Disputes resolution process commenced by a taxpayer (June 08) (WITHDRAWN)

Withdrawn statement SPS 08/02 - Disputes resolution process commenced by a taxpayer. Statement provided for historical purposes only.

Withdrawn

This statement has been withdrawn and is provided for historical purposes only.

This item also appears in Tax Information Bulletin Vol 20, No 6 (July 2008).

Introduction

- This Standard Practice Statement ("SPS") discusses a taxpayer's rights and responsibilities in respect of an assessment or other disputable decision when the taxpayer commences the disputes resolution process.

- Where the Commissioner commences the disputes resolution process, the Commissioner's practice is stated in SPS 08/01: Disputes resolution process commenced by the Commissioner of Inland Revenue .

- This SPS has been updated due to changes made to the law under:

- the Taxation (Base Maintenance and Miscellaneous Provisions) Act 2005, and

- the Taxation (Savings Investment and Miscellaneous Provisions) Act 2006, and

- the Taxation (Depreciation, Payment Dates Alignment, FBT, and Miscellaneous Provisions) Act 2006, and

- the Taxation (Business Taxation and Remedial Matters) Act 2007, and

- the relevant case law decided since SPS 05/04: Disputes resolution process commenced by a taxpayer was published.

- The Commissioner regards this SPS as a reference guide for taxpayers and Inland Revenue officers. Where possible, Inland Revenue officers must follow the practices outlined in this SPS.

Application

- This SPS applies to a dispute commenced on or after 9 June 2008 or in the case of a dispute involving Goods and Services Tax ("GST") to a GST return period that ends on or after 31 March 2007. SPS 05/04: Disputes resolution process commenced by a taxpayer continues to apply from its commencement date up to 9 June 2008.

- Unless specified otherwise, all legislative references in this SPS refer to the Tax Administration Act 1994 ("TAA").

Background

- The tax dispute resolution procedures were introduced in accordance with the recommendations of the Richardson Committee in the Report of the Organisational Review of the Inland Revenue Department (April 1994) and were designed to reduce the number of disputes by:

- promoting full disclosure, and

- encouraging the prompt and efficient resolution of tax disputes, and

- promoting the early identification of issues, and

- improving the accuracy of decisions.

- The disputes resolution process ensures that there is full and frank communication between the parties in a structured way within strict time limits for the legislated phases of the process.

- The disputes resolution process is designed to encourage an "all cards on the table" approach and the resolution of issues without the need for litigation. It aims to ensure that all the relevant evidence, facts, and legal arguments are canvassed before a case goes to court.

- The disputes resolution process was introduced in 1996 and reviewed in July 2003. There have been changes made to the disputes resolution process following recent legislative amendments and case law since 2005.

- The early resolution of a dispute is intended to be achieved through a series of steps specified in the TAA. The main elements of those steps are the issue of:

- A notice of proposed adjustment ("NOPA"): this is a notice that either the Commissioner or taxpayer issues to the other advising that an adjustment is sought in relation to the taxpayer's assessment, the Commissioner's assessment or other disputable decision (the requisite form is the IR770 Notice of proposed adjustment ).

- A notice of response ("NOR"): this must be issued by the recipient of a NOPA if they disagree with it (the preferred form is the IR771 Notice of response ).

- A notice rejecting the Commissioner's NOR: this must be issued by the taxpayer if they disagree with the Commissioner's NOR (there is no prescribed form for a notice rejecting the Commissioner's NOR).

- A disclosure notice and statement of position ("SOP"): the issue of a disclosure notice by the Commissioner triggers the issue of a SOP. Each SOP must provide an outline of the facts, evidence, issues and propositions of law with sufficient details to support the positions taken. Each party must issue a SOP (the requisite form is the IR773 Statement of position). The SOPs are important documents because they limit the facts, evidence, issues and propositions of law that either party can rely on if the case proceeds to court to what is included in the SOPs (unless a hearing authority makes an order that allows a party to raise new facts or evidence under section 138G(2)).

- There are also two administrative phases in the process - the conference and adjudication phases. If the dispute has not been already resolved after the NOR phase, the Commissioner's practice will be to hold a conference, unless the parties agree to abridge the conference phase (please see paragraphs 180 to 183 of the SPS). A conference can be a formal or informal discussion between the parties to clarify and, if possible, resolve the issues.

- If the dispute remains unresolved after the SOP phase, the Commissioner will refer the dispute to adjudication, except in certain circumstances. Adjudication involves Inland Revenue independently considering a dispute and is the final phase in the process before the taxpayer's assessment is amended (if it is to be amended) following the exchange of the SOPs.

Contents

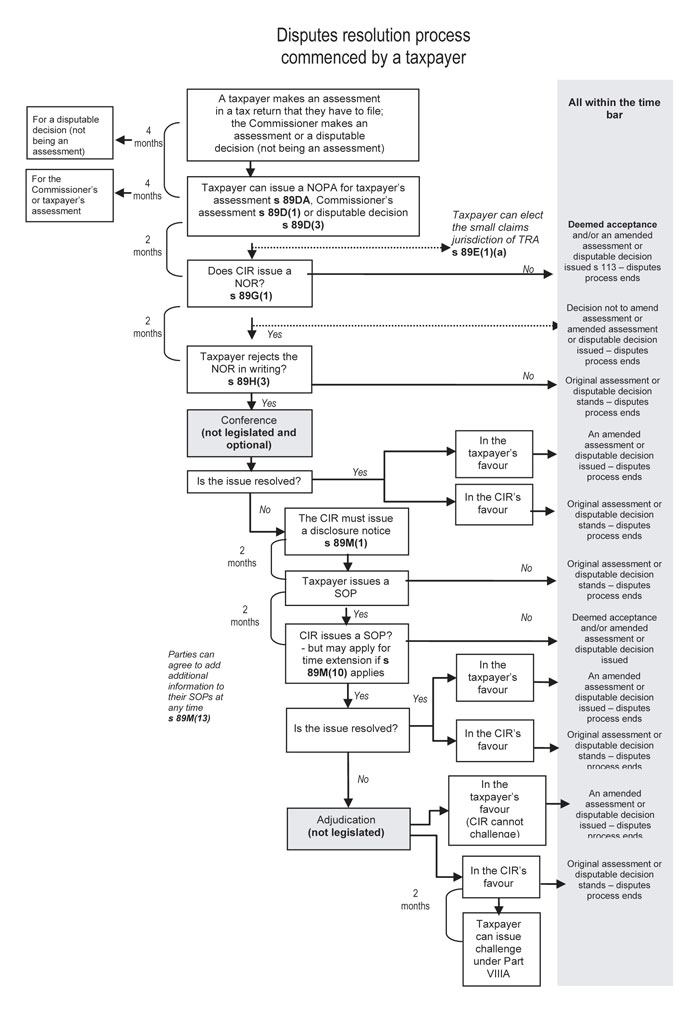

Disputes resolution process commenced by a taxpayer

The disputes resolution process is set out in the following diagram.

Click on the image below to get full sized view

Summary of key actions and indicative administrative time frames

- Set out below is a summary of the key actions and administrative time frames where a disputes resolution process is commenced by a taxpayer.

