return method if they are using the fair dividend rate method for their first income year beginning on or after 1 July 2011. This recognises the fact that the accounting profits method and the branch equivalent method have been repealed and the deemed rate of return method is now restricted to non-ordinary shares.

Taxpayers are able to change from the fair dividend rate method if it becomes impossible to obtain a start-of-year market valuation except by independent valuation (see section EX 62(2)(f)).

They are also able to change from the cost method to the fair dividend rate method if they are able to use the fair dividend rate method and can now get a market value for the FIF other than by independent valuation, for example, if the FIF becomes listed on a stock exchange. (See section EX 62(2)(g).)

Natural persons and trustees of a trust for the benefit of a loved one or charity are able to change between the fair dividend rate and comparative value methods in consecutive years without restriction (see section EX 62(8)). However, if they use comparative value for one interest, they cannot use the fair dividend rate for another interest. This means that the comparative value method will generally apply to their entire share portfolio.

1 Even though the company is a CFC, a person with less than a 10% interest in the CFC (including interests of associated persons) will use the FIF rules as opposed to the CFC rules to attribute income from the CFC.