Disputes resolution process commenced by the Commissioner of Inland Revenue (November 2010) (WITHDRAWN)

Withdrawn SPS 10/04 Disputes resolution process commenced by the Commissioner of Inland Revenue (Nov 2010). Statement provided for historical purposes only.

Withdrawn

This statement has been withdrawn and is provided for historical purposes only.

This item also appears in Tax Information Bulletin Vol. 22, No. 11 (December 2010).

Introduction

- This Standard Practice Statement ("SPS") sets out the Commissioner's rights and responsibilities with a taxpayer in respect of an adjustment to an assessment when the Commissioner commences the disputes resolution process.

- Unless specified otherwise, all legislative references in this SPS refer to the Tax Administration Act 1994 ("TAA").

- Where a taxpayer commences the disputes resolution process, the Commissioner's practice is set out in SPS 10/05 Disputes resolution process commenced by a taxpayer.

- The Commissioner regards this SPS as a reference guide for taxpayers and Inland Revenue officers. Where possible, Inland Revenue officers must follow the practices outlined in this SPS.

- The disputes resolution process is designed to ensure that there is a full and frank communication between the parties in a structured way within strict time limits for the legislated phases of the process.

- The disputes resolution process is designed to encourage an "all cards on the table" approach and the resolution of issues without the need for litigation. It aims to ensure that all the relevant evidence, facts and legal arguments are canvassed before a case proceeds to a court.

- In accordance with the objectives of the disputes resolution process, the Commissioner (unless a statutory exception applies under section 89C or 89N(1)(c)) must go through the disputes resolution process before the Commissioner can issue an assessment.

Application

- This SPS applies from 8 November 2010 and incorporates changes made to the Commissioner's administrative practice in relation to the disputes process which were implemented by Inland Revenue on 1 April 2010.

- It replaces SPS 08/01: Disputes resolution process commenced by the Commissioner of Inland Revenue.

- We acknowledge that Inland Revenue issued an officials' issues paper entitled "Disputes: a review" in July 2010. However, the outcome of that review has yet to be finally determined. This SPS represents the law and the Commissioner's administrative practice as it currently stands. If changes to the law and/or the Commissioner's administrative practice arise out of "Disputes: a review" this SPS will be reviewed and amended to reflect those changes.

Background

- The tax disputes resolution procedures were introduced in accordance with the recommendations of the Richardson Committee in the Report of the Organisational Review of the Inland Revenue Department (April 1994) and were designed to reduce the number of disputes by:

- promoting full disclosure, and

- encouraging the prompt and efficient resolution of tax disputes, and

- promoting the early identification of issues, and

- improving the accuracy of decisions.

- The disputes resolution process ensures that there is a full and frank communication between the parties in a structured way within strict time limits for the legislated phases of the process.

- The disputes resolution process is designed to encourage an "all cards on the table" approach and the resolution of issues without the need for litigation. It aims to ensure that all the relevant evidence, facts and legal arguments are canvassed before a case goes to a court or hearing authority.

- In accordance with the objectives of the disputes resolution process, the Commissioner (unless a statutory exception applies under section 89C or 89N(1)(c)) must go through the disputes resolution process before the Commissioner can issue an assessment.

- The early resolution of a dispute is intended to be achieved through a series of steps specified in the TAA. The main elements of those steps are the issue of:

- A notice of proposed adjustment ("NOPA"): this is a notice that either the Commissioner or taxpayer issues to the other advising that an adjustment is sought in relation to the taxpayer's assessment, the Commissioner's assessment or other disputable decision (the prescribed form is the IR 770 Notice of proposed adjustment). A NOPA is the formal document which begins the disputes process.

- A notice of response ("NOR"): this must be issued by the recipient of a NOPA if they disagree with it (the preferred form is the IR 771 Notice of response).

- A disclosure notice and statement of position ("SOP"): the issue of a disclosure notice and SOP by the Commissioner triggers the requirement for the taxpayer to provide a SOP to continue the dispute. . Each SOP must provide an outline of the facts, evidence, issues and propositions of law with sufficient details to support the positions taken. Each party must issue a SOP (the preferred form is the IR 773 Statement of position). The SOPs are important documents because they limit the facts, evidence, issues and propositions of law that either party can rely on if the case proceeds to court to what is included in the SOP (unless a hearing authority makes an order that allows a party to raise new facts or evidence under section 138G(2)).

- There are also two administrative phases in the disputes process - the conference and adjudication phases. If the dispute has not been already resolved after the NOR phase, the Commissioner's practice will be to hold a conference. A conference can be a formal or informal discussion between the parties to clarify and, if possible, resolve the issues.

- If the dispute remains unresolved after the conference phase, the Commissioner will prepare a SOP and refer the dispute to adjudication, except in certain circumstances. One of the circumstances where the Commissioner will not refer a dispute to adjudication is where the Commissioner and the taxpayer have agreed in writing not to complete the disputes process (referred to as "opt out" (see paragraphs 261 to 285).

- Adjudication involves an independent review of the dispute by Inland Revenue's Adjudication Unit, which was formed to provide an internal but impartial review of unresolved disputes. Adjudication is the final phase in the disputes process before the taxpayer's assessment is amended (if it is to be amended) following the exchange of the SOPs.

- Timely progression of disputes through the disputes process may require the use of the Commissioner's information gathering powers (particularly section 17) before and/or during the disputes process.

- Inland Revenue has a quality assurance review process known as Core Task Assurance ("CTA") which is designed to ensure that key pieces of work (including NOPAs and SOPs) are subject to an independent review by Legal & Technical Services ("LTS") before being issued. Given the importance of the disputes process to the Commissioner and to taxpayers, Inland Revenue officers are required to get CTA approval of disputes documents prior to issue.

