Part III - Goods and Services Tax Amendment Act (No. 3) 1988

Archived legislative commentary on Part III - Goods and Services Tax Amendment Act (No. 3) 1988 from PIB vol 177 Oct 1988.

This commentary item was published in Public Information Bulletin Volume 177, October 1988

More information about Public Information Bulletins.

Section 1 - Short Title

This section provides for this Act to be referred to as the Goods and Services Tax Amendment Act (No. 3) 1988 which amends the Goods and Services Tax Act 1985.

This Act came into force on the 28th of July 1988, the date on which the Act received the Governor-General's assent. It applies to supplies made on or after that date.

Only section 2 has a different application date (for details see below).

Section 2 - Interpretation

Section 2 amends the meaning of the definition of the term "consideration" contained in section 2 of the GST Act.

Prior to this amendment, the Act provided that a registered person, in the course of making taxable supplies, was unable to make an unconditional gift (i.e., a donation). Hence any payment made by a registered person which would constitute a donation (if made by any other person) was treated under the GST Act as a payment for the supply of goods and services and therefore subject to GST if the recipient non-profit body was registered. This was based on the premise that a business always expects something in return for a payment.

This amendment removes this distinction. This means that where a registered person makes a donation to a non-profit body in the course of its taxable activity, the payment is not subject to GST in the hands of the non-profit body. However, if the person making the payment, or an associated person, receives any identifiable direct valuable benefit in the form of a supply of goods and services then the payment is subject to GST.

This amendment does not apply in respect of payments made by the Crown or any public authority as such payments are specifically excluded from the meaning of the term "unconditional gift". They therefore remain taxable when made to registered persons.

The amendment applies in respect of any payments made on or after 1 October 1988.

Section 3 - Meaning of term "supply"

This section amends section 5 of the GST Act by introducing a new subsection (6C) to provide certainty as to the GST treatment of candidates' deposits in local body and parliamentary elections. Prior to this amendment some doubt was expressed as to whether the deposit, when forfeited, was consideration for the supply of goods and services.

The amendment ensures that:

- The deposit is consideration (GST inclusive) for the supply of services; and

- The supply occurs when the deposit is forfeited. Forfeiture occurs where the candidate polls insufficient votes.

This means that there are no GST implications at the time the deposit is paid by the candidate or when the deposit is refunded by the Local Authority or the Justice Department. However, if the deposit is forfeited the Local Authority or Justice Department is required to account for 1/11th of the amount of the deposit as output tax.

The amendment applies to deposits forfeited on or after the 28th July 1988, i.e., the date on which the Act received the Governor-General's assent. The ruling made by the Department at the time of the introduction of GST stating that such deposits were consideration for a supply when the deposit was forfeited applies in respect of the deposits forfeited prior to the application date of this amendment.

Section 4 - New sections inserted relating to the furnishing of returns following change in rate of tax

Section 4 of the Amendment Act (No. 3) 1988 introduces two new sections i.e., sections 78A and 78B to the Goods and Services Tax Act. These sections provide transitional arrangements for implementing a rate change should the Government in the future make a decision to increase or decrease the rate of GST. These new sections relate to:

- The return filing requirements on a change in the rate of GST; and

- An adjustment to be made by registered persons who account on the payments basis in respect of supplies made or received that have not been accounted for in any taxable period ending prior to the change in the rate of GST.

The reason for introducing these transitional provisions at this early stage is to increase certainty for both taxpayers and the Department.

(i) New section 78A - Returns to be furnished in 2 parts for taxable period in which change in rate of tax occurs

All registered persons are allocated a taxable period in terms of section 15 or section 15A of the GST Act and these taxable periods are staggered and of varying duration (1, 2, or 6 months). It is therefore not possible for all registered persons to have a taxable period beginning on the day on which a change in the rate of tax comes into force. This new section therefore applies where the taxable period allocated does not commence on the same date as the change in the rate of tax.

The amendment requires registered persons whose taxable period spans the date on which the change in the rate occurs to file a return in two parts for that taxable period. The first part of this return will cover the period from the beginning of that period to the day before the change in the rate of GST occurs. The second part will cover the balance of the taxable period. This ensures that the first part of the return only includes supplies at the old rate whilst the second part only includes supplies at the new rate. These two parts together form the return for that taxable period and both are required to be furnished on or before that person's normal due date (i.e., one day and one month after the last day of the taxable period).

Where a person has adopted an alternative date for the last day of a taxable period in terms of section 15(7) of the Act (i.e., plus or minus 7 days) that person will also be required to furnish a return in two parts where that alternative day does not coincide with the change in the rate. For example, if a registered person's taxable period ended on the last Saturday of the month and the rate change came into force on the following Wednesday, then that person would be required to furnish a part I return in respect of the period Sunday to Tuesday inclusive and a part II return in respect of the balance of the taxable period.

This amendment applies from the day on which the Act received the Governor-General's assent (i.e., 28th of July 1988) but has no practical application until a change in the rate of GST comes into force.

Subsection summary

Section 78A(1) requires all registered persons whose taxable period does not commence on the same day as the change in the rate comes in to force to furnish a return in two parts for that taxable period. The Part I return covers the period from the beginning of that period to the day before the change in the rate comes into force. The second part covers the balance of the taxable period.

