Third-party royalties paid through a chain of CFCs

2012 legislation applies an exemption for royalty payments that pass through a chain of controlled foreign companies in certain circumstances.

Section EX 50B(5)(d)

In general, royalty payments are attributable income when they are received by a CFC. However there are several exceptions to this. One of these exceptions did not operate as intended and has been corrected.

The exception in section EX 20B(5)(d) provides an exemption for royalty payments in cases where a New Zealand company owns intellectual property and licenses this to a CFC which in turn sub-licenses it to a person who is not associated with the CFC.

The Act modifies the exemption so that it also applies to royalty payments that pass through a chain of two or more associated CFCs, so long as the royalty:

- is paid in relation to intellectual property that is owned by a New Zealand resident;

- is licensed to one of the CFCs in the chain; and

- is ultimately derived from another royalty that is paid by person who is not associated with the chain of CFCs.

The reference to "ultimately derived" means that the royalty should be an amount that is similar to the amount of the original third-party royalty.

Note that the transfer pricing rules could apply if the related party royalties are significantly different from the third party royalty.

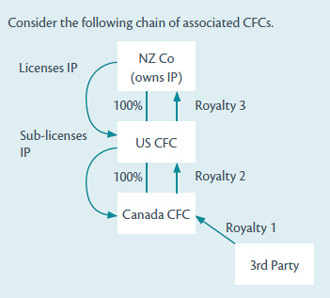

Example

Royalty 1 is exempt income of Canada CFC because it is paid by a person who is not associated with Canada CFC.

Royalty 2 is exempt income of US CFC because it is paid by Canada CFC which is associated with US CFC and it arises from Royalty 1 which was paid by a person who is not associated with these CFCs.

Royalty 3 is taxable income of NZ company. It is expected that royalty 3 should be for an amount that is the same or similar to the amount of the original royalty from the third party.