Glossary

- The following abbreviations are used throughout this SPS:

- NOPA - Notice of Proposed Adjustment

- NOR - Notice of Response

- SOP - Statement of Position

- Disputes Process - Disputes Resolution Process

- TRA - Taxation Review Authority

Contents

Disputes resolution process commenced by the Commissioner of Inland Revenue

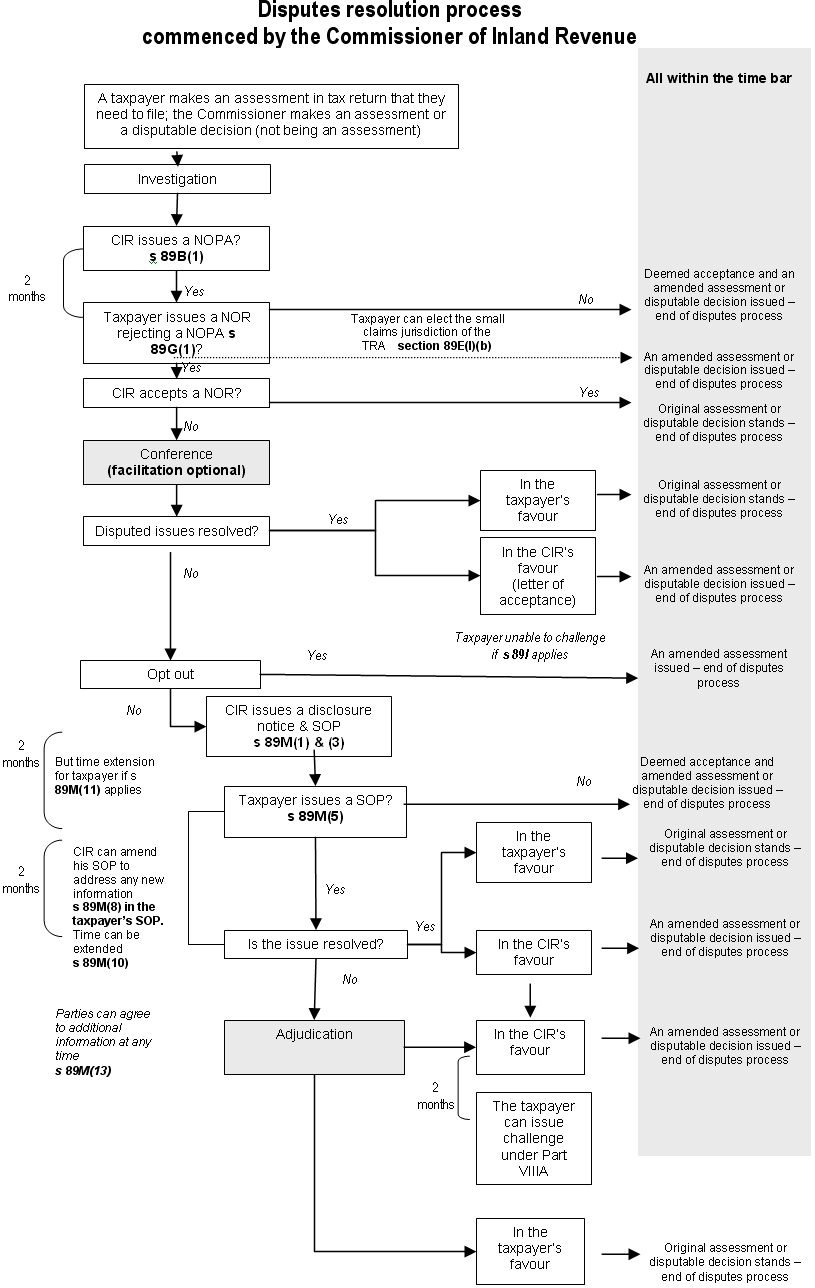

The disputes process is set out in the following diagram.

Summary of key actions and indicative administrative timeframes

- Set out below is a summary of the key actions and administrative timeframes where the disputes process is commenced by the Commissioner of Inland Revenue.

- These key actions and timeframes are intended to be administrative guide lines for Inland Revenue officers. Any failure to meet these administrative timeframes will not invalidate subsequent actions of the Commissioner or prevent the case from going through the disputes process.

| Paragraph in the SPS | Key actions | Indicative time frames |

|---|---|---|

| The Commissioner's NOPA | ||

| 94 | The Commissioner will advise the taxpayer that a NOPA will be issued. | Usually within five working days before the date that the Commissioner issues a NOPA, but this may happen earlier. |

| 99 | The Commissioner will confirm whether the taxpayer has received the Commissioner's NOPA (either by telephone or in writing). | Within 10 working days from the date that the Commissioner's NOPA is issued, where practicable. |

| Taxpayer's NOR | ||

| 196 | The taxpayer issues a NOR in response to the Commissioner's NOPA within the applicable response period. | Within two months from the date that the Commissioner's NOPA is issued, unless any of the "exceptional circumstances" under section 89K applies. |

| 198 | The Commissioner will confirm whether the taxpayer will issue a NOR. | Usually two weeks before the response period for the Commissioner's NOPA expires. |

| 216 | The Commissioner will forward the taxpayer's NOR to the responsible officer. | Usually within five working days after the taxpayer's NOR is received. |

| 217 | The Commissioner will acknowledge the receipt of the taxpayer's NOR. | Usually within 10 working days after the taxpayer's NOR is received. |

| 222 | The Commissioner will advise that the taxpayer's NOR is deficient, but the two-month response period has not expired. | Inland Revenue officers will advise the taxpayer or their agent immediately after they become aware of the deficiency. |

| 213 | The Commissioner will consider the application of "exceptional circumstances" under section 89K, where a taxpayer's NOR has been issued outside the applicable response period. | Usually within 15 working days after the taxpayer's application is received. |