- These key actions and time frames are intended to be administrative guide lines for Inland Revenue officers. Any failure to meet these administrative time frames will not invalidate subsequent actions of the Commissioner or prevent the case from going through the disputes resolution process.

| Paragraph in the SPS | Key actions | Indicative time frames |

|---|---|---|

| The taxpayer's NOPA | ||

| 32, 37, 54, 65 and 70 | A taxpayer's response period for issuing a NOPA in respect of an assessment or other disputable decision | Within four months from the date that the assessment or other disputable decision is issued. |

| 83 | A taxpayer's response period for issuing a NOPA that relates solely to a research and development tax credit in respect of a notice of disputable decision or notice revoking or varying a disputable decision issued by the Commissioner. | Within one year that starts on the date that the Commissioner issues a notice of disputable decision or notice revoking or varying a disputable decision that is not an assessment. |

| 86 | A taxpayer's response period for issuing a NOPA that relates solely to a research and development tax credit in a notice of assessment that they have issued if they are a single person for the purpose of section 68D. | Within the period that ends two years (for an assessment that relates to the 2008-09 and 2009-10 income years) or one year (for an assessment that relates to the 2010-11 and later income years) after the date that the Commissioner receives the taxpayer's assessment. |

| 86(b) | A taxpayer's response period for issuing a NOPA that relates solely to research and development tax credits in a notice of assessment that they have issued if they are a member of an internal software development group or partner of a partnership that chooses to apply section 68E for the 2008-09 and later income years. | Within the period that starts on the date on which the Commissioner receives the taxpayers' assessment and ends 2 years (for an assessment that relates to the 2008-09 and 2009-10 income years) or 1 year (for an assessment relating to the 2010-11 and later income years) after the latest date that the taxpayer can provide an income tax or joint income tax return. |

| 118 | The Commissioner forwards and assigns the taxpayer's NOPA to the responsible officer. | Usually within five working days after the taxpayer's NOPA is received. |

| 120 | The Commissioner acknowledges the receipt of the taxpayer's NOPA (either by telephone or in writing). | Usually within 10 working days after the taxpayer's NOPA is received. |

| 121 | The Commissioner advises that the taxpayer's NOPA is invalid, but the applicable response period has not expired. | Immediately after the Inland Revenue officer becomes aware of the invalidity. |

| 123 | The Commissioner advises the taxpayer in writing that their NOPA is invalid and they have not rectified the invalidity within the applicable response period. | Usually within 15 working days after the date that the response period for issuing a taxpayer's NOPA expires. |

| 134 | The Commissioner considers the application of "exceptional circumstances" under section 89K, where a taxpayer's NOPA has been issued outside the applicable response period. | Usually within 15 working days after receiving the taxpayer's application. |

| The Commissioner's NOR | ||

| 146 | The Commissioner advises the taxpayer (either by telephone or in writing) whether the Commissioner intends to issue a NOR. | Usually within 10 working days before the response period for the taxpayer to issue a NOPA expires. |

| 146 | The Commissioner has issued and the taxpayer has received a NOR. | Within two months starting on the date that the taxpayer's NOPA is issued. |

| The taxpayer's written rejection of the Commissioner's NOR | ||

| 165 | The Commissioner confirms whether the taxpayer will reject the Commissioner's NOR. | Usually two weeks before the response period for the Commissioner's NOR expires. |

| 162 | The taxpayer rejects the Commissioner's NOR in writing. | Within two months after the date that the Commissioner's NOR is issued. |

| 168 | Inland Revenue forwards the taxpayer's rejection of the Commissioner's NOR to the responsible officer. | Usually within five working days after receiving the taxpayer's rejection. |

| 168 | The Commissioner acknowledges receipt of the taxpayer's rejection of the Commissioner's NOR. | Usually within 10 working days after receiving the taxpayer's rejection. |

| 169 | The taxpayer is deemed to accept the Commissioner's NOR, because they have failed to reject it within the applicable response period and none of the "exceptional circumstances" apply. | Two months after the response period for the Commissioner's NOR has expired. |

| Conference phase | ||

| 171 | The Commissioner contacts the taxpayer to initiate the conference phase. | Conferences usually commence within one month after the Commissioner receives the taxpayer's rejection of the Commissioner's NOR. The suggested average time frame of the conference phase is three months, subject to the facts and complexity of the dispute. |

| 183 | The Commissioner communicates the decision not to hold, or abridge any conference, which must be documented in writing and conveyed by the Commissioner or agent. | Usually within five working days after the date of the Commissioner's decision. |

| Disclosure notice | ||

| 186 | The Commissioner advises the taxpayer that a disclosure notice will be issued. | Usually within two weeks before the date that the disclosure notice is issued. |

| Taxpayer's SOP | ||

| 199 | The taxpayer must issue a SOP within the response period for the disclosure notice. | Within two months after the date that the disclosure notice is issued, unless any of the "exceptional circumstances" under section 89K applies. |

| 213 | The Commissioner confirms whether the taxpayer will issue a SOP. | Usually 10 working days before the response period for the disclosure notice expires. |

| 213 | The Commissioner forwards the taxpayer's SOP to the responsible officer. | Usually within five working days after the taxpayer's SOP is received. |

| 215 | The Commissioner acknowledges the receipt of the taxpayer's SOP. | Usually within 10 working days after the taxpayer's SOP is received. |

| 215 | The Commissioner advises that the taxpayer's SOP is invalid, but the two-month response period has not expired. | Inland Revenue officers will advise the taxpayer or their agent as soon as they become aware of the invalidity. |

| 215 | The Commissioner considers whether "exceptional circumstances" under section 89K apply, where the taxpayer has issued a SOP outside the applicable response period. | Usually within 15 working days after the taxpayer's application is received. |

| 216 | The dispute is treated as if it was never commenced, if the taxpayer fails to issue a SOP within the applicable response period and none of the "exceptional circumstances" apply. | Usually 10 working days after the response period for the disclosure notice expires. |

| The Commissioner's SOP | ||

| 218 | The Commissioner issues a SOP in response to the taxpayer's SOP. | Within two months after the date that the taxpayer's SOP is issued, unless an application has been made to the High Court under section 89M(11). |

| The Commissioner's addendum | ||

| 224 | The Commissioner provides additional information via addendum to the Commissioner's SOP within the response period for the taxpayer's SOP. | Where applicable, within two months after the date that the taxpayer's SOP is issued. |

| 228 | The Commissioner considers a taxpayer's request to include additional information in the SOP. | Usually within one month after the date that the Commissioner's SOP or addendum is issued. |

Adjudication | ||

| 241 | The Commissioner prepares a cover sheet and issues a letter (with a copy of the cover sheet) to the taxpayer to seek concurrence on the materials to be sent to the adjudicator. | Usually within one month after the date that the Commissioner's addendum (if any) or the response period for the taxpayer's SOP expires. |

| 242 | The taxpayer responds to the Commissioner's letter. | Within 10 working days after the date that the letter is issued. |

| 243 | The Commissioner forwards materials relevant to the dispute to the Adjudication Unit. | Usually when the Commissioner receives the taxpayer's response or within 10 working days after the date that the Commissioner's letter is issued. |

| Adjudication of the disputes case | Usually four months after the date that the Adjudication Unit receives the disputes files, depending on the number of disputes that are before the Adjudication Unit, any allocation delays and the technical, legal and factual complexity of those disputes. | |

| The taxpayer can file challenge proceedings under section 138B in respect of an assessment or amended assessment | Within two months after the assessment or amended assessment is issued. |

Standard Practice and Analysis

Taxpayer's assessment

- Section 92(1) reads:

A taxpayer who is required to furnish a return of income for a tax year must make an assessment of the taxpayer's taxable income and income tax liability and, if applicable for the tax year, the net loss, terminal tax or refund due.

- Section 92(1) applies to tax on income derived in:

- the 2005-06 and later tax years for a taxpayer whose income year matches the tax year, and

- the corresponding income year for a taxpayer whose income year is different from the 2005-06 and later tax years.

- If a taxpayer has to file an income tax return they must make an assessment of their taxable income and income tax liability and, if applicable, the net loss, terminal tax or refund due. The definition of disputable decision in section 3(1) includes an assessment made by a taxpayer.

- Similar requirements apply to a taxpayer who must file a GST return under the Goods and Services Tax Act 1985 ("the GST Act"). For a GST return period that begins on or after 1 April 2005, the taxpayer must make an assessment of the amount of GST payable. Section 92B(1) reads:

A taxpayer who is required under the Goods and Services Tax Act 1985 to provide a GST tax return for a GST return period must make an assessment of the amount of GST payable by the taxpayer for the return period.

- Pursuant to sections 92(2) and 92B(2) the assessment date for an income tax or GST assessment made by a taxpayer is the date that Inland Revenue receives the taxpayer's tax return.

- However, under section 92B(3) for a GST assessment and section 92(6) for an income tax assessment, a taxpayer cannot make an assessment of the amount of tax payable for a return period in their tax return if the Commissioner has previously made an assessment of the tax that is payable for that return period. This is commonly known as a "default assessment" and involves the Commissioner making a default determination that estimates the taxpayer's tax liability (for example, if they have missed a return filing deadline).

