Sale and leaseback of intangibles

2005 amendments ensure taxpayers entering into transactions involving the sale/leaseback of intangibles do not get deductions for repayments of loan principal.

Sections FC 8B and OB 1 of the Income Tax Act 1994 and Income Tax Act 2004

Introduction

Amendments have been made to ensure that taxpayers entering into transactions involving the sale and leaseback of intangibles such as trademarks do not get deductions for what are, in substance, repayments of loan principal. The amendments are designed to protect the tax base.

The tax rules for finance leases, which prevent deductions being taken for the principal amount of a deemed loan, have been amended to ensure that the transactions involving the sale and leaseback of intangibles that cause concern are caught by these rules.

Background

The government announced in May 2003 that it was concerned about a scheme involving the sale and leaseback of intangibles under which tax deductions were claimed for what were, in substance, repayments of principal under a loan. The government said that it would propose remedial legislation to ensure that such deductions could not be taken.

Schemes that may allow deductions for repayment of loan principal

Described below are the simplified features of a transaction under which, before these amendments, deductions may have been allowed for what are, in substance, loan principal repayments.

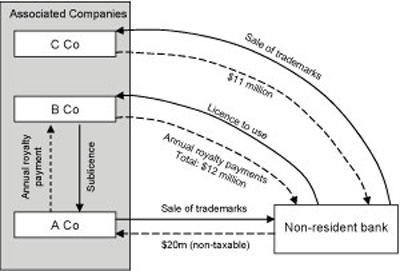

A Co, B Co and C Co are associated. A Co sells its trademarks or brand names to a non-resident bank for, say, $20 million (which is non-taxable as any profit is a capital gain). The bank immediately grants to B Co an exclusive licence to use the trademarks for a fixed term in return for annual royalty payments totalling, say, $12 million that are deductible to B Co. B Co grants a sublicence to A Co on the same terms. The bank grants to C Co an option to purchase the trade marks, subject to the bank retaining the right to receive the licence payments from B Co. The exercise price under the option is, say, $11 million, the reduction in value of the trademarks from $20 million reflecting the bank's right to continue to receive the royalty income from B Co during the licence period. The option is exercised on the date that the bank buys the trademarks and the licence begins, so that the bank pays A Co $20 million for the trademarks and immediately sells them to C Co for $11 million. The bank's net outgoing is $9 million, which it pays in return for future payments of $12 million.

In substance, the transaction is a loan of $9 million from the bank to the group, and the bank treats the transaction for tax, regulatory and accounting purposes accordingly. By structuring the loan as a licence, a deduction may have been available to B Co for what are, in substance, repayments of the $9 million principal, instead of only the $3 million interest that would be allowed if the transaction were in the form of a loan. This outcome is contrary to the policy intent underlying the tax treatment of debt transactions (and it may be that the tax avoidance provisions in the Income Tax Act 1994 apply to it).

Finance lease rule

The Income Tax Act contains provisions called finance lease rules that, in certain circumstances, recharacterise lease transactions as the purchase of the leased asset by the lessee, with the purchase funded by a loan from the lessor to the lessee. The lessee can depreciate the leased asset (if it is depreciable property) and, instead of obtaining a deduction for lease payments, obtains a deduction under the accrual rules for the interest component of the deemed loan. The treatment of the lessor mirrors that of the lessee - the lessor cannot depreciate the leased asset, and returns as income the interest component of the deemed loan.

The finance lease rules were introduced in 1982 and revised in 1999. They recognise that certain lease transactions are, in substance, financing arrangements, under which the lessor finances the purchase of the leased asset by the lessee. Broadly, they are triggered when the lease arrangement provides for the transfer of the asset to the lessee or an associate of the lessee, or when the asset is leased for most of its effective life.

Application of finance lease rules

The amended finance lease rules apply in the following way to the transaction in the example. The trademarks are treated as sold from the bank to B Co on the day the lease starts. The bank is treated as giving B Co a loan of $9 million, and B Co is treated as using the loan to purchase the trademark. The interest component of the deemed loan is $3 million (being $9 million consideration payable to B Co less $12 million consideration payable by B Co). This amount is deductible to B Co and spread under the accrual rules. B Co is treated as owning the lease asset (the trademarks) but as trademarks are not depreciable property, there is no depreciation deduction. This treatment accords with the correct policy outcome.