202 | The taxpayer is deemed to accept the Commissioner's NOPA, because they failed to issue a NOR within the applicable response period and none of the "exceptional circumstances" apply in the case of a late NOR. | At the end of the two month period starting on the date of issue of the Commissioner's NOPA. |

| 202 | The Commissioner will advise the taxpayer in writing that they are deemed to accept the Commissioner's NOPA. | Usually two weeks after the response period to the Commissioner's NOPA has expired. |

| 218 | The Commissioner will advise the taxpayer whether their NOR is being considered, has been accepted, or rejected in full or part. | Usually within one month after the taxpayer's NOR is received. |

219 | If the taxpayer's NOR has been accepted in full, the dispute finishes and Inland Revenue will take appropriate actions (for example, issue an amended assessment). | Usually within one month after the advice of acceptance of the NOR is issued. |

| Conference phase | ||

| 236 | The Commissioner will write to the taxpayer to initiate the conference phase and to offer a facilitated conference. | The Commissioner's offer of a facilitated conference will be made in writing within one month from the date of issue of the taxpayer's NOR. The conference letter marks the start of the conference phase. |

| 238 | The taxpayer will advise Inland Revenue whether they will attend the conference meeting, and whether they will accept the conference facilitation offer. | Usually within two weeks of receipt of the conference facilitation letter. If the taxpayer does not respond within this timeframe, the Inland Revenue officers involved in the dispute will contact the taxpayer about the letter. |

| 239 | When a taxpayer agrees to attend a conference meeting, Inland Revenue will contact the taxpayer to establish a timeframe, and agree on how the meeting will be conducted. | Usually within two weeks following the taxpayer's agreement to a conference. |

| 243 | Conference meeting(s) and further information exchange between Inland Revenue and the taxpayer. | The suggested average timeframe of the conference phase is three months, subject to the facts and complexity of the dispute. |

| Opt out | ||

268 | The taxpayer may request to opt out of the disputes resolution process | Within two weeks from the end of the conference phase. |

| 268 | Inland Revenue officer will advise the taxpayer whether the request to opt out has been agreed to. | Usually within two weeks from the date of the taxpayer's request to opt out. |

| Disclosure notice and the Commissioner's SOP | ||

| 301 | The Commissioner will advise the taxpayer that a disclosure notice and the Commissioner's SOP will be issued. | Usually within two weeks before the date that the Commissioner's disclosure notice and SOP are issued. |

| 310 | The Commissioner will issue a disclosure notice and the Commissioner's SOP. | Usually within three months from the end of the conference phase or within three months from the date when the Commissioner advises that the taxpayer's opt out request has been declined. |

| Taxpayer's SOP | ||

| 332 | The taxpayer must issue a SOP within the response period for the disclosure notice. | Within two months after the date that the disclosure notice is issued, unless any of the "exceptional circumstances" under section 89K apply. |

| 335 | The Commissioner will confirm whether the taxpayer will issue a SOP. | Usually two weeks before the response period for the Commissioner's disclosure notice expires. |

| 336 | The taxpayer's SOP is forwarded to the responsible officer. | Usually within five working days after the taxpayer's SOP is received. |

| 337 | The Commissioner will acknowledge the receipt of the taxpayer's SOP. | Usually within 10 working days after the taxpayer's SOP is received. |

| 337 | The Commissioner will advise that the taxpayer's SOP is deficient, but the two-month response period has not expired. | Inland Revenue officers will advise the taxpayer or their agent as soon as they become aware of the deficiency. |

| 338 | The Commissioner will consider the application of "exceptional circumstances" under section 89K, where the taxpayer's SOP has been issued outside the applicable response period. | Usually within 15 working days after the taxpayer's application is received. |

| 339 | The Commissioner will advise that taxpayer is deemed to accept the Commissioner's SOP, because they failed to issue a SOP within the applicable response period and none of the "exceptional circumstances" apply. | Usually two weeks after the response period for the disclosure notice expires. |

| Addendum to the Commissioner's SOP | ||

340 | The Commissioner can provide additional information via an addendum to the Commissioner's SOP under section 89M(8) within the response period for the taxpayer's SOP. | Within two months after the taxpayer's SOP is issued. |

343 | The Commissioner will advise the taxpayer whether additional information to the Commissioner's SOP will be provided via an addendum under section 89M(8). | Usually within two weeks after the taxpayer's SOP is received, subject to the facts and complexity of the dispute and the available response period. |

345 | The Commissioner will consider the taxpayer's request to include additional information in their SOP under section 89M(13). | Usually within one month after the date that the Commissioner's addendum is issued. |

| Adjudication | ||

| 358 | The Commissioner will prepare a cover sheet and issue a letter (including a copy of the cover sheet) to the taxpayer to seek their concurrence of the materials to be sent to the adjudicator. | Usually within one month after the date that the Commissioner's addendum (if any) is issued or within one month from the date that the response period for the taxpayer's SOP to expire. |

| 359 | The taxpayer must respond to the Commissioner's letter. | Within 10 working days after the date that the Commissioner's letter is issued. |

| 360 | The Commissioner will forward materials relevant to the dispute to the Adjudication Unit. | Usually after the taxpayer has concurred on the materials to be sent to the Adjudication Unit or after the 10 working days allowed for the taxpayer's response have elapsed if no response is received. |

352 | Adjudication of the disputes case | Usually within 3 months after the date that the Adjudication Unit receives the dispute files depending on the number of disputes that are before the Adjudication Unit, any allocation delays and the technical, legal and factual complexity of those disputes. |

Standard Practice and Analysis

The Commissioner must issue a NOPA before making an assessment

- The Commissioner must issue a NOPA before making an assessment (including an assessment of shortfall penalties but excluding other civil penalties and interest), unless an exception to the requirement that a NOPA be issued applies under section 89C.

- Nevertheless, even if the Commissioner, in a very unlikely event, made an assessment in breach of section 89C, the assessment would be regarded as being valid under section 114(a).