Section 78A(2) states that these parts will be in a form prescribed by the Commissioner and be deemed to be a single return.

Section 78A(3) provides that if the two parts are furnished separately, section 46 (Interest on refunds) has no application until both of the parts have been received by the Commissioner.

Section 78A(4) provides that a return has to be in two parts where a registered person is required to file a return in terms of section 16(2) of the Act because that person has ceased to be registered and the period of that final return spans the change in the rate coming into force.

(ii) New section 78B - Adjustment to tax payable for persons furnishing returns on payments basis following change in rate of tax

In general, the application of the new rate in respect of the supply of goods and services will be determined by reference to the time of supply (i.e., this is generally the earlier of the issue of an invoice or any payment being received in respect of the supply). For example, if a service is performed prior to the change in the rate and the invoice is issued after the change in the rate, GST on the supply is imposed at the new rate. Appendix E of this PIB sets out in detail the various time of supply rules in the GST Act and the manner in which the change in the rate will apply.

For registered persons on the invoice basis of accounting, this is consistent with the normal rules of accounting for GST on supplies made or received.

However, in relation to registered persons on the payments basis of accounting this is not the case. Generally, such registered persons account for GST on supplies made or received to the extent that a payment is made or received. This will mean that in any one taxable period a registered person may be accounting for tax in respect of supplies that may have been partly accounted for in previous taxable periods. If there was a change in the rate of GST, such a person would be required to account for tax in relation to different supplies at both the old and new rate on an ongoing basis. In order to simplify accounting for GST and to ensure consistent application of the new rate to supplies made by both types traders on the invoice and payment basis of accounting, an adjustment is provided.

The adjustment is to be made only by persons on thepayments basis in respect of all taxable supplies made or received (refer Time of Supply rules) that have not been accounted for in calculating the tax payable before the date of the change in the rate of tax. This adjustment is taken into account in either the part I return or the return for the taxable period that ends on the day before the change in the rate of GST. After the adjustment registered persons can apply the new tax rate to ALL amounts received and paid out in subsequent return periods.

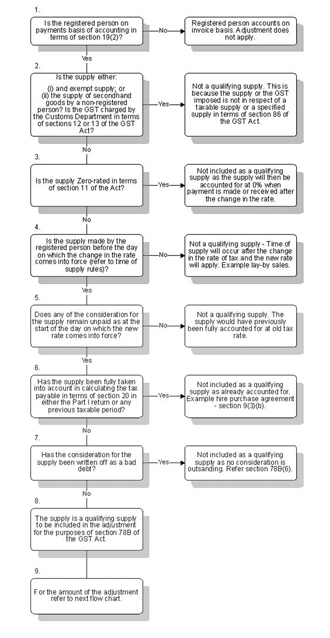

"Qualifying supply"

The adjustment is made in respect of any "qualifying supply". A qualifying supply is:

- any taxable supply made to or by a registered person prior to the date of the change in the rate; or

- any specified supply within the meaning of section 86 of the GST Act, -

to the extent that the consideration for the supply remains unpaid and has not been written off as a bad debt as at date of the change in the rate. The adjustment does not apply to any supply that has been fully taken into account in calculating the tax payable of a registered person in the part I return or any previous taxable period or is zero-rated. Neither does it apply to any supply to the extent to which it has been partly taken into account in calculating the tax payable of a registered person in the part I return or any previous taxable period.

(i) Taxable supplies made by or to a registered person

- A taxable supply is any supply made in NZ that is charged with GST at 10% in terms of section 8 and includes supplies that are zero-rated. To determine whether supplies are made by or to a registered person prior to the date of the change in the rate, the time of supply rules will apply. Supplies which became taxable on the introduction of GST in terms of section 84 of the Act are also included. Appendix E of this PIB details the time of supply rules. Zero-rated supplies are specifically excluded from being qualifying supplies.

(ii) Section 86 specified supplies

On the introduction of GST an adjustment was able to be used by a person on the payments basis of accounting to claim an input credit in respect of debtors outstanding as at 1 October 1986. The registered person then simply accounted for 1/11th of all receipts on or after 1 October 1986. The supplies to which this alternative method applied were termed specified supplies under section 86 of the Act and are covered by the new adjustment to the extent that those supplies have not been previously been [sic] accounted for under section 20 of the Act.

(iii) To the extent that ...

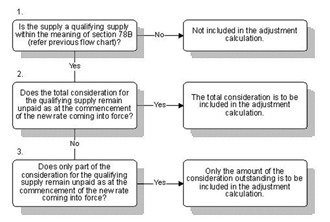

The purpose of this phrase is to ensure that amount of "qualifying supplies" for the purposes of the adjustment is limited to the amount of the consideration of the supply that remains unpaid and has not been previously accounted for in a prior taxable period or part I return. This means that the total consideration for a supply is included in the adjustment where:

- The taxable supply has been made or received prior to the change in the rate;

- The total consideration for that supply remains unpaid; and

- The total consideration for that supply has not been taken into account in calculating the tax payable by the registered person in the part I return or any previous taxable period.