- For further discussion regarding how a taxpayer can dispute a default assessment please see paragraphs 37 to 49. Any later amendment to a default assessment must be the Commissioner's assessment made under section 113. The Commissioner can make any such amendment on the basis of the information provided in the taxpayer's tax return and treat that return as a record of the taxpayer's assertion of their tax liability.

- When the taxpayer's assessment is received, the Commissioner's practice is to stamp, either electronically or manually, the tax return with the date of receipt. This date is then entered into Inland Revenue's computerised database and a return acknowledgment form is sent to the taxpayer or agent. This practice ensures that the taxpayer will have a clear record of when their assessment was made.

The Commissioner's assessment

- Notwithstanding section 92(1) and subject to the statutory time bar in sections 108 and 108A, the Commissioner can sometimes issue a notice of assessment to a taxpayer.

- The Commissioner cannot make an assessment without first issuing a NOPA to a taxpayer, unless an exception under section 89C to the requirement for issuing a NOPA applies.

- For example, under section 6A, the Commissioner settles challenge proceedings in the Taxation Review Authority ("TRA") and a disputes resolution process commenced by the taxpayer. The Commissioner enters into an individual settlement deed and agreed adjustment with the taxpayer to confirm the settlement. The Commissioner will apply section 89C(d) and give effect to the settlement deed and agreed adjustment by issuing an assessment to the taxpayer under section 89J(1) without first issuing a NOPA. In this circumstance section 89J(1) prevents the parties from further disputing the previously agreed adjustment.

- The exceptions under section 89C are explained in the Commissioner's practice as stated in SPS 08/01: Disputes resolution process commenced by the Commissioner of Inland Revenue. (The Commissioner must ensure that any assessment is made in accordance with section 89C. However, if, on a rare occasion, an assessment was made in breach of section 89C, it will still be regarded as being valid under section 114(a)).

- If the Commissioner issues an assessment without first issuing a NOPA, the taxpayer can issue a NOPA to the Commissioner under section 89D(1) or challenge proceedings under section 138B(3) in respect of that assessment.

A taxpayer can issue a NOPA to the Commissioner

- A taxpayer can issue a NOPA to the Commissioner in the following six situations:

Situation 1: NOPA in respect of the Commissioner's assessment

- Section 89D(1) reads:

If the Commissioner:

(a) Issues a notice of assessment to a taxpayer; and

(b) Has not previously issued a notice of proposed adjustment to the taxpayer in respect of the assessment, whether or not in breach of section 89C,-

the taxpayer may, subject to subsection (2); issue a notice of proposed adjustment in respect of the assessment. - When the Commissioner issues to a taxpayer a notice of assessment that does not relate to a "default assessment" (as discussed in paragraph 21) without first issuing a NOPA, the taxpayer can issue to the Commissioner for receipt a NOPA in respect of the assessment. A taxpayer's response to a default assessment is discussed under the heading Situation 2: NOPA in respect of the Commissioner's default assessment.

- A taxpayer's NOPA is not an assessment. It is an initiating action that allows open and full communication between the parties. A NOPA forms a basis for ensuring that the Commissioner does not issue an assessment without some formal and structured dialogue with the taxpayer in respect of the grounds upon which the Commissioner is issuing any assessment or amended assessment (McIlraith v CIR (2007) 23 NZTC 21,456).

- If the Commissioner has issued an assessment the taxpayer can issue a NOPA under section 89D(1) in respect of any of the considerations that were relevant to making the assessment. This could include preliminary decisions which are necessary to make the assessment, for example, a decision made by the Commissioner under section 89C (MR Forestry (No 1) Trust Ltd v CIR (2006) 22 NZTC 19,954).

- The taxpayer must issue the NOPA within the applicable "response period" as defined in section 3(1). Generally, this will be within the four-month period that starts on the date that the Commissioner issues the assessment unless the Commissioner accepts a late NOPA under section 89K(1). However, this response period is subject to the exception discussed in Situation 6 : NOPA that relates solely to a research and development tax credit.

- For example, if the Commissioner's notice of assessment is issued on 7 April 2008, under section 89D(1) the taxpayer must issue a NOPA in the prescribed form in respect of the assessment on or before 6 August 2008.

- The taxpayer's right to issue a NOPA under section 89D(1) is unaffected, even if, in a very rare circumstance, the Commissioner made the assessment in breach of section 89C. The assessment will be deemed to be valid under section 114(a).

Situation 2: NOPA in respect of the Commissioner's default assessment

Default assessment that does not relate to GST

- If a taxpayer has not filed a tax return, the Commissioner can make a default assessment under section 106(1) without first issuing a NOPA to the taxpayer.

- Section 89D(2) reads:

A taxpayer who has not furnished a return of income for an assessment period may dispute the assessment made by the Commissioner only by furnishing a return of income for the assessment period.

- A taxpayer that intends to dispute a default assessment through the disputes resolution process must:

- pursuant to section 89D(2) provide a tax return for the period to which the default assessment relates notwithstanding that the tax return cannot include the taxpayer's assessment (section 89D(2A)), and

- issue a NOPA to the Commissioner in respect of the default assessment within the applicable response period. Generally, this will be within the four-month period that starts on the date that the Commissioner issues the default assessment.

GST default assessment

- Similar rules apply to a NOPA that a taxpayer issues in respect of a GST default assessment.

- Section 89D(2C) reads:

A taxpayer who has not provided a GST tax return for a GST return period may not dispute the assessment made by the Commissioner other than by providing a GST return for the GST return period.

- Where a taxpayer has not filed a GST return, the Commissioner can make a GST default assessment without first issuing a NOPA to the taxpayer.

- If a taxpayer wants to dispute a GST default assessment through the disputes resolution process, they must:

- provide a GST return for the periods to which the GST default assessment relates pursuant to section 89D(2C) for return periods beginning on or after 1 April 2005, notwithstanding that the tax return cannot include the taxpayer's assessment (section 89D(2D)), and

- issue a NOPA to the Commissioner in respect of the GST default assessment,

within the applicable response period. That is, within four months from the date that the default assessment is issued.

- The legislative requirement to provide a tax return i n respect of a default assessment made by the Commissioner under section 106(1) when issuing a NOPA is an additional requirement of the disputes resolution process. This ensures that the taxpayer has provided the requisite statutory information before they dispute the assessment.

- If the Commissioner agrees with the taxpayer's NOPA and tax return, the Commissioner will amend the default assessment by exercising the discretion under section 113 subject to the statutory time bar in section 108 and any other relevant limitations on the exercise of that discretion.

- However, if the Commissioner disagrees with the taxpayer's tax return and NOPA the Commissioner cannot amend the default assessment. Instead, the Commissioner must issue a NOR to the taxpayer within the relevant response period to continue the disputes resolution process.

- The taxpayer cannot commence a dispute or challenge proceedings in a hearing authority by simply filing the tax return to which the default assessment relates. If the taxpayer does not want to enter the disputes resolution process they should not issue a NOPA with their tax return.

- If a NOPA is not issued, the Commissioner cannot be compelled to amend the default assessment on receipt of the taxpayer's tax return. However, the Commissioner will amend the assessment under section 113 on the basis of the information provided in the tax return subject to the statutory time bar in section 108 and any other relevant limitations on the exercise of that discretion if this would ensure that the assessment was correct. (Please see SPS 07/03: Requests to amend assessments for further details.) Any amended assessment must be treated as the Commissioner's assessment in this circumstance.

- The Commissioner can decide not to amend the default assessment by exercising the discretion under section 113 on the basis of the tax return provided. For example, if the Commissioner considers that the taxpayer's tax position is incorrect. In this circumstance, the Commissioner can dispute the default assessment by issuing a NOPA in respect of the taxpayer's tax return under section 89B(1).

Situation 3: NOPA in respect of a deemed assessment made under section 80H

- Section 89D(2B) reads:

A taxpayer to whom section 80F applies who has not furnished an amended income statement for an assessment period may dispute a deemed assessment under section 80H only by furnishing an amended income statement for the assessment period.

- Section 89D(2B) applies to a taxpayer who derives income solely from salary, wages, interest and dividends and who will receive an income statement from the Commissioner under section 80D(1).