- Each exception under section 89C can apply independently or together depending on the circumstances. However, the Commissioner can also choose to issue a NOPA before making an assessment notwithstanding that an exception under section 89C applies.

A disputable decision

- Pursuant to the definition in section 3(1), a disputable decision is:

- an assessment, or

- a decision that the Commissioner makes under a tax law, except for a decision:

- to decline to issue a binding ruling, or

- that cannot be the subject of an objection or challenge, or

- that is left to the Commissioner's discretion under sections 89K, 89L, 89M(8), (10) and 89N(3).

- The Commissioner will generally issue a NOPA before issuing an assessment that takes into account a disputable decision.

- For example, the Commissioner issues a notice of disputable decision to a taxpayer who is a director and shareholder of a company advising that the company's loss attributing qualifying company election for the 2007 tax year is invalid because it is received late. However, the company's loss calculation and assessment for the 2007 tax year are not affected. The Commissioner intends to issue an assessment to the taxpayer that takes into account the notice of disputable decision by disallowing the company's losses that the taxpayer has claimed. The Commissioner will issue a NOPA to the taxpayer before making the assessment.

Exceptions

Exception 1: The assessment corresponds with a tax return

- Section 89C(a) reads:

The assessment corresponds with a tax return that has been provided by the taxpayer.

- The application of section 89C(a) is limited under the self-assessment rules. Generally, a taxpayer makes an assessment and files a tax return that includes that assessment. If the taxpayer's assessment is supported by the information in the tax return and any underlying source documents that the taxpayer has provided and the Commissioner agrees with the taxpayer's return and assessment there is no need for the Commissioner to invoke the disputes process.

- In these circumstances, instead of issuing a notice of assessment the Commissioner will issue a statement of account that confirms the taxpayer's assessment. The statutory response period for the purposes of the disputes process will commence from the date that Inland Revenue receives the taxpayer's assessment.

- Sometimes, if there is a deficiency in the taxpayer's tax return, the Commissioner will issue an assessment without first issuing a NOPA to the taxpayer because section 89C(a) applies. For example, the Commissioner can issue an assessment, where the taxpayer has provided all their income details but omitted to calculate their income tax liability in the tax return.

Exception 2: Simple or obvious mistake or oversight

- Section 89C(b) reads:

The taxpayer has provided a tax return which, in the Commissioner's opinion, appears to contain a simple or obvious mistake or oversight, and the assessment merely corrects the mistake or oversight.

- This exception is intended to apply to a simple calculation error or oversight that Inland Revenue's Processing Centres generally discover with computer edits and simple return checks. This maintains the status quo for the many assessments arising in this situation.

- The Commissioner will generally treat the following as a simple mistake or oversight:

- an arithmetical error;

- an error in transposing numbers from one box to another in a tax return;

- double counting, such as inadvertently including in the taxpayer's income the same item twice;

- not claiming a rebate to which the taxpayer is entitled or that was incorrectly calculated, for example, the low income rebate for a taxpayer.

- A "simple or obvious mistake or oversight" can be determined on a case-by-case basis with no dollar limit. The Commissioner may consider whether this exception applies irrespective of whether the taxpayer has requested that the Commissioner makes an amendment under section 113 or applies the exception under section 89C(b).

- Where the Commissioner issues an assessment to correct a taxpayer's simple or obvious mistake or oversight, the Commissioner may consider imposing shortfall penalties on the taxpayer, if there is a tax shortfall and the taxpayer has committed one of the culpable acts, for example, lack of reasonable care and not relied on the action or advice of their tax advisor for the purposes of section 141A(2B).

Exception 3: Agreement to amend previous tax position

- Section 89C(c) reads:

The assessment corrects a tax position previously taken by the taxpayer in a way or manner agreed by the Commissioner and the taxpayer.

- This situation can occur if the issue is raised by either the Commissioner or the taxpayer. There is no need to issue a NOPA because no dispute arises.

- If the Commissioner proposes the adjustment, this exception cannot apply unless the taxpayer accepts the adjustment. For the purpose of section 89C(c), the agreement between the parties can be oral, but the Commissioner's practice will be to seek written agreement. Section 89C(c) applies if Inland Revenue officers can demonstrate that the Commissioner and taxpayer have agreed on the proposed adjustment.

- However, if the parties agree on only one adjustment and dispute others in respect of the same assessment, the Commissioner cannot issue an assessment on the basis of the agreed adjustment because the tax position is not necessarily correct.

- Where a taxpayer proposes an adjustment outside the disputes process and the Commissioner agrees, for example a taxpayer makes a request to amend an assessment, the particulars must be recorded in writing and state that the assessment is made in accordance with the Commissioner's practice on exercising the discretion under section 113. (See SPS 07/03: Requests to amend assessments.) The Commissioner must also consider if shortfall penalties are applicable.

Exception 4: The assessment otherwise reflects an agreement

- Section 89C(d) reads:

The assessment reflects an agreement reached between the Commissioner and the taxpayer.

- The same procedures apply for section 89C(c) and (d). However, the agreement that the parties reach does not have to relate to a tax position that the taxpayer has previously taken.

- For example, if the taxpayer has disputed, but now agrees, that they are a "taxpayer" for the purpose of the definition in section YA 1 of the Income Tax Act 2007 ("ITA 2007") and has not provided a tax return. The Commissioner may issue an assessment to the taxpayer under section 89C(d) to reflect this agreement. The Commissioner must also consider whether shortfall penalties are applicable.

- Another example is where, pursuant to section 6A, the Commissioner settles a tax case and disputes process. In such cases, the Commissioner will usually enter into an individual settlement deed and agreed adjustment in writing with the taxpayer to confirm the settlement.

- The Commissioner will then give effect to that settlement deed and agreed adjustment by issuing an assessment to the taxpayer under section 89C(d) without first issuing a NOPA.