However, where the consideration for the supply has been paid for in part and accounted for to that extent, only the balance that remains unpaid and unaccounted for is included as "qualifying supply" for the purposes of the adjustment. In addition where any consideration for supply that may constitute a "qualifying supply" has been written off as a bad debt, the consideration for that supply is not to be included in the adjustment.

(iv) Debit and credit notes

Where a person on the payments basis of accounting is required to:

- make an adjustment, as the supplier, to correct the amount of output tax incorrectly accounted in terms of section 25(2); or

- make an adjustment, as the recipient of the supply, to correct the amount of input tax incorrectly accounted in terms of section 25(4) or 25(5)

the adjustment is accounted for in the taxable period in which the person becomes aware of the adjustment to the extent that any payment is received or made. This means in relation to a change in the rate of tax that these supplies will be included as "qualifying supplies" where the registered person has become aware of the adjustment or received a debit or credit note prior to the change in the rate but the consideration for that adjustment still remains unpaid or received as at that date.

(v) Supplies not included in adjustment

The legislation specifically excludes supplies that are zero-rated from being a "qualifying supply". This is because the supply will be accounted for at the same rate of tax imposed after the change in the rate.

GST that has been charged by the Customs Department in terms of sections 12 or 13 of the GST Act and remains unpaid as at the date of the change in the rate isnot included as a "qualifying supply". This is because the GST imposed is not on a taxable supply and the amount paid is separately identified on the GST return form as an input tax adjustment.

It should also be noted that any consideration that remains unpaid and has not been accounted for in the periods mentioned above in respect of secondhand goods acquired by a registered person for which an input tax credit can be claimed isnot a "qualifying supply". It has been decided that to the extent that the consideration is paid after a change in the rate of tax in respect of such a supply the registered person should claim it at the new rate.

(vi) Summary

It is considered that qualifying supplies will generally be supplies that have a time of supply generated in terms of section 9(1), 9(3)(a), 9(3)(aa), or 9(6) of the Act and includes debit and credit notes as discussed above. This is because other supplies are accounted for fully in the taxable period in which the time of supply occurs.

Flow charts are attached to assist in determining whether and to what extent a supply is a "qualifying supply".

Adjustment

The adjustment will require the registered person to identify the following amounts in respect of "qualifying supplies":

- The amount of the consideration payable on "qualifying supplies" made to that person (inputs); and

- The amount of the consideration payable on "qualifying supplies" made by that person (outputs).

The amount of consideration payable on "qualifying supplies" made to or by a registered person is limitedto the extent that the consideration for the supply remains unpaid and has not been previously accounted for in calculating the tax payable in period or part period prior to the day of the change in the rate. If the consideration has been written off as a bad debt then it is not included as consideration for a "qualifying supply" in the adjustment.

The amount in paragraph (ii) is subtracted from the amount in paragraph (i) and the resultant total is then multiplied by the difference between the old tax fraction subtracted from the new tax fraction to give the amount of the adjustment. This adjustment will be on a prescribed form which sets out the calculation.

If the amount of the adjustment calculated is a positive amount then it is deemed to be output tax in the period to the date of the change in the rate.

If the amount of the adjustment calculated is a negative amount then it is a credit (input tax) to the registered person and available to be set off in the following order:

- Against any tax payable that is outstanding in respect of any taxable periods ending prior to the change in the rate of GST;

- Against any tax payable in respect of the taxable period in which the new rate comes in force;

- Against any tax payable in respect of the next taxable period and so on until the amount of the credit is extinguished.

This provision will allow any credit still available to be set off and to be applied to back period reassessment where those assessments have been issued subsequent to the change in the rate.

This credit is in no case refundable by the Commissioner.

Bad debt adjustment

This adjustment is made where any consideration that has been included as a qualifying supply is subsequently written off as a bad debt. This is to ensure that the adjustment previously made in respect of the consideration for a qualifying supply is reversed. The amount of the adjustment is determined by multiplying the amount of the consideration written off as a bad debt by the difference of the old rate subtracted from the new rate.

If the amount is positive, it is deemed to be output tax in the period in which the bad debt is written off. Conversely, if the amount is negative, it is deemed to be input tax in the period in which it is written off.

Records

Where any adjustment is made in respect of qualifying supplies the registered person is required to prepare a list of debtors (supplies made by the registered person) and a list of creditors (supplies made to the registered person) showing the amounts due as at the start of the day of the coming into force of the new rate. These lists have to be retained for 10 years in terms of section 75 of the GST Act.

Application date

The application date of this amendment is the 28th of July 1988 (i.e. the day on which the Act received the Governor-General's assent) but has no practical application until a change in the rate of GST comes into force.

Subsection summary

Section 78B(1) provides that a person on the payments basis is required to make an adjustment in accordance with this section. The adjustment will be on a prescribed form and made in either the part I return required under section 78A or the taxable period ending on the day before the change in the rate.

Section 78B(2) sets out what supplies constitute a qualifying supply (and to what extent) for the purposes of this adjustment.

Section 78B(3) sets out the manner in which the amount of the adjustment is calculated.

Section 78B(4) provides if the amount of the adjustment is a positive amount it is deemed to be output tax attributable to the taxable period referred to in section 78A(1)(c).

Section 78B(5) provides that where the amount of the adjustment is a negative amount that the amount shall be a credit and available to be off set against any tax payable by the registered person. The subsection also sets out the order of the set off and provides that the credit shall not be refunded by the Commissioner.