- Generally, where the taxpayer considers that the income statement is incorrect, they must advise the Commissioner of the reasons and provide the relevant information to correct the income statement under section 80F(1). This must be done within the statutory time limit. That is, the later of:

- the taxpayer's terminal tax date for the tax year to which the income statement relates, and

- two months after the date that the income statement is issued.

- If the taxpayer does not provide the relevant information within the statutory time limit, they will be treated as having filed a tax return under section 80G(2) and made an assessment under section 80H in respect of that income statement. In this case, the date of the deemed assessment under section 80H will be the date that the statutory time limit under section 80F expires.

- Pursuant to section 89D(2B), the taxpayer cannot issue to the Commissioner a NOPA in respect of the deemed assessment made under section 80H without first satisfying their statutory obligation to file an amended income statement for the assessment period.

- If a taxpayer wants to dispute a deemed assessment under section 80H, they must:

- provide an amended income statement for the assessment period, and

- issue a NOPA to the Commissioner in respect of the assessment within the applicable response period (that is, four months after the date that the deemed assessment is issued).

Situation 4: NOPA in respect of a disputable decision that is not an assessment

- Under section 89D(3) a taxpayer can issue a NOPA in respect of a disputable decision that is not an assessment. Section 89D(3) reads:

If the Commissioner:

(a) Issues a notice of disputable decision that is not a notice of assessment; and

(b) The notice of disputable decision affects the taxpayer, -

the taxpayer, or any other person who has the standing under a tax law to do so on behalf of the taxpayer, may issue a notice of proposed adjustment in respect of the disputable decision.

- For the purpose of section 89D(3) a person with standing under a tax law to issue a NOPA on behalf of the taxpayer includes a tax advisor and an approved advisor group.

- Section 3(1) defines a "disputable decision" to include:

- A decision of the Commissioner under a tax law, except for a decision -

- To decline to issue a binding ruling under Part VA ; or

- That cannot be the subject of an objection under Part VIII; or

- That cannot be challenged under Part VIIIA; or

- That is left to the Commissioner's discretion under sections 89K, 89L, 89M(8) and (10) and 89N(3).

- A decision of the Commissioner under a tax law, except for a decision -

- A "decision of the Commissioner under a tax law" generally refers to a tax law that specifically confers a discretion or power on the Commissioner. Paragraph (b)(iii) excludes from the definition of "disputable decision" any decision that cannot be challenged under Part VIIIA.

- For example, if the Commissioner:

- does not exercise the discretion under section 113 to amend a taxpayer's income tax assessment, or

- makes a decision under section 108A(3) regarding the application of the time bar, or

- does not agree to a time bar waiver under section 108B,

section 138E(1)(e)(iv) (within Part VIIIA) provides that this decision cannot be challenged and, therefore, is not a disputable decision for the purposes of section 89D(3). However, under section 89D(1), the taxpayer can issue a NOPA in respect of the initial assessment within the applicable response period if the Commissioner has not previously issued a NOPA in respect of that assessment.

- A decision made by the Commissioner under section 108(2) (to increase an assessment) is not of itself, and in the absence of an assessment, a disputable decision. Any challenge to the correctness of the decision must be brought in the context of a challenge to the assessment itself ( Vinelight Nominees Ltd & Anor v Commissioner of Inland Revenue (No 2) (2005) 22 NZTC 19,519).

- Paragraph (b)(iv) of the definition of "disputable decision" in section 3(1) also excludes any decision that is left to the Commissioner's discretion arising under sections 89K, 89L, 89M(8), (10) and 89N(3). For example, the Commissioner:

- does not exercise the discretion under section 89K(1) in respect of a NOPA that a taxpayer has issued outside the applicable response period. This decision to not exercise the discretion in the taxpayer's favour is not a disputable decision.

- provides the taxpayer with additional information under section 89M(8) after receiving their SOP. The decision to provide this additional information is not a disputable decision.

- The exceptions specified in paragraph (b) of the definition of "disputable decision" ensure that only substantive issues are disputed as disputable decisions and the procedural components of the disputes resolution process do not, in themselves, give rise to disputes although they may be amenable to judicial review.

- The following examples illustrate what is a disputable decision:

- a taxpayer who is a natural person can dispute the Commissioner's decision made under section YD 1 of the Income Tax Act 2007 ("ITA 2007") that they are a New Zealand resident for taxation purposes.

- under section RD 3(5) of the ITA 2007, the Commissioner can determine whether, and to what extent, a payment is subject to PAYE. This determination cannot be challenged by the taxpayer and, therefore, is excluded from the definition of "disputable decision" under section 3(1)(b)(iii). However, an employer or employee can dispute an assessment of tax deductions on the basis that a section RD 3(5) determination on which it is founded is wrong in fact or law.

- The taxpayer must issue the NOPA to the Commissioner within the applicable response period. Generally, this will be within the four-month period that starts on the date that the Commissioner issues the notice of disputable decision or notice revoking or varying a disputable decision that is not an assessment unless the Commissioner allows a late NOPA under section 89K(1).

Situation 5: NOPA in respect of a taxpayer's assessment

- Section 89DA(1) reads:

A taxpayer may issue a notice of proposed adjustment in respect of an assessment made by the taxpayer for a tax year or a GST return period if the Commissioner has not previously issued a notice of proposed adjustment to the taxpayer in respect of the assessment.

- Section 89DA(1) applies to tax on income derived in:

- the 2005-06 and later income years for a taxpayer whose income year is the same as the tax year, and

- the corresponding income year for a taxpayer whose income year is different to the 2005-06 and later tax years.

For tax on income derived in the 2002-03 to 2005-06 income years please see the discussion in SPS 05/04: Disputes resolution process commenced by a taxpayer.

- If a taxpayer needs to file an income tax return they must also make an assessment of their taxable income and income tax liability under section 92(1) unless the Commissioner has previously made an assessment for that tax year (section 92(6)).

- Section 89DA(1) also applies to a taxpayer's GST assessment for a return period that begins on or after 1 April 2005. A taxpayer who has to file a GST return must also make an assessment of the amount of GST payable for the return period under section 92B(1).

- Pursuant to section 89DA(1), a taxpayer can issue to the Commissioner a NOPA in respect of their own tax assessment.

- The taxpayer's NOPA must be issued within the applicable response period as defined in section 3(1). Generally, this will be within the four-month period that starts on the date that the Commissioner receives the taxpayer's assessment unless the Commissioner allows a late NOPA under section 89K(1).

- The date that the Commissioner receives the taxpayer's assessment will be determined under section 14B. For example, under section 14B(8) the Commissioner will receive a NOPA that the taxpayer sends by post on the date that it would have been delivered in the ordinary course of post.

Proposed adjustment – input tax credit

- If a taxpayer receives a taxable supply and does not claim an input tax deduction under section 20(3) of the GST Act, they have several options.

- Firstly, the taxpayer (registered person) can claim an input tax deduction in a later GST return period under section 20(3) of the GST Act within the applicable two-year period. Pursuant to paragraph (a) of the proviso to section 20(3) of the GST Act (appearing after paragraph (i) of the section), the two-year period is calculated from the earlier of the date that:

- a payment is made for the taxable supply to which the input tax credit relates, and

- a tax invoice in relation to that taxable supply is issued.

- However, pursuant to the proviso to section 20(3) of the GST Act, the taxpayer can have unlimited time to claim the input tax credit if their failure to make the deduction under that section arises from any of the following reasons:

- their inability to obtain a tax invoice, or

- a dispute over the proper amount of payment for the taxable supply to which the deduction relates, or

- their mistaken understanding that the supply to which the deduction relates was not a taxable supply, or

- a clear mistake or simple oversight made by the taxpayer.

- Alternatively, the taxpayer can propose an adjustment to the relevant assessment by issuing a NOPA to the Commissioner within the applicable response period.

- If the taxpayer is outside the response period for issuing a NOPA and they have made a genuine error and otherwise satisfy the criteria set out in SPS 07/03: Requests to amend assessments they can request that the Commissioner amends the assessment by exercising the discretion under section 113.

- For example, a taxpayer is registered for GST. They pay GST on an invoice basis and file monthly GST returns. In May 2005, they receive a tax invoice in respect of a taxable supply. However, the taxpayer omits to claim the input tax credit in respect of that taxable supply in the May 2005 GST return period. The omission occurs because the taxpayer has misplaced the tax invoice in one of their business files and only discovers it in December 2007.