Exception 5: Material facts and law identical to court proceeding

- Section 89C(db) reads:

The assessment is made in relation to a matter for which the material facts and relevant law are identical to those for an assessment of the taxpayer for another period that is at the time the subject of court proceedings.

- Pursuant to section 89C(db), the Commissioner can issue an assessment to the taxpayer in relation to the other period that is the subject of court proceedings, without first issuing a NOPA. The Commissioner does not have to follow the disputes process for the same issue in the other period because the matter is before the court to resolve. A dual process towards resolution does not need to be adopted. The Commissioner will also consider whether shortfall penalties are applicable.

- However, a taxpayer who has been issued with an assessment in relation to another period under section 89C(db), can dispute that assessment by issuing a NOPA to the Commissioner under section 89D within the applicable response period.

- Section 89C(db) is intended to reduce compliance costs. Notwithstanding this provision, the Commissioner can elect to issue a NOPA in respect of the other period in order to resolve the dispute through the disputes process.

Exception 6: Revenue protection

- Section 89C(e) reads:

The Commissioner has reasonable grounds to believe a notice may cause the taxpayer or an associated person -

(i) To leave New Zealand; or

(ii) To take steps, in relation to the existence or location of the taxpayer's assets, making it harder for the Commissioner to collect the tax from the taxpayer. - This exception is intended to ensure that the revenue is protected in the relevant circumstances. Section 89C(e) does not require that the taxpayer has physical possession of their assets.

- If Inland Revenue officers apply the exception under section 89C(e), this should be supported by evidence of the "reasonable grounds" relied on (for example, the taxpayer's correspondence with third parties, application to emigrate overseas and any transcripts of interviews with the taxpayer, etc.)

Exception 7: Fraudulent activity

- Section 89C(eb) reads:

The Commissioner has reasonable grounds to believe that the taxpayer has been involved in fraudulent activity.

- Pursuant to section 89C(eb), a taxpayer has been involved in a fraudulent activity if they have:

- engaged or participated in, or been connected with, any fraudulent activity that would have tax consequences for them, and

- acted deliberately with the knowledge that they were acting in breach of their legal obligations and did so without an honest belief that they were so entitled to act.

- If the taxpayer has not been convicted of an offence relating to a fraudulent activity section 89C(eb) can still apply provided that the Commissioner believes on reasonable grounds that the taxpayer has been involved in a fraudulent activity.

- If Inland Revenue officers apply the exception under section 89C(eb), this should be supported by sufficient evidence of the "reasonable grounds" relied on. The evidence does not have to be absolute proof but, merely sufficient to verify the "reasonable grounds".

Exception 8: Vexatious or frivolous

- Section 89C(f) reads:

The assessment corrects a tax position previously taken by a taxpayer that, in the opinion of the Commissioner is, or is the result of, a vexatious or frivolous act of, or vexatious or frivolous failure to act by, the taxpayer.

- If Inland Revenue officers apply this exception, this should be supported by documentation that evidences:

- the action or inaction giving rise to the tax positions previously taken, and

- why that action is considered to be vexatious or frivolous and any shortfall penalties/prosecution consideration. Examples of a tax position taken as result of a vexatious or frivolous act are a tax position that is:

- clearly lacking in substance, for example, where the taxpayer continues to take the same position that has previously been finalised, or

- motivated by the sole purpose of delay.

- Where this exception applies, the Commissioner must also consider the imposition of shortfall penalties in respect of the taxpayer's tax position resulting from a vexatious or frivolous act.

Exception 9: Taxation Review Authority or court determination

- Section 89C(g) reads:

The assessment is made as a result of a direction or determination of a court or the Taxation Review Authority.

- For the purpose of section 89C(g), a direction or determination includes any court or TRA decision that affects the particular taxpayer in relation to a specific tax period and a court decision on a "test case" that applies to the taxpayer irrespective of whether they were a party to the test case.

- The Commissioner must retain a copy of the direction or determination to support the application of this exception. In these circumstances, the Commissioner will endeavour to make an assessment including imposing shortfall penalties, within two weeks after receiving the written direction or determination. However, if the direction or determination relates to a test case the Commissioner can issue an assessment within the period specified under section 89O(5).

Exception 10: "Default assessment"

- Section 89C(h) reads:

The taxpayer has not provided a tax return when and as required by a tax law.

- If section 89C(h) applies because the taxpayer has failed to provide a tax return the Commissioner can make an assessment or amended assessment pursuant to section 106(1) (commonly known as a "default assessment").

- Where a taxpayer seeks to dispute a default assessment through the disputes process, the taxpayer must, within the applicable response period (that is, four months from the date that the default assessment is issued):

- provide a tax return in the prescribed form for the period to which the default assessment relates (pursuant to section 89D(2C) for GST and section 89D(2) for all other tax types) notwithstanding that the tax return will not include the taxpayer's assessment, and

- issue a NOPA to the Commissioner in respect of the default assessment.

- The requirement to provide a tax return in respect of a default assessment made under section 106(1) before issuing a NOPA is an additional requirement of the disputes process. This ensures that the taxpayer has provided the information that is required by the tax law before they are entitled to dispute the assessment.

- If the Commissioner agrees with the taxpayer's NOPA and tax return, the Commissioner will generally amend the default assessment by exercising the discretion under section 113, subject to the statutory time bar in section 108 and any other relevant limitations. However, if the Commissioner does not agree with the taxpayer's tax return and NOPA the Commissioner can decide to not amend the default assessment and issue a NOR instead.

- If a taxpayer cannot provide a NOPA because they are outside the applicable response period to dispute a default assessment or do not want to enter into the disputes process, they must still provide a tax return.

- Although the Commissioner does not have to amend the initial assessment on receipt of the tax return from a defaulting taxpayer, the Commissioner can exercise the discretion to amend under section 113 subject to the time bar in section 108 or 108A and any other relevant limitations on the exercise of that discretion.