Key features

The following amendments to the finance lease rules in the Income Tax Act 1994 have been made to ensure that taxpayers entering into transactions involving the sale and leaseback of intangibles do not get deductions for what are, in effect, repayments of loan principal.

Licence to use intangible propert

It ha been clarified that the finance lease rules in sections FC 8A to FC 8I apply to the granting of a licence to use intangible property. This has been achieved by amending paragraph (f) of the definition of "lease" in section OB 1, which applies for the purposes of the finance lease rules.

The result of this amendment flows through to the other definitions that use the term "lease", such as "finance lease", "lease asset", "lease term", "lessee" and "lessor". In the definition of "lease asset", the personal property that is subject to the licence to use intangible property is the intangible property itself such as a trademark.

Application of definition of "finance lease" to arrangement

It has been clarified that the finance lease rules apply if a feature referred to in the definition of "finance lease" - such as a transfer of ownership to the lessee or an associate or an option granted to a lessee or an associate - is contemporaneously part of the lease arrangement but is not specified in the lease agreement itself. This has been achieved by changing the opening wording of the definition of "finance lease" in section OB 1 to refer to a lease that "involves or is part of an arrangement that involves" a feature of the definition.

Previously, the definition of "finance lease" referred to a lease "under which" there was a feature referred to in the definition. It was not clear whether this wording was adequate to catch an arrangement involving a feature of the definition, such as a transfer of ownership to a lessee or associate, which was documented separately from the lease.

The addition of "at the time of entry" wording in this amendment confirms that only any arrangement existing at the time a lease is entered into should be taken into account in determining whether or not the lease is a finance lease. Therefore events that occur subsequently and independently to entering into the lease are not treated as part of the arrangement (other than an effective extension of the lease term through a consecutive or successive lease for which an adjustment is made under section FC 8I).

Transfer of ownership of lease asset during lease ter

The application of paragraph (a) of the definition of "finance lease" in section OB 1 has been widened to include a lease under which ownership of the lease asset is transferred to the lessee or an associate of the lessee during or at the end of the lease term rather than only at the end of the lease term. Consequential amendments have also been made to section FC 8B(2) and (3) to refer to ownership of the lease asset being acquired on or by the date that the lease term ends.

New owner not entitled to lease payment

The definition of "finance lease" in section OB 1 has been expanded - new paragraph (d) - to include an arrangement that involves a right of an associate of the lessee to acquire the lease asset (or a right of the lessor to require an associate of the lessee to acquire the lease asset) during the lease term if the associate is not entitled to all of the lease payments that may fall due after the acquisition.

The new test targets a feature of the transactions causing concern: that the sale of the lease asset back to the associate of the lessee does not involve the associate as the new owner receiving all of the lease payments accruing from the date of sale, as would normally be the case. Instead, lease payments continue to flow to the previous owner (the financier). It is this feature of the transactions that indicates their financing nature and, accordingly, it is appropriate to treat arrangements with this feature as finance leases.

Other technical amendment

A technical error in paragraph (c) of the definition of "finance lease" in section OB 1 - which compares the lease term with the lease asset's estimated useful life - has been corrected by removing the reference to the formula in section EG 4(3). The purpose of this formula is to set the diminishing value economic rate of depreciation for an asset. However, intangible property that is fixed life intangible property must be depreciated using the straight line depreciation basis and cannot be depreciated on a diminishing value basis. Therefore the formula in section EG 4(3) can have no application to this type of depreciable property.

The new wording of paragraph (c) of the definition of "finance lease" now refers to "a lease term that is more than 75% of the lease asset's estimated useful life". The definition of "estimated useful life" in section OB 1 applies to all depreciable property, including fixed life intangible property.

The definition of "lessee" has been amended by omitting the reference to "hires, or bails". This reference and a reference to licensing intangible property are unnecessary because reliance can be placed on the reference to "leases". Section 32 of the Interpretation Act 1999 means that this latter reference has a corresponding meaning to the paragraph (f) definition of "lease", which includes a hire, bailment or a licence to use intangible property.

This amendment also makes the definitions of "lessee" and "lessor" consistent because the latter does not use hire or bailment terminology.

The foregoing amendments to the definition of "finance lease" in section OB 1 have been achieved by replacing that definition.

The main purpose of the amendments is to protect the tax base. The amendments are not intended to affect normal commercial leasing transactions that do not raise tax base maintenance concerns.

Application date

The amendments apply for arrangements entered into on or after 29 March 2004.