- The taxpayer has several options. They can claim an input tax deduction in the current GST return period under section 20(3) of the GST Act. The two-year restriction on claiming the deduction does not apply because the taxpayer's omission is due to their simple oversight.

- Whether a "simple or obvious mistake or oversight" has occurred is determined on a case-by-case basis with no dollar limit. However, "a simple or obvious mistake or oversight" cannot include a taxpayer's GST position that they take as a result of:

- a new, beneficial interpretation of, or favourable new case law, or

- a regretted choice.

- The taxpayer can also propose an adjustment to an input tax credit in the May 2005 GST period by issuing a NOPA to the Commissioner. However, the NOPA will be issued outside the four-month response period unless the Commissioner considers that any of the "exceptional circumstances" in section 89K apply and accepts the late NOPA.

- Alternatively, the taxpayer can request that the Commissioner considers their case in terms of the discretion under section 113 if they have made a genuine error. (Please see SPS 07/03: Requests to amend assessments for details of this practice).

Situation 6: NOPA that relates solely to a research and development tax credit

- Under section 89D, a taxpayer can issue a NOPA that relates solely to a research and development expenditure tax credit arising under section LH 2 of the ITA 2007 in respect of:

- a notice of disputable decision (please see paragraphs 56 to 65), or

- a notice revoking or varying a disputable decision that is not an assessment,

that the Commissioner issues in the 2008-09 or later tax years. In this circumstance section 3(1) provides that the response period for a NOPA that relates solely to a research and development expenditure tax credit is within the one-year period that starts on the date that the Commissioner issues such a notice.

- For example, the Commissioner makes an assessment based on the taxpayer's tax return on 10 August 2009. The taxpayer later seeks to issue a NOPA in respect of the assessment under section 89D(1). The NOPA relates solely to a claim for a research and development expenditure tax credit arising under section LH 2 of the ITA 2007. The taxpayer must issue the NOPA within the one-year period that starts on 10 August 2009 and ends on 9 August 2010.

- Under section 89DA, a taxpayer can also issue a NOPA that relates solely to a research and development expenditure tax credit arising from a notice of assessment that they have previously issued for the 2008-09 or later income years.

- The NOPA must be issued within the period that pursuant to paragraph (e)(i) of the definition of "response period" in section 3(1):

- ends:

- two years (for an assessment that relates to the 2008-09 and 2009-10 income years), or

- one year (for an assessment that relates to the 2010-11 and later income years),

after the date that the Commissioner receives the taxpayer's assessment if the taxpayer is a single person for the purpose of section 68D (that is, not a member of an internal software development group ("ISDG") or partner of a partnership to which section 68E applies), or

- starts on the date on which the Commissioner receives the taxpayer's assessment and ends:

- two years (for an assessment that relates to the 2008-09 and 2009-10 income years), or

- one year (for an assessment relating to the 2010-11 and later income years),

after the latest date on which the taxpayer can provide an income tax or joint income tax return for the relevant tax year under section 37 if the taxpayer is a member of an ISDG or partner of a partnership that chooses to apply section 68E for the 2008-09 and later income years (paragraph (e)(ii) the definition of "response period" in section 3(1)).

- ends:

- For the purpose of paragraphs (d) and (e) of the definition of "response period" in section 3(1) the date that the Commissioner receives the taxpayer's assessment must be determined under section 14B (as discussed in paragraph 72).

- For example, a taxpayer that is a member of an ISDG provides their partnership's 2009 income tax return to the Commissioner on 1 July 2009 which is before the return filing due date of 7 July 2009 under section 37(1)(c). The taxpayer discovers that they have under claimed research and development expenditure tax credits in the assessment in their tax return.

- Under section 89DA, the taxpayer can issue in respect of their assessment a NOPA that relates solely to the claim for a research and development expenditure tax credit. The taxpayer must issue the NOPA within the period that starts on 1 July 2009 (the date that the Commissioner received their assessment) and ends on 6 July 2011 (two years after 7 July 2009 which is the due date for filing the member's income tax return under section 37).

Contents of a taxpayer's NOPA

- A NOPA is the document that commences the disputes resolution process. It is intended to identify the true points of contention and explain the legal or technical aspects of the issuer's position in relation to the proposed adjustment in a formal and understandable manner. This will ensure that information relevant to the dispute is quickly made available to the parties. Section 89F(1) and (3) specifies the content requirements for any NOPA that a taxpayer may issue.

- Section 89F reads:

(1) A notice of proposed adjustment must -

...(a) contain sufficient detail of the matters described in subsections (2) and (3) to identify the issues arising between the Commissioner and the disputant; and

(b) be in the prescribed form.(3) A notice of proposed adjustment issued by a disputant must -

(a) identify the adjustment or adjustments proposed to be made to the assessment; and

(b) provide a statement of the facts and the law in sufficient detail to inform the Commissioner of the grounds for the disputant's proposed adjustment or adjustments; and

(c) state how the law applies to the facts; and

(d) include copies of the documents of which the disputant is aware at the time that the notice is issued that are significantly relevant to the issues arising between the Commissioner and the disputant. - The prescribed form for a NOPA as required under section 89F(3)(b) is the IR770 Notice of proposed adjustment form that can be found on Inland Revenue's website: www.ird.govt.nz. A handwritten NOPA in this form is acceptable. Additional information can also be attached to the prescribed form.

- If the Commissioner receives a NOPA that is not in the prescribed form or has insufficient detail under section 89F(1)(a) the Commissioner's practice will be to advise the taxpayer that the NOPA must be in the prescribed form or include sufficient information. If this occurs on the last day of the response period the Commissioner will consider any resubmitted NOPA under section 89K(1)(a)(iii) provided that the lateness is minimal (please see paragraph 130).

- If the taxpayer's NOPA does not satisfy the content requirements under sections 89F(1)(a) and 89F(3) the Commissioner can reject the NOPA on the basis of the invalidity and not issue a NOR.

- When issuing a NOPA, the taxpayer must state the facts and law in sufficient detail, how the law applies to the facts and include copies of the documents that are significantly relevant to the dispute and known to the taxpayer when they issue the NOPA. However, the taxpayer must avoid repeating facts, arguments or using unnecessary detail. The Commissioner cannot treat a tax return provided by the taxpayer as a NOPA because it will not satisfy the requirements in section 89F(1) and (3).

- Section 89F(3)(b) requires that the taxpayer's NOPA states the key facts and law concisely and in sufficient detail. The term "sufficient detail" means that the document must contain adequate analysis of the law and facts that are relevant to the dispute. This means sufficient discussion of the law to enable the Commissioner to clearly understand the proposed adjustment.

- The Commissioner considers that it is necessary that the taxpayer provides "a statement of the facts and law in sufficient detail" to ensure that they have fully considered issues before they raise them in their NOPA.

- Although not a requirement under section 89F(3) the taxpayer must ensure that a NOPA is relatively brief and simple to enable the parties to quickly progress the dispute without incurring substantial expenses or excessive preparation time. However, the taxpayer must also provide sufficient information to support the proposed adjustments in their NOPA and to reduce further administrative and compliance costs.

Identify the proposed adjustment - section 89F(3)(a)

- The taxpayer must identify the proposed adjustment in their NOPA. This includes for each proposed adjustment:

- the amount or impact of the adjustment, and

- the tax year or period to which the proposed adjustment relates.

- The proposed adjustment should be set out as specifically as possible. For example: "increase the 2007 repairs and maintenance expenditure by $3,000"; "increase the GST input tax deduction by $4,000 in the August 2007 return period", etc.

Provide a statement of the facts and law in sufficient detail - section 89F(3)(b)

Facts

- To provide a brief and accurate statement of facts, the taxpayer must focus on the material factual matters relevant to the legal issues. The taxpayer must include the facts necessary for proving all the arguments raised in support of each adjustment, including any facts that are inconsistent with any argument that the Commissioner has previously raised.