- If the Commissioner decides not to exercise the discretion under section 113 the Commissioner can issue a NOPA in respect of the default assessment under section 89B(1) where, for example, new information received from the taxpayer suggests that the default assessment is incorrect.

- The Commissioner is not precluded from further investigating an amended assessment issued on the basis of the taxpayer's tax return and, if necessary, issuing a NOPA to the taxpayer.

Exception 11: Failure to make or account for tax deductions

- Section 89C(i) reads:

The assessment is made following the failure by a taxpayer to withhold or deduct an amount required to be withheld or deducted by a tax law or to account for an amount withheld or deducted in the manner required by a tax law.

- This exception is intended to address a taxpayer's failure to withhold, deduct or account to the Commissioner for an amount of tax including PAYE, schedular payments to non-resident contractors and resident withholding tax ("RWT"). The Commissioner must also consider whether shortfall penalties are applicable.

- The Commissioner may not apply this exception if there is a dispute that involves statutory interpretation (for example, whether a particular item attracts liability for RWT meaning that the taxpayer was required to withhold or deduct RWT) and/or shortfall penalties.

Exception 12: Non-assessed tax return

- Section 89C(j) reads:

The taxpayer is entitled to issue a notice of proposed adjustment in respect of a tax return provided by the taxpayer, and has done so.

- If a taxpayer proposes an adjustment in a NOPA with which the Commissioner agrees, an assessment can be issued without first issuing a NOPA. This exception only applies to an adjustment that the taxpayer has proposed in their NOPA under section 89DA(1) within the applicable response period.

Exception 13: Consequential adjustment

- Section 89C(k) reads:

The assessment corrects a tax position taken by the taxpayer or an associated person as a consequence or result of an incorrect tax position taken by another taxpayer, and, at the time the Commissioner makes the assessment, the Commissioner has made, or is able to make, an assessment for that other taxpayer for the correct amount of tax payable by that other taxpayer...

- If transactions affect multiple taxpayers, whether in the same way or in related but opposite ways, the Commissioner can reassess any consequentially affected taxpayers under section 89C(k). This is notwithstanding that the consequentially affected taxpayers have not agreed to the amended assessments.

- However, those taxpayers subject to the amended assessments may still issue a NOPA to dispute the consequential adjustment within the applicable response period. The Commissioner must also consider whether shortfall penalties are applicable.

- Section 109(b) deems any assessment that the Commissioner makes to be correct. Therefore, the Commissioner can make any consequential amendment under section 89C(k). However, the Commissioner must be satisfied that there is a direct consequential link between the taxpayers before making any adjustment. For example:

- Group loss offsets: if a loss company has claimed losses to which it is not entitled and the Commissioner has amended the loss company's loss assessment to disallow those losses, pursuant to section 89C(k), the Commissioner can also make a separate assessment for the profit company that had offset the loss company's losses against its profits.

- GST: the supplier and recipient of a supply have incorrectly assumed that a transaction was GST-exempt. The Commissioner later agrees that the recipient was entitled to a GST input tax credit and issues an assessment to them allowing the credit. The Commissioner can also issue an assessment to the supplier under section 89C(k) in respect of the output tax on the value of the supply.

A taxpayer can dispute an assessment that is issued without a NOPA

- The Commissioner can issue an assessment without first issuing a NOPA under section 89C in the circumstances outlined above. Although the Commissioner must always endeavour to apply the exceptions under section 89C correctly, any assessment made in breach of section 89C will still be treated as valid under section 114(a).

- Where the Commissioner issues an assessment without first issuing a NOPA, the taxpayer can dispute the assessment through the disputes process under section 89D(1). (See SPS 10/05: Disputes resolution process commenced by a taxpayer or any replacement SPS.)

- However, where the Commissioner issues a NOPA to a taxpayer and they accept the proposed adjustment by written agreement or are deemed to have accepted the proposed adjustment, then section 89I(1) precludes the taxpayer from challenging the assessment.

- However, section 89I cannot apply if the Commissioner and taxpayer have agreed on an adjustment before entering into the disputes process. The parties can dispute the amended assessment, notwithstanding the previous agreement.

When the Commissioner can issue a NOPA

- Section 89B specifies when the Commissioner can issue a NOPA.

- Under section 89B(1) the Commissioner can issue one NOPA for multiple issues, tax types and periods. Alternatively, the Commissioner can issue multiple NOPAs for the same issue and period, consistent with the obligation to correctly make an assessment within the four-year statutory time period.

- An investigation will have been substantially completed, the facts ascertained, and the proposed adjustment identified and discussed with the taxpayer before a formal NOPA is issued. The Commissioner may actively use his powers to require production of documents in order to ensure that a sustainable position can be taken in the NOPA. The NOPA will also have been quality checked by the Legal and Technical Services.

- A NOPA is not an assessment. It is an initiating action that allows open and full communication between the parties. If possible, the taxpayer will be given the opportunity to settle a dispute by entering into an agreed adjustment with Inland Revenue before the Commissioner issues a NOPA.

- However, the Commissioner or taxpayer is not precluded from issuing a NOPA in respect of any amended assessment that the Commissioner has previously issued to reflect the agreed adjustment.

- A NOPA forms a basis for ensuring that the Commissioner does not issue an assessment without some formal and structured dialogue with the taxpayer in respect of the grounds upon which the Commissioner will issue any assessment or amended assessment (McIlraith v CIR (2007) 23 NZTC 21,456).

- Once an investigation has commenced, the intended approach must be discussed with the taxpayer. If the Commissioner decides to issue a NOPA, the responsible officer will endeavour to advise the taxpayer at least five working days before the date that the NOPA is issued. This is to allow the taxpayer time to consider their position and/or seek advice. However, the taxpayer can also be advised earlier.

- The Commissioner will endeavour to ensure that any issues relating to the same period and tax type are kept together in the dispute.