Section 78B(6) provides that where the consideration for a qualifying supply has been subsequently written off as a bad debt the registered person is required to make an adjustment to reverse the adjustment made pursuant to section 78B(3). This provision requires the adjustment to be returned as either input or output tax in the taxable period in which the consideration is written off as a bad debt.

Section 78B(7) requires the registered person to prepare a list of debtors (in respect of the qualifying supplies made by the registered person) and creditors (in respect of the qualifying supplies made to the registered person) showing the amounts due as at the commencement date of the new rate.

Consequential amendment

Section 75(2) has been consequentially amended by section 4(2).

Section 4(2) of the Amendment Act makes a consequential amendment to section 75(2) of the principal Act by inserting in the paragraph (c) the expression section 78B(7). This amendment explicitly ensures the retention of lists of debtors and creditors prepared for the adjustment.

FLOW CHART TO DETERMINE WHETHER A SUPPLY IS A "QUALIFYING SUPPLY" FOR THE PURPOSES OF SECTION 78B

FLOW CHART TO DETERMINE THE AMOUNT TO BE INCLUDED IN THE ADJUSTMENT WHERE A SUPPLY IS A "QUALIFYING SUPPLY" FOR THE PURPOSES OF SECTION 78B

EXAMPLE

The following example shows the manner in which the new section 78A and 78B will apply. The example assumes that the rate of GST increases to 12.5% on the 1st day of April 19XX and apply to supplies made on or after this day.

Popular Books Ltd is a registered person carrying on the taxable activity of a stationery and book retailer. The company has been allocated a two monthly category B taxable period and has adopted the payments basis of accounting.

As the company's taxable period spans the new rate coming into force, Popular Books Ltd is required, in terms of section 78A, to furnish a return in two parts for the taxable period 1 March 19XX to 30 April 19XX.

The first part covers the period 1 March 19XX to 31 March 19XX (being the day before the increase in the rate comes into force). The company accounts for supplies in terms of section 20 of the Act as if that part was a taxable period in its own right. This means that the registered person must make any adjustments in terms of section 21 for that part of the taxable period to ensure that it is accounted for at the old rate. The taxable supplies made or received in this part are accounted for at the old rate, i.e. 10%.

The second part covers the period 1 April 19XX to 30 April 19XX. Supplies are accounted for in terms of section 20 of the Act as above and are accounted for at the new rate, in this example 12.5%.

These two parts form a return for the taxable period and the return (i.e., both parts) is due on or before the 1 June 19XX.

As the company is on the payments basis of accounting it is required to make an adjustment in terms of section 78B of the GST Act. The adjustment brings into account all taxable supplies made or received before the date of the rate change, that have not been taken into account for the purposes of calculating the tax payable before that date. This enables that company to account for tax at the new rate on ALL money received or paid out after the rate change.

The company is required to identify, as at 31 March 19XX, its debtors and creditors to establish whether they relate to a qualifying supply for the purposes of the adjustment. This involves ensuring that:

- The supplies made or received, for GST purposes, were made prior to the date on which the new rate came into force;

- At least some consideration remains unpaid at that date; and

- The consideration has not been previously accounted for in any previous taxable period or part I return.

A check of the company's debtors and creditors as at 31 March 19XX shows the following details. These amounts are inclusive of GST and therefore are the consideration unpaid.

| Creditors: | Debtors: | ||

|---|---|---|---|

| Finance Ltd | 750.00** | J Smith | 120.00 |

| Building Ltd | 150.00 | K Brown | 10.00* |

| Books Ltd | 1550.00 | J Green | 30.00 |

| Paper Ltd | 750.00 | K Grey | 50.50 |

| Pens Ltd | 650.00 | B Smith | 71.50 |

| Electricity Ltd | 75.00 | ABC Ltd | 750.00 |

| Stationery Ltd | 1450.00 | Bankers Ltd | 1050.00 |

| Builder P/ship | 675.00 | B Black | 120.25 |

| Total | $6,050.00 | J Blue | 75.25 |

| Total | $2277.50 |

* The debt owed by K Brown is in respect of a lay-by sale of which $60 has already been paid.

** The creditor Finance Ltd is in respect of the purchase of a cash register in term of a hire purchase agreement.

In relation to the above debtors and creditors the time of supply occurred prior to 31 March 19XX (date of rate change).

The company then has to determine whether the supplies made to and by the company are qualifying supplies. The attached Flow Charts may be of assistance.

The debt of $10 owed by K Brown is not included as a qualifying supply as it is not a supply until the property in the goods is transferred to the recipient (section 9(2)(c)).

The debt of $750 owed to Finance Ltd is not included as a qualifying supply as the supply would have been fully accounted for in the taxable period in which the agreement is executed (section 9(3)(b) and section 20(3)(b)(iii)).

The amount of the qualifying supplies is therefore:

| Taxable supplies received $5,300.00 | ($6,050.00 - $750.00) |

| Taxable supplies made $2,267.50 | ($2,277.50 - $ 10.00) |

Calculation of adjustment:

| Consideration payable on qualifying supplies made to the registered person (inputs) | $5,300.00 | |

| less | ||

| Consideration payable on qualifying supplies made by the registered person (outputs) | $2,267.50 | |

| (A) | $3,032.50 |

This amount is multiplied by the difference between the old rate tax fraction subtracted from the new rate tax fraction.