- The taxpayer should endeavour to disclose all the relevant material facts clearly and with adequate amounts of detail relative to the complexity of the issues. The taxpayer is best suited to do this because they are usually very familiar with the background and facts that relate to the dispute. Disclosing the background and facts at the NOPA phase helps to resolve the dispute at an earlier stage. However, the taxpayer should not overstate the facts with irrelevant detail or repetition.

- In complex cases, the Commissioner expects the taxpayer to explain the relevant facts clearly and methodically. The taxpayer should also assist the Commissioner to understand the background and facts of the dispute, so as to facilitate a speedy resolution of the case. The taxpayer should explain the facts and law in sufficient detail to inform the Commissioner of the grounds for the adjustment. It is unhelpful and can cause delays if the Commissioner has to second guess the factual bases of the taxpayer's case.

- For example, in a dispute that involves a complex financial arrangement, the taxpayer should explain each element of it. This includes explaining the background to the financial arrangement, identifying the parties involved, highlighting the relevant clauses in an agreement, etc.

Law

- Each proposed adjustment should stipulate the relevant section or sections that the taxpayer relies on including, if a section has multiple independent parts, the applicable subsection(s).

- It is important that the taxpayer includes an adequate amount of analysis of the applicable legal principles or tests in their NOPA. If possible these should be supported by case authorities with full citations. For example, in a dispute that involves the tax treatment of a trade-tie payment, the taxpayer must apply the legal principles from a leading case such as Birkdale Service Station v CIR (2000) 19 NZTC 15,981. However, it is not necessary to laboriously describe large numbers of precedent cases on the same issue or include extracts from each.

How the law applies to the facts - section 89F(3)(c)

- The taxpayer must apply the legal arguments to the facts. This ensures that the proposed adjustment is not a statement that appears out of context in relation to the rest of the document. The Commissioner considers that the application of the law to the facts must logically support the proposed adjustment and be stated clearly and in detail.

- The taxpayer must present the materials and arguments on which they intend to rely or on which reliance will be placed. That is, if more than one argument supports the same or a similar outcome, all arguments must be made and supported by evidence. For each proposition of law, it is recommended that the NOPA makes a clear link to an outline of supporting facts.

Include copies of the relevant documents that support the adjustment - section 89F(3)(d)

- The taxpayer must provide full copies of the documents that they know are significantly relevant to the dispute and in existence when they issue the NOPA. This ensures that the Commissioner has all the relevant information necessary to respond to the NOPA.

- For example:

- a taxpayer proposes an adjustment to GST input tax credits in their NOPA. The taxpayer must provide copies of the relevant tax invoices as documentary evidence in their NOPA.

- a taxpayer's dispute involves a sale of land transaction. The taxpayer must provide a copy of the sale and purchase agreement and other relevant correspondence between the vendor and the purchaser as documentary evidence in their NOPA.

- However, a NOPA will not necessarily be treated as invalid if the taxpayer has not provided all the documentary evidence with it. In some cases, new documentary evidence can emerge, as the dispute progresses. For example:

- a dispute involves overseas parties who hold relevant documents outside of New Zealand.

- the documentation is quite old and may have been misplaced.

- The taxpayer may be unaware of these documents when the NOPA was issued. The parties should then exchange this new evidence when it becomes known or available.

- Where a taxpayer is aware of a particular document that is significantly relevant to their dispute, but cannot obtain a copy of it, the taxpayer should include the following matters in their NOPA:

- the nature of the document and its relevance to the dispute, and

- the reasonable steps that the taxpayer has taken to obtain a copy of the document, and

- the expected date that the document will be made available to the Commissioner.

- However, the practice allowed in the immediately preceding paragraph should not be treated as dispensing with the requirements under section 89F(3)(d). The Commissioner expects the taxpayer to send copies of the relevant documents mentioned in their NOPA as soon as they become available and can reject the proposed adjustment if they fail to do so.

Election of the small claims jurisdiction of the taxation review authority

- Pursuant to section 89E(1), if a taxpayer issues a NOPA they can elect in that NOPA that the TRA acting in its small claims jurisdiction hears any unresolved dispute that arises from the NOPA, if the following requirements are met:

- the taxpayer's NOPA is issued under section 89D or 89DA (please see earlier discussion), and

- the amount in dispute is $30,000 or less.

- The Commissioner's practice is not to oppose any election made by the taxpayer under section 89E(1), for example where the dispute involves complicated legal issues, because the taxpayer's election is irrevocable and is binding on them. In this circumstance, the full disputes resolution process does not have to be followed.

- Section 89E(1) applies in respect of a disputes resolution process that is commenced under Part IVA on or after 1 April 2005.

Receipt of a taxpayer's NOPA

- Inland Revenue will usually assign a taxpayer's NOPA to the responsible officer within five working days after it is received.

- After receiving the NOPA, the responsible officer will determine and record the following:

- the date on which the NOPA was issued, whether the NOPA has been issued within the applicable response period and the date by which the Commissioner's response must be issued, and

- the NOPA's salient features including any deficiencies in its content.

- Where this is practicable, Inland Revenue will advise the taxpayer or their tax agent that it has received the NOPA by telephone or in writing within 10 working days.

Deficiencies in the contents of a NOPA

- If Inland Revenue has received a NOPA that it considers has deficiencies (that is, it has not satisfied the requirements under section 89F(1)(a) and (3)), the responsible officer must take reasonable steps to ensure that the taxpayer can correct the information in the NOPA before the response period expires.</<BR>

- Any decision regarding the NOPA's validity made by the Commissioner must be based on reasonable grounds. For example, where the Commissioner treats the NOPA as invalid because there is insufficient information to allow the Commissioner to make an informed decision regarding the assessment. The taxpayer must be advised as soon as practicable that the NOPA is invalid unless rectified and the additional or correct information must be provided within the remainder of the response period.

- Taxpayers are encouraged to issue their NOPA immediately after they have completed it because they could have insufficient time to rectify any deficiency or invalidity if the response period is about to expire.

- If the Commissioner does not accept that a NOPA is valid because it has deficiencies and the information is not corrected before the response period expires, the dispute will be treated as if it has never been commenced (unless the taxpayer resubmits a late NOPA and the Commissioner accepts it under one of the exceptional circumstances under section 89K).

- The responsible officer will document the reasons for not accepting a NOPA and advise the taxpayer of these reasons in writing immediately if the taxpayer is still within the response period or 15 working days after the response period for issuing the taxpayer's NOPA expires if there is insufficient time for the taxpayer to resubmit the NOPA.

NOPA that a taxpayer has issued outside the applicable response period

- Unless an "exceptional circumstance" arises under any of the circumstances specified in section 89K(1) in respect of a dispute that was commenced on or after 1 April 2005, the Commissioner cannot accept a NOPA that a taxpayer issues under section 89D or 89DA outside the applicable response period.

Exceptional circumstances under section 89K

- The legislation defines exceptional circumstances very narrowly. The cases on "exceptional circumstances", such as Treasury Technology Holdings Ltd v CIR (1998) 18 NZTC 13,752, Milburn NZ Ltd v CIR (1998) 18 NZTC 14,005, Fuji Xerox NZ Ltd v CIR (2001) 17,470 (CA), Hollis v CIR (2005) 22 NZTC 19,570, and Balich v CIR (2007) 23 NZTC 21,230 are also relevant. The case law confirms that the Commissioner should apply the definition of “exceptional circumstances” in sections 89K(3) and 138D consistently.

The following guidelines have emerged from the case law:- a taxpayer's misunderstanding or erroneous calculation of the applicable response period will usually not be regarded as an event or circumstance beyond the taxpayer's control under section 89K(3)(a)

- an agent's failure to advise their client that they have received a notice of assessment or other relevant documents that causes the taxpayer to respond outside the applicable response period will not generally be considered to be an exceptional circumstance under section 89K(3)(b) (Hollis v CIR)

- an exceptional circumstance can arise if the taxpayer has relied on misleading information that the Commissioner has given them that causes them to respond outside the applicable response period (Hollis v CIR)

- The Commissioner will only accept a late NOPA on rare occasions. Please see Tax Information Bulletin Vol 8, No 3 (August 1996) for some examples of situations that can be considered “exceptional circumstances” beyond a taxpayer's control.