- The Commissioner can also exercise certain statutory powers (for example, issuing a section 17 notice) after a dispute has commenced and will continue to investigate the facts that relate to the dispute.

- If the parties agree upon some and dispute other proposed adjustments for the same tax period and type, the Commissioner cannot issue an assessment that reflects any agreed adjustment already accepted under section 89J(1) until all the remaining disputed issues are resolved (even if the Commissioner does not pursue the disputed issue further) or determined by the Adjudication Unit. That is, the Commissioner will not issue a "partial" or "interim" assessment under section 89J(1) if the Commissioner is not satisfied that the assessment is correct.

- However, where the statutory time bar is about to fall due, the Commissioner can issue an assessment to reflect both the agreed and disputed adjustment, provided that the requirements of section 89N are met. (See paragraphs 152 to 195 for further discussion).

- Where it is practicable, Inland Revenue officers will contact the taxpayer or their tax agent within 10 working days after the NOPA is issued to ensure that it has been received. Inland Revenue officers making written contact should comply with section 14.

Exceptions to the statutory time bar

Time bar waivers

- If it is contemplated that the disputes process cannot be completed before the statutory time bar period for amending an assessment commences, the parties can agree in writing pursuant to section 108B(1)(a) to waive the time bar by up to 12 months to enable the full disputes process to be applied.

- The taxpayer can also give written notice to the Commissioner and waive the time bar for a further six months after the end of the 12-month period under section 108B(1)(b) to allow sufficient time for the dispute to progress through the adjudication process. This notice must be given to the Commissioner within the initial 12-month period.

- If the time bar is waived, the taxpayer must be advised in writing that:

- a NOPA will be issued, and

- the disputes process will be followed.

- To be effective, a statutory time bar waiver must be agreed in writing on the prescribed form (IR775 Notice of waiver of time bar) and delivered to the Commissioner before the relevant four-year period expires.

- The statutory time bar waiver only applies to those issues that the parties have identified and understood before the initial statutory time bar. Other issues not so identified will still be subject to the original statutory time bar, unless section 108(2) or 108A(3) applies. (See paragraph 110 in this SPS.)

The Commissioner's application to the High Court under section 89N(3)

- If a NOPA has been issued and the disputes process cannot be completed before the statutory time bar period expires, the Commissioner can apply to the High Court for more time to complete the process. (See the discussion regarding section 89N(3) in paragraphs 182 to 193)

- However, where the Adjudication Unit has insufficient time (that is, before the statutory time bar arises or further time allowed under section 108B(1) to fully consider a matter submitted to it expires) the matter will be returned to the responsible officer to decide whether to issue an assessment or amended assessment or to accept the taxpayer's position. Section 89N(2)(b) allows the Commissioner to amend an assessment at any time after the Commissioner has considered the taxpayer's SOP in relation to the particular period. (See paragraphs 318 to 320 for further discussion).

Exceptions under section 89N(1)

- When a NOPA has been issued, the Commissioner will follow the disputes process unless an exception under section 89N applies. (The application of section 89N is discussed in detail later in paragraphs 151 to 192) The Commissioner must obtain and document administrative approval for any departure from the full disputes process.

Limitations on the Commissioner issuing a NOPA

- Under section 89B(4), the Commissioner cannot issue a NOPA:

- if the proposed adjustment is the subject of challenge proceedings, or

- after the statutory time bar has expired.

- The time bar that arises under sections 108 and 108A prevents the Commissioner from issuing an assessment that increases the amount assessed. The Commissioner can still issue an assessment that decreases the amount of the initial assessment subject to the limitation on refunding overpaid tax under sections RM 2(1) of the ITA 2007 and 45(1) of the Goods and Services Tax Act 1985.

- However, the Commissioner is not subject to the statutory time bar that arises under sections 108 and 108A, if the Commissioner considers that the taxpayer has:

- provided a fraudulent or wilfully misleading tax return (section 108(2)(a)), or

- omitted income for which a tax return must be provided that is of a particular nature or source (section 108(2)(b)), or

- knowingly or fraudulently failed to make a full and true disclosure of the material facts necessary to determine their GST payable (section 108A(3)).

- Furthermore, the Commissioner is not subject to the statutory time bar that arises under section 108 if a taxpayer has a remaining tax credit to which section LA 6(1) of the ITA 2007 applies and the Commissioner seeks to amend an assessment or determination to give effect to section LA 6(3) of the ITA 2007 (section 108(3B)).

- When considering whether the exception under section 108(2)(b) applies, the Commissioner will disregard omissions of relatively small amounts of income by applying the principle of de minimis non curat lex (Babington v C of IR [1957] NZLR 861).

- The Commissioner accepts that the time bar ensures finality in relation to assessments, is a key protection for most taxpayers and the exclusions from its protection must be only invoked where there is an adequate basis in fact and law to support their operation. Section 89B(4)(b) requires that the Commissioner initially decides whether an exception to the time bar applies, for example, whether a tax return is fraudulent or wilfully misleading, before determining whether a NOPA can be issued under section 89B(1).

- Any opinion that the Commissioner forms regarding the application of the exceptions to the time bar must be honestly held and reasonably justifiable on the basis of the evidence available and the relevant law. The decision must be clearly documented and include reference to the grounds and reasoning on which it is based.

- Any decision to examine a particular period (which would otherwise be time barred) on the basis that section 108(2)(a), 108(2)(b) or section 108A(3) may apply, is not, in itself, a disputable decision. Nor is any decision that is made under section 108A, in itself, a disputable decision.

- Any NOPA where the CIR is proposing an adjustment on the basis that the exception to the time bar in either 108(2)(a), 108(2)(b) or section 108A(3) applies will set out the reasons why the CIR does not consider that the time bar applies.