Old rate tax fraction: 1/11th

New rate tax fraction: 1/9th

1/9 - 1/11 = 2/99th (B)

The amount of the adjustment = (A) * (B)

$3,032 50 * 2/99 = $61.26

As this amount is a positive amount it is treated as output tax in the Part I return in terms of section 78B(1)(c)(i) of the Act.

The adjustment form is attached to the Part I return for the part of the taxable period 1 March 19XX to 31 March 19XX and is due on or before 1 June 19XX (as is the case with Part II of the return).

The company is also required to prepare a list of the debtors and creditors which constitute the "qualifying supplies" showing the amount of consideration due to or by the company as at the commencement of the day that the increased rate comes into force. These lists are not required to be furnished with the return but are required to be retained for 10 years in terms of section 75 of the Act.

When the company makes or receives any payment in respect of these qualifying supplies, GST is accounted for at the NEW RATE i.e., 1/9th of the consideration paid or received.

Clauses 37 and 38 of Taxation Reform Bill (No. 4)

These clauses which were to introduce new provisions relating to the GST treatment of non-profit bodies were removed from the Bill and were not enacted. These provisions related to: -

- GST being imposed on the supply of donated goods and services by non-profit bodies where the value of such supplies exceeded $5,000 per annum;

- GST being imposed on the supply of donated goods and services by non-profit bodies that have been significantly altered;

- The denial of input tax credits in respect of fund raising activities that do not involve the making of taxable supplies, and also of costs associated with the administering of donation; and

- The limitation of input tax credits in respect of taxable activities subsidised by donations.

These clauses were removed to allow the measures to be reviewed by the Brash Committee.

Appendix A

Tax Treatment of Redundancy Payments

Calculation of specified sum.

Example 1 - Taxpayer has been employed in the same employment for 11 years.

Total remuneration for 3 years prior to the termination of employment was $72,000.

| Specified sum is lesser of | (i) | $72,000/3 ($24,000) or |

| (ii) | $20,000 |

i.e. Specified sum equals $20,000.

Example 2 - Taxpayer has been employed in the same employment for 11 years.

Total remuneration for 3 years prior to the termination of employment was $54,000.

| Specified sum is lesser of: | (i) | $54,000/3 ($18,000) or |

| (ii) | $20,000 |

i.e. Specified sum equals $18,000.

Example 3 - Taxpayer has been employed in the same employment for 4 years and 6 months.

Total remuneration for 3 years prior to the termination of employment was $72,000.

Specified sum is (4/10) x b

b is lesser of:

- Average Remuneration over last 3 years, or

- $20,000

i.e. b is lesser of:

- ($72,000/3) x $24,000

- $20,000

Therefore b is $20,000 and specified sum is (4/10) x $20,000 = $8,000

Calculation of Tax on Redundancy Payments

Example 5

Data as for example 1

| Redundancy payment made: | $50,000 |

| less specified sum | $20,000 |

| $30,000 | |

| Income Tax (Payable by recipient) on | |

| 5% of $20,000 at, say, 33c | $330 |

| FBT (Payable by employer) on $30,000 at 24c | $7,200 |

| Example 6 | |

|---|---|

| Data as for example 1 | |

| Redundancy payment made: | 18,000 |

| less specified sum: | 20,000 |

| NIL | |

| Income Tax (Payable by Recipient) on 5% of $18,000 at, say, 33c | $297 |

Appendix B

Lump Sum Payments

Part A

LUMP SUM REDUNDANCY PAYMENTS - AS DEFINED.

Part B

LUMP SUM REDUNDANCY PAYMENTS - OTHER THAN THOSE WHICH SATISFY THE DEFINITION.

Appendix C

Questions and Answers

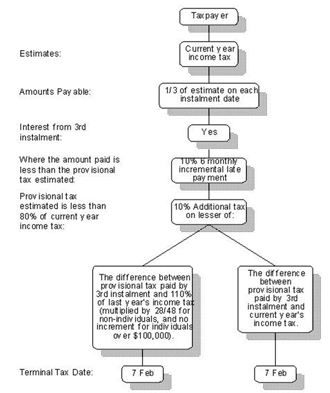

PROVISIONAL TAX PENALTIES - DETERMINATION OF LIABILITY

Questions

Following are a series of situations relating to various types of taxpayer. You are asked to determine if:

- The taxpayer is liable for any penalty

- If yes, whether liable for

- - Additional tax for late payment

- - Additional tax for underestimation

- - Interest (either paid by the Department or payable by the taxpayer).

Unless stated otherwise, provisional tax instalments are paid in full, on time.

- An individual taxpayer pays 1989 provisional tax (1988 plus 10%) of $60,000. 1989 provisional income is $110,000 and 1989 residual income tax is $65,000.

- A company calculates 1989 provisional tax (1988 plus 10% x 28/48) of $20,000. The third instalment is paid on 10 March 1989. 1989 provisional income is $80,000 and 1989 residual income tax is $22,000.