- Section 89K(3) reads:

an exceptional circumstance arises if-

(i) an event or circumstance beyond the control of a disputant provides the disputant with a reasonable justification for not rejecting a proposed adjustment, or for not issuing a notice of proposed adjustment or statement of position, within the response period for the notice:

(b) an act or omission of an agent of a disputant is not an exceptional circumstance unless-

(ii) a disputant is late in issuing a notice of proposed adjustment, notice of response or statement of position but the Commissioner considers that the lateness is minimal, or results from 1 or more statutory holidays falling in the response period:(i) it was caused by an event or circumstance beyond the control of the agent that could not have been anticipated, and its effect could not have been avoided by compliance with accepted standards of business organisation and professional conduct; or

(ii) the agent is late in issuing a notice of proposed adjustment, notice of response or statement of position but the Commissioner considers that the lateness is minimal, or results from 1 or more statutory holidays falling in the response period. - The statutory holiday exception is self-explanatory. The Commissioner can also accept a late NOPA if the Commissioner considers that the lateness is minimal, that is, the document was only one to two days late.

- For example, the response period ends on a Saturday and the taxpayer provides a NOPA on the following Tuesday. The Commissioner treats the response period as ending on Monday on the basis of section 35(6) of the Interpretation Act 1999 and accepts that the lateness of the NOPA was minimal. That is, the Commissioner received the NOPA within one to two days of Monday, the last day of the response period. If the response period ended on Friday and the taxpayer provided the NOR on the following Monday, the Commissioner would also accept that the lateness is minimal.

- Besides the degree of lateness, the Commissioner will consider the following factors when exercising the discretion under section 89K(1):

- the date on which the NOPA was issued, and

- the response period within which the NOPA should be issued, and

- the real event, circumstance or reason why the taxpayer did not issue the NOPA within the applicable response period, and

- the taxpayer's compliance history in relation to the tax types under consideration (for example, whether the taxpayer has a history of paying tax late or filing late tax returns or NOPAs in the past?).

- For example, a taxpayer issues a NOPA to the Commissioner two days after the applicable "response period" has expired. The taxpayer does not provide a legitimate reason for the lateness. The taxpayer also has a history of filing late NOPAs within the minimal allowable lateness period (that is, up to two days outside the applicable "response period") and has been advised on the calculation of the "response period" each time.

- Although the degree of lateness was minimal each time, the Commissioner would not accept the taxpayer's NOPA in this circumstance. This ensures that the section 89K(3)(b)(ii) exception is not treated as an extension of the "response period" in all circumstances.

- The Commissioner will consider a taxpayer's application made under section 89K(1) after receiving the relevant NOPA. The responsible officer will document the reasons for accepting or rejecting the taxpayer's application and advise them of their decision in writing within 15 working days after Inland Revenue receives their application.

- If the Commissioner rejects a taxpayer's application made under section 89K(1), the Commissioner can still consider the validity of the taxpayer's tax position in terms of the practice for applying the discretion under section 113. Please see SPS 07/03: Requests to amend assessments for details of this practice. However, the Commissioner's decision to reject an application made under section 89K(1) is not a "disputable decision" for the purposes of section 89D(3).

Time frames to complete the disputes resolution process

- If a taxpayer has issued a NOPA to the Commissioner and the dispute remains unresolved, when practicable, the parties should negotiate a time line to ensure that the dispute is progressed in a timely and efficient way.

- Agreeing to a time line is not statutorily required but, rather, is a critical administrative requirement that requires both parties to be ready to progress matters. The parties should endeavour to meet the agreed time line. If there are delays in the progress of the dispute the responsible officer must manage the delay including any relationship with internal advisers and liaise with the taxpayer.

- If the negotiated time line cannot be achieved, the Commissioner must enter into continuing discussions with the taxpayer to, either arrange a new time line, or otherwise keep them advised of when the disclosure notice will be issued. Therefore, the failure to negotiate or adhere to an agreed time line will not prevent the case from progressing through the disputes resolution process in a timely manner.

- In addition to the above administrative practice, the Commissioner is bound by section 89N. Under section 89N(2), if the parties cannot agree on the proposed adjustment, the Commissioner cannot amend the assessment without completing the disputes resolution process (that is, consider the taxpayer's SOP), unless any of the exceptions in section 89N(1)(c) apply. These exceptions are explained in SPS 08/01: Disputes resolution process commenced by the Commissioner of Inland Revenue.

- Although not a statutory requirement of the disputes resolution process, when practicable, it is the Commissioner's administrative practice to go through the adjudication phase for the purpose of resolving the dispute after the SOP phase.

- However, if the adjudication phase cannot be completed (for example, because the statutory time bar is imminent), the Commissioner can amend the assessment under section 113 after considering the taxpayer's SOP. Inland Revenue officers will adequately consider the facts and legal arguments in the taxpayer's SOP before deciding whether to amend the assessment. It is expected that this will occur only in very rare circumstances.

- Whether the Commissioner has adequately considered a SOP will depend on what is a reasonable length of time and level of analysis for that SOP given the circumstances of the case (for example, the length of the SOP and the complexity of the legal issues).

- Thus a simple dispute could take only a couple of days to consider adequately while a complex dispute could take a few weeks. If the statutory time bar is imminent the Inland Revenue officer will consider the taxpayer's SOP urgently.

- If the Commissioner issues an amended assessment because section 89N(1)(c) or 89N(2)(b) applies (please see the discussion in SPS 08/01: Disputes resolution process commenced by the Commissioner of Inland Revenue) the disputes resolution process will end and the dispute will not go through the adjudication phase. Any decision that the Commissioner makes under section 89N(1)(c) is a disputable decision for the purpose of section 89D(3).

The Commissioner's response to a taxpayer's NOPA: Notice of response

- If the Commissioner disagrees with the taxpayer's proposed adjustment, then, under section 89G(1) the Commissioner must advise the taxpayer that any or all of their proposed adjustments are rejected by issuing a NOR within the applicable response period. That is, within two months starting on the date that the taxpayer's NOPA is issued. The Commissioner interprets this to mean that the taxpayer must receive the NOR within this period. For example, if a taxpayer issues a NOPA on 8 April 2007, the Commissioner must advise the taxpayer of its rejection by issuing to them a NOR and they must receive that NOR on or before 7 June 2007.

- Where it is practicable, the Commissioner will make reasonable efforts to contact the taxpayer or their tax agent within 10 working days before the response period expires to advise whether the Commissioner intends to issue a NOR to them in response to their NOPA. Such contact may be made by telephone or letter.

- The Commissioner must issue the NOR to the taxpayer (section 14(3)(a)) or a representative authorised to act on their behalf (section 14(3)(b)). In respect of the latter, it is a question of fact whether the recipient is authorised to receive the NOR on the taxpayer's behalf. The taxpayer must ensure that their NOPA stipulates the name of the person or agent that they have nominated to receive any NOR issued by the Commissioner (CIR v Thompson (2007) 23 NZTC 21,375).

- For example, a tax agent sends a NOPA to the Commissioner. Although the tax agent would appear to have ostensible authority to receive the Commissioner's NOR, the Commissioner's practice will be to contact the tax agent to confirm whether the agent can accept service of the NOR. Therefore, the Commissioner must ensure that a NOR issued in accordance with section 14(3)(b) complies with any relevant instructions given by the taxpayer or the recipient's authority to receive can otherwise be verified.

- Section 89G(2) specifies the content requirements for a NOR. The Commissioner must state concisely in the NOR:

- the facts or legal arguments in the taxpayer's NOPA that the Commissioner considers are wrong, and

- why the Commissioner considers that those facts and arguments are wrong, and

- any facts and legal arguments that the Commissioner relies upon, and

- how the legal arguments apply to the facts, and

- the quantitative adjustment to any figures proposed in the taxpayer's NOPA that results from the facts and legal arguments that the Commissioner relies upon.

- Under section 89G(2)(e), the requirement for a quantitative adjustment establishes the extent to which the Commissioner considers that the adjustment in the taxpayer's NOPA is incorrect. This amount need not be exact, although, every attempt should be made to ensure that it is as accurate as possible. The amount in dispute can be varied, as the dispute progresses. For example, if the parties agree on new figures at the conference phase.