- The Commissioner is generally limited to a four-year period within which a taxpayer's assessment can be increased following an investigation or in certain other circumstances. In respect of a dispute, the assessment is amended (if necessary) after the disputes process is completed. The Commissioner will endeavour to undertake the various steps involved in the process within the four-year period.

- Section 89B(4)(a) applies to individual proposed adjustments. Where the proposed adjustment is the subject of court proceedings, the Commissioner cannot issue a NOPA in respect of those proposed adjustments. However, the Commissioner can issue a separate NOPA to the taxpayer in relation to the same tax period provided it relates to a different adjustment.

- For example, a taxpayer challenges the deductibility of feasibility expenditure in the 2009 tax year pursuant to section 138B. The Commissioner can also issue a NOPA to the same taxpayer in relation to the tax treatment of a bad debt in the same tax year.

Contents of the Commissioners NOPA

- A NOPA is the document that commences the disputes process. It is intended to identify the points of contention and explain the legal or technical aspects of the issuer's position in relation to the proposed adjustment in a formal and understandable manner. This will ensure that information relevant to the dispute is quickly made available to the parties. Section 89F(1) and (2) specifies the content requirements for any NOPA that the Commissioner may issue.

- Under section 89F(1)(b), the NOPA must be in the prescribed form (IR770 Notice of proposed adjustment). Any NOPA that the Commissioner issues must identify in sufficient detail the adjustment proposed and explain concisely the facts and law that relate to the adjustment and how the law applies to the facts. When preparing a NOPA the Commissioner will endeavour to avoid repeating facts, arguments or using unnecessary detail.

- Section 89F(2)(b) requires that the NOPA states the key facts and law concisely and in sufficient detail. The Commissioner must ensure that the document is relatively brief and simple to enable the parties to quickly progress the dispute without incurring substantial expenses or excessive preparation time but also detailed enough to explain all the issues relevant to the dispute. The Commissioner's NOPAs should be concise, accurate, coherent and logically presented. In preparing a NOPA Inland Revenue officers should avoid unnecessarily using legalistic language.

- The Commissioner should identify (but not reproduce in full) the relevant legislation and legal principles derived from leading cases. These references should be in sufficient detail to clarify the grounds for the proposed adjustment. However, lengthy quotations from cases should be avoided.

- The Commissioner has a statutory obligation to inform a taxpayer adequately, but it is recognised that the matters relevant to the dispute will be set out in greater detail at the SOP phase if the dispute is not resolved.

- Therefore, what is included in a NOPA or NOR is not conclusive as between the parties because they can introduce further grounds or information or adjust the quantum of the proposed adjustments later in the disputes process (CIR v Zentrum Holdings Limited (2006) 22 NZTC 19,912). However, the parties cannot propose another adjustment involving new grounds and a fresh liability at the SOP phase.

- The Commissioner must always endeavour to issue a NOPA that has sufficient details, is of a high standard and has been considered by Legal and Technical Services. The Commissioner must endeavour to advise the taxpayer during the conference phase of any new grounds, information or reduction in quantum that will be introduced in the SOP.

- If the Commissioner decides to increase the quantum of any proposed adjustment after the NOPA is issued the Commissioner must issue a new NOPA to the taxpayer.

- Although candid and complete exchanges of information are implicit in the spirit and intent of the disputes process, the Commissioner's practice will be to ensure that the NOPA is, within those limits, as brief as practicable.

- The content of any NOPA that the Commissioner issues must satisfy all the requirements specified in section 89F(2)(a) to (c).

Identify adjustments or proposed adjustments - section 89F(2)(a)

- The Commissioner must consider in respect of each proposed adjustment:

- the income amount or impact of the adjustment, and

- the tax year or period to which the proposed adjustment relates, and

- whether use of money interest will apply.

- The Commissioner will also consider whether shortfall penalties and/or other appropriate penalties of lesser percentages apply. That is, where sufficient evidence is held to support the imposition of the penalties and this can be justified (by reference to any relevant guidelines.)

Shortfall penalties

- Shortfall penalties are separate items of adjustment that must be explained and supported in the same manner as the underlying tax shortfall. Section 94A(2) also requires that shortfall penalties must be assessed the same way as the underlying tax. Even though assessments of shortfall penalties relate to the underlying tax they are not subject to the time bars that arise under section 108 or 108A.

- Where there is sufficient evidence to suggest that shortfall penalties should be imposed, the relevant Inland Revenue officer must ensure that the shortfall penalties are proposed in the same NOPA as the substantive issues. However, the officer can dispense with this practice if any of the following exceptions apply:

- The evidence supporting the imposition of shortfall penalties does not become available until after the Commissioner has issued the NOPA on the substantive issues. In such circumstances, a separate NOPA may be issued in respect of the shortfall penalties at a later stage.

- Before entering into the disputes process, a taxpayer has accepted the proposed adjustment in relation to the substantive issues, but not accepted the imposition of the shortfall penalties. In this circumstance, the Commissioner may still issue a NOPA to the taxpayer for the proposed penalties.

- The taxpayer makes a voluntary disclosure of the substantive issues to the Commissioner and the only disputed issue relates to the imposition of the shortfall penalties.

- Prosecution action is being considered and shortfall penalties also apply because the taxpayer has committed one of the culpable acts (for example, evasion), in most instances the Commissioner must first complete any prosecution action against the taxpayer before the shortfall penalties can be imposed.

- Pursuant to section 149(5), if shortfall penalties have been imposed the Commissioner cannot subsequently prosecute the taxpayer for taking the incorrect tax position unless the shortfall penalties are imposed under section 141ED. Therefore, the Commissioner may omit proposing shortfall penalties in a NOPA if prosecution is being considered as an option. The Commissioner must issue a new NOPA in respect of any shortfall penalties that are to be imposed after the prosecution.

- Furthermore, the Commissioner cannot propose shortfall penalties at the SOP phase if they were not previously proposed in a