- The trust return for 1988 shows provisional income of $2,500 and 1988 residual income tax of $800. The trustees pay no 1989 provisional tax. The 1989 return shows provisional income of $2,900 and residual income tax of $1,000.

- DEF Ltd. estimates that 1989 income will be over $1,000,000 and estimates 1989 provisional tax of $290,000. The 1989 return shows income of $1,500,000 and residual income tax of $420,000.

- . Doctor Medicine's 1988 return shows provisional income of $90,000 and residual income tax of $35,000. 1989 provisional tax (residual income tax plus 10%) is $38,500. 1989 provisional income is $120,000 and terminal tax is $33,500.

- Ms Penny Farthing's 1988 return shows provisional income of $90,000 and residual income tax of $27,000. 1989 provisional tax (residual income tax plus 10%) is $29,200. By the third instalment she decides that her income will reduce and re-estimates her 1989 provisional tax at $18,000. The 1989 return shows provisional income of $60,000 and terminal tax of $25,000.

- The Ruapehu Trust's 1988 return shows provisional income of $15,000 and residual income tax of $3,000. 1989 provisional tax is $3,300. The 1989 return shows provisional income of $2,000 and residual income tax of $300.

- Rich People Ltd do not furnish their 1988 return until December 1988. Their 1988 return shows residual income tax of $51,000. On 7 November they pay enough tax so that in total, $34,000 has been paid. By 7 March 1989, the company decides that their 1989 income will be reduced and estimate their 1989 provisional tax at $40,000. On 7 March, they pay $4,000. When the 1989 return is furnished, residual income tax is $60,000.

Answers

| 1 | (a) | yes |

| (b) | Interest only (short paid) | |

| 2 | (a) | yes |

| (b) | additional tax for late payment interest (short paid) | |

| 3 | (a) | no |

| (b) | Nil | |

| 4 | (a) | yes |

| (b) | additional tax for underestimate interest (short paid) | |

| 5 | (a) | yes |

| (b) | interest (overpaid) | |

| 6 | (a) | yes |

| (b) | additional tax for underestimation interest (short paid) | |

| 7 | (a) | no |

| (b) | Nil | |

| 8 | (a) | yes |

| (b) | additional tax for short payment | |

| additional tax for underestimation interest (short payment) |

EXAMPLE

The taxpayer, a company, furnishes 1988 return in August 1988 showing provisional income of $150,000. The 1988 residual income tax is $72,000. 1989 provisional tax is calculated as $46,200 (72,000 x 110% x 28/48). By the third instalment date, the taxpayer decides that provisional income will reduce and uses the estimate option. The taxpayer estimates that residual income tax payable will be $35,000.

Payments are made as follows:

| 7 July 1988 | - | $24,000 | - | (Old regime payment) |

| 7 November 1988 | - | $ 6,800 | - | (2/3 of $46,200 less 7/7/88 payment) |

| 25 March 1989 | - | $ 3,200 | - | (Payment late and short. Should have been estimated residual tax less 1st and 2nd provisional tax instalments) |

When the 1989 return is furnished in August 1989, provisional income is shown as $180,000. 1989 residual income tax is $50,400. The 1989 assessment is issued on 7 November 1989.

Stage One - Calculate additional tax for late payment.

Provisional tax paid at the 3rd instalment date was less than provisional tax required to be paid so the taxpayer may be liable for additional tax. The account reads as follows:

| Date | Amount due | Amount paid | Balance |

|---|---|---|---|

| 7 November 1988 | $23,332 | $30,800 | $7,468 CR |

| 7 March 1989 | $11,668 | $0 | $4,200 DR |

| 25 March 1989 | $0 | $3,200 | $1,000 DR |

The account is recast using the taxpayer's estimate of $35,000.

As tax at 7 March was short paid, additional tax of $420 is imposed. The account is not cleared by 7 September 1989 so there is incremental additional tax imposed of $230 as follows:

| Date | Amount due | Amount paid | Balance |

|---|---|---|---|

| 7 March 1989 | $4,200 | $0 | $4,200 DR |

| 8 March 1989 | $420 | $0 | $4,620 DR |

| 25 March 1989 | $0 | $3,200 | $1,420 DR |

| 8 September 1989 | $142 | $0 | $1,562 DR |

Total additional tax for late payment is $562

Stage two - Calculate additional tax for underestimation.

| 1989 provisional tax estimate: | $35,000 |

| 1989 residual income tax: | $50,400 |

The amount estimated by the taxpayer is less than 80% of the residual income tax payable so additional tax must be considered. The taxpayer has voluntarily estimated so the taxpayer has additional tax limited to 10% of the difference between the payments made and the lesser of the 1989 residual income tax and the 1988 residual income tax plus 10%. In this example the 1989 residual income tax is used:

| 1989 residual income tax: | $50,400 | |

| Provisional tax payments: | $30,800 | The remaining payment was made after 7.3.88) |

| Balance remaining: | $19,600 | |

| Additional tax is 10% of balance = | $1,960 |

Stage three - Calculate interest.

The taxpayer is a not a natural person so automatically qualifies for interest.

Account reads as follows:

| 1989 residual income tax: | $50,400 | |

| plus additional tax for: | ||

| Late payment: | $420 | |

| Underestimation: | $ 1,960 | |

| Total: | $52,780 | |

| Paid to 7 March 1989: | $30,800 | |

| Balance: | $21,980 | |

| Payment received 25 March 1989: | $ 3,200 | |

| Balance at 25 March 1989: | $18,780 | |

| Incremental tax 8 September 1989: | $ 142 | |

| Balance at 8 September 1989: | $18,922 |

Tax Return assessed 7 November 1989:

Interest is calculated as follows:

| 8-3-89 to 25-3-89 (17 days) on $21,980 x 10% x 17/365 | = | $102.37 |

| 26-3-89 to 7-9-89 (165 days) on $18,780 x 10% x 165/365 | = | $848.95 |

| 7-9-89 to 7-11-89 (60 days ) on $18,922 x 10% x 60/365 | = | $311.04 |

| Total interest | $1,262.36 |

Stage four - the assessment

| 1989 Residual income tax: | $50,400 |

| Additional tax for: | |

| Underestimation: | $ 1,960 |

| Late payment: | $ 420 |

| Incremental tax for late payment: | $ 142 |

| Non-penal interest: | $ 1,262.36 |

| Total amount due: | $54,184.36 |

| Payments: | $34,000 |

| Total due as terminal tax: | $20,184.36 |

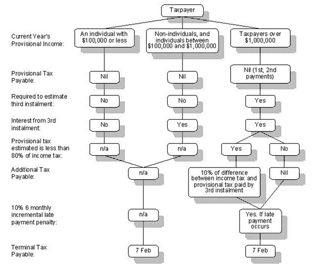

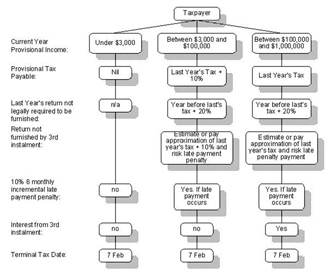

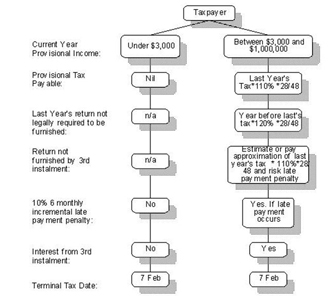

Appendix D

FLOWCHART OF THE AMENDED PROVISIONAL TAX REGIME

LAST YEARS PROVISIONAL INCOME WAS UNDER $3,000

FLOWCHART OF THE AMENDED PROVISIONAL TAX REGIME

Individual taxpayer with last year's provisional income of greater than $3,000 and current year provisional income less than $1,000,000.

Individual taxpayers with a provisional income last year exceeding $100,000 may use last year's tax with no increment. This is as interim arrangement reflecting the decrease in the marginal tax rates.

FLOWCHART OF THE AMENDED PROVISIONAL TAX REGIME

Non-individual taxpayers with a last year's provisional income of greater than $3,000 and current year provisional income less than $1,000,000.

Non-individual taxpayers may use last year's tax with an increment multiplied by this year's tax rate divided by last year's tax rate. This calculation is an interim arrangement reflecting the changes in tax rates non-individuals have experienced. e.g. Companies multiply the incremented provisional tax figure by 28/48.

FLOWCHART OF THE AMENDED PROVISIONAL TAX REGIME

TAXPAYERS WITH CURRENT YEAR PEOVISIONAL INCOME GREATER THAN $1,000,000

FLOWCHART OF THE AMENDED PROVISIONAL TAX REGIME

TAXPAYERS ELECTING TO ESTIMATE THEIR PROVISIONAL INCOME

Appendix E

Schedule of Time of Supply Rules and Application on the Change in the Rate of GST

| Section S. 5(2) | Time of supply rule Goods sold in satisfaction of a debt owed. Time of supply is the earlier of the issue of an invoice or any payment received. Section 17 return furnished. | When accounted for As a special return is furnished has no effect on registered persons. Refer to section 9(1) to determine rate applicable to the supply. |

| S. 5(3) | Goods retained on cessation of registration. Time of supply occurs at the time immediately before cessation. | The supply is accounted for in period that supply occurs. This rule determines the rate which applies for all traders. |

| S. 5(6B) | Road user charges. Time of supply occurs when and to the extent that any payment is made to the National Roads Fund. | The supply is accounted for in period when payment made. This rule determines the rate which applies for all traders. |

| S. 5(6C) | Election deposits. Time of supply occurs when the deposit is forfeited. | The supply is accounted for in period of forfeiture. This rule determines the rate which applies for all traders |

| S. 5 (11A) | Postage stamps used on postal notes. Time of supply is when the stamp is applied to postal note. (As postal notes are now not used this section has no application). | The supply is accounted for in period of application of the postage stamps. This rule determines the rate which applies for all traders. |

| S. 5(13) | Receipt of indemnity payments. Time of supply is the day on which the payment is received. | The supply is accounted for in the period of receipt of payment. This rule determines the rate which applies for all traders. |

| S. 9(1) | General time of supply rule. Earlier of the issue of invoice by the supplier or the recipient of the supply or the receipt of any payment by the supplier. | Persons on invoice basis account for the full consideration of the supply in the period in which this event occurs. Payments traders make an adjustment and simply account for tax at the rate applying when payment is received. This rule determines the rate which applies for all traders |

| S. 9(2) (a) | Supplies to associated persons. Time of supply is performance or availability if no invoice is issued or payment received before last day of filing return for that taxable period. If an invoice is issued etc., then section 9(1) applies | If time of supply is performance then accounted for in period in which this occurs. This rule determines rate which applies for all traders. If an invoice is issued etc., then accounted for as outlined above in terms of section 9(1) in the period this occurs. |

| S. 9(2) (b) | Door to door sales. Time of supply occurs when the 7 day cancellation period expires. | The supply is accounted for in the period in which the cancellation period expires. This rule determines the rate which applies for all traders. |

| S. 9(2) (c) | Lay-by sales. Time of supply occurs when the goods passes to the recipient of the supply — usually when full payment is made. If sale cancelled the supply occurs at that date. | The supply is accounted for in the period in which either of these events occur. This rule determines the rate which applies for all traders. |

| S. 9(2) (d) | The placing of a bet on a race. Time of supply occurs when the consideration for the bet is dealt with in terms of section 5(8). | The supply is accounted for in the period that the consideration for the bet is dealt with. This rule determines the rate which applies for all traders. |

| S. 9(2) (e) | Lotteries, games of chance. Time of supply occurs at the time of the first draw or determination of a result. | The supply is accounted for in the period that the first draw takes place. This rule determines the rate which applies for all traders. |

| S. 9(2) (f) | Machine or meter operated by a coin or token. Time of supply occurs when the coins or tokens are removed from the machine or meter. | The supply is accounted for in the period in which this event occurs. This rule determines the rate which applies for all traders. |

| S. 9(3) (a) | Goods supplied under an agreement to hire which provides for periodic payment. Time of supply occurs on the earlier of the payment becoming due or is received. | Persons on the invoice basis account for the supply in full in the period in which the earlier of these events occurs. Payments traders make an adjustment and simply account for tax at the rate applying when payment is received. This rule determines the rate which applies for all traders. |

| S. 9(3) (aa)(i) & (ii) | (i) Goods supplied periodically under an agreement. (ii) Construction progressive payments. Time of supply occurs on the earlier of the issue of an invoice to which that payment relates or any payment in respect of that supply becomes due or is received. | Persons on the invoice basis account for the supply in full in the period in which the earlier of these events occurs. Payments traders make an adjustment and simply account for tax at the rate applying when payment is received. This rule determines the rate which applies for all traders. |

| S. 9(3) (b) | Hire purchase agreements. Time of supply occurs at the time the agreement is entered into. | Supply is accounted for in the period in which the agreement is entered into. This rule determines the rate which applies for all traders. |

| S. 9 (6) | Goods supplied under an agreement in which goods have been appropriated but the whole of the consideration has not been determined. Time of supply occurs when and to the extent that any payment is due or received or an invoice is issued, whichever is the earlier | Persons on the invoice basis account for the supply in the period in which the earlier of these events occurs. Payments traders make an adjustment and simply account for tax at the rate applying when payment received. This rule determines the rate which applies for all traders. |

| S. 12 | Importation. Time of supply occurs when goods are entered or delivered for home consumption or to a manufacturing area. | Persons on the invoice basis account for GST in full in the period in which any payment is made or invoice received. Persons on the payments basis account for GST to the extent that a payment is made in a period. These rules determine the rate which applies. |

| S. 13 | Goods liable for excise duty applies at "in bond" prices. Time of supply occurs when the goods are removed from the bonded warehouse. | The accounting for GST is the same as for section 12 above. These rules determine the rate which applies. |

| S. 21 (2) | Adjustments where goods and services acquired for the principal purposes of making taxable supplies are applied for making other than taxable supplies — section 21(1). Time of supply occurs when those goods and services are so applied.so applied. | The supply is accounted for in the period to the extent that the goods and services are so applied. This rule determines the rate which applies for all traders. |

| S. 21 (4) | Fringe benefits. Time supply takes place at the time the registered person is liable to pay the fringe benefit tax. | The supply is accounted for in the period in which the liability to pay the fringe benefit tax arises. This rule determines the rate which applies for all traders. |

| S. 21 (5) | Adjustments where goods and services acquired after 1 October 1986 for the principal purposes of making other than taxable supples are applied for making taxable supplies. Time of supply occurs when those goods and services are so applied. | The supply is accounted for in the period to the extent those goods and services are so applied. This rule determines the rate which applies for all traders. |

| S. 22 | Goods and services acquired prior to incorporation. Time of supply occurs in the period in which the company reimburses the person who acquired those goods and services. | The supply is accounted for in the period of reimbursement. This rule determines the rate which applies for all traders. |

| S. 25 (2) | Supplier's adjustment of output tax incorrectly accounted for. Time of supply occurs in the period in which the adjustment is made. | The rate is the one that applies to the original supply. |

| S. 25 (4) & (5) | Recipient's adjustment of input tax incorrectly accounted for on the receipt of a debit or credit note. Time of supply occurs in the period in which the debit or credit note was received. | The rate is the one that applied to the original supply. |

| S. 26 | Bad debts written off and recovered. Time of supply occurs in the period in which the bad debt is written off or subsequently recovered. | The rate is the one that applies to the original supply written off and subsequently recovered. |