- The Commissioner considers that Inland Revenue has a statutory obligation to inform the taxpayer adequately. Therefore, any NOR that the Commissioner issues to reject the adjustment proposed in the taxpayer's NOPA must be relatively brief but sufficiently detailed to explain all the relevant facts, quantitative adjustments, issues and law.

Deemed acceptance

- Section 89H(2) reads:

If the Commissioner does not, within the response period for a notice of proposed adjustment issued by a disputant, reject an adjustment contained in the notice, the Commissioner is deemed to accept the proposed adjustment and section 89J applies.

- If the Commissioner issues a NOR outside the two-month response period, the Commissioner is deemed to have accepted the adjustment proposed in the taxpayer's NOPA under section 89H(2). This will finish the dispute and the Commissioner must issue an assessment or amended assessment to the taxpayer pursuant to section 89J(1) (please see the discussion in paragraphs 159 to 162).

- However, the Commissioner is not precluded from later exercising the discretion under section 113 and issuing to the taxpayer an amended assessment that reflects another adjustment for a different issue to that previously accepted under section 89H(2) for the same tax period.

Exception to deemed acceptance

- Notwithstanding section 89H(2), the Commissioner can apply to the High Court for an order that a NOR can be issued outside the two-month response period under section 89L(1). Section 89L only applies if an exceptional circumstance has occurred or prevented the Commissioner from issuing a NOR to the taxpayer within the response period. The Commissioner will endeavour to apply the requirement for exceptional circumstances in section 89L(1)(a) consistently with the similar requirement in section 89K(1)(a) (please see discussion in paragraphs 127 to 136).

- Under section 89L(3), an "exceptional circumstance":

- is an event or circumstance beyond the control of the Commissioner or an officer of the Department that provides the Commissioner with a reasonable justification for not rejecting an adjustment proposed by a disputant within the response period; and

- Without limiting paragraph (a), includes a change to a tax law, or a new tax law, or a decision of a court in respect of a tax law, that is enacted or made within the response period.

- For example:

- A flood damaged an Inland Revenue office during the applicable response period for a taxpayer's NOPA. The taxpayer's NOPA was lost in the flood. The Inland Revenue officer could not obtain another copy of the NOPA within the applicable response period. The absence of information has prevented the Commissioner from forming a view on the subject matter in dispute. The Commissioner can apply for a High Court order under section 89L for further time to issue a NOR.

- A taxpayer issues to the Commissioner a NOPA that claims additional tax depreciation on computer software. During the two-month response period, a High Court decision was made in respect of another taxpayer. The High Court held that a depreciation claim amounted to tax avoidance and should be disallowed. The Commissioner can apply to the High Court for further time to issue a NOR to the taxpayer, so as to consider the full effect of the High Court decision.

- The Inland Revenue officer to whom a taxpayer's NOPA was assigned is absent on annual leave for the remainder of the response period. The Inland Revenue officer does not arrange for another officer to prepare and issue a NOR to the taxpayer within the response period. The Commissioner is deemed to accept the NOPA under section 89H(2). In this circumstance, the Commissioner does not consider that an exceptional circumstance prevented the Inland Revenue officer from rejecting the adjustment within the response period for the purpose of section 89L(1)(a).

Implication of section 89J

- Pursuant to section 89J(1), if the Commissioner accepts or is deemed to accept any adjustment that is proposed in a taxpayer's NOPA, the Commissioner must include or take account of the adjustment in:

- a notice of assessment, and

- any further notice of assessment or amended assessment,

that is issued to the taxpayer unless the Commissioner has applied to the High Court for an order that a notice can be issued rejecting the proposed adjustment under section 89L(1).

- In this circumstance, the Commissioner's practice will be to not later issue a NOPA that purports to reverse any proposed adjustment previously accepted under section 89H(2) because section 89J(1) prevents the Commissioner from issuing to the taxpayer a further amended assessment that does not include or take into account the previously accepted adjustment.

- However, pursuant to section 89J(2) the Commissioner can issue a notice of assessment or amended assessment that does not include or take into account an adjustment that the Commissioner has, or is deemed to have accepted, if the Commissioner considers that, in relation to the adjustment, the taxpayer:

- was fraudulent, or

- wilfully misled the Commissioner.

- If the Commissioner considers that section 89J(2) applies following a deemed acceptance under section 89H(2) the Commissioner cannot resume the earlier disputes resolution process but can later issue a NOPA in respect of any of the adjustments proposed in the earlier disputes resolution process.

- Pursuant to section 89J(2), the Commissioner must decide whether any of the exceptions to section 89J(1) apply before an assessment or amended assessment that does not include an adjustment that the Commissioner has, or is deemed to have accepted can be issued.

- Any opinion that the Commissioner forms under section 89J(2) must be honestly held, based on a correct understanding of the relevant grounds and reasonably justifiable on the basis of the facts and law available. An opinion formed by the Commissioner under section 89J(2) is a disputable decision for the purposes of section 89D(3).

Rejection of the Commissioner's notice of response

- If the Commissioner has issued a NOR under section 89G(1) that rejects the adjustment proposed in the taxpayer's NOPA, the taxpayer must reject the Commissioner's NOR within the applicable response period. That is, within two months starting on the date that the Commissioner issues the NOR. Otherwise, the taxpayer is deemed to have accepted the Commissioner's NOR under section 89H(3) and the dispute will finish.

- The Commissioner will make reasonable efforts to contact the taxpayer or their tax agent two weeks before the response period for the Commissioner's NOR expires to determine whether the taxpayer will reject the Commissioner's NOR in writing. Such contact can be made by telephone or in writing.

- The taxpayer must reject the Commissioner's NOR in writing. The written rejection must be issued within the response period and can be in any form. The taxpayer does not have to expressly reject each of the rejections of proposed adjustments that are included in the Commissioner's NOR. The taxpayer's written rejection must simply make it clear that the taxpayer rejects the Commissioner's NOR.

- For example, in certain circumstances, the Commissioner can treat a notice of proceedings and statement of claim that the taxpayer serves on the Commissioner within the response period to commence challenge proceedings as a valid rejection in writing of the Commissioner's NOR under section 89H(3)(a). However, if the parties do not agree to suspend the dispute under section 89N(1)(c)(viii) the Commissioner must issue a disclosure notice and the taxpayer must issue a SOP in response within the applicable response period to continue the disputes resolution process.

- Where it is practicable, the taxpayer's written rejection will be referred to the responsible officer within five working days after Inland Revenue has received it and acknowledged as received within 10 working days.

- If deemed acceptance occurs (that is, the taxpayer has not rejected the Commissioner's NOR in writing), the Commissioner will make reasonable efforts to advise the taxpayer of this within two weeks after the response period to the Commissioner's NOR has expired.

Conference

Conduct of a conference

- Generally, if a dispute remains unresolved after the Commissioner's NOR has been rejected, the conference phase will follow. The Commissioner will usually commence the conference phase in a timely manner, that is, within one month after receiving the taxpayer's notice rejecting the Commissioner's NOR. However, the Commissioner must not endeavour to advance the disputes resolution process by initiating the conference phase before the taxpayer's rejection of the NOR has been fully considered.

- If the start of the conference phase is delayed (for example to obtain legal advice) the responsible officer will keep the taxpayer informed regarding the progress of the conference. The suggested average time frame for the conference phase is three months. However, this time frame will vary depending on the facts and complexity of the specific case.

- A conference is not statutorily required. Rather, the conference phase is an administrative process that aims to clarify and, if possible, resolve the disputed issue by conducting an open discussion. However, the conference phase should not be used by either party to the dispute for the purpose of delaying the completion of the disputes resolution process.

- The conference should be conducted in a way that is sufficiently flexible and consistent with the taxpayer's wishes and any other relevant factors such as the scope of the investigation. The Commissioner will establish a time frame to meet with the taxpayer and any advisors and, sometimes, if necessary, Inland Revenue officers will meet with the taxpayer immediately after considering further information. Where appropriate a conference can be adjourned to allow the parties to reconsider the position that they have taken in the dispute.

- A conference can range from telephone calls to several face-to-face meetings between the parties. If the parties are relying on expert evidence the expert may also attend the conference. All discussions in the conference must be recorded or otherwise documented (to provide the best record of such discussions and promote the free flow of conversation) and a consensus reached if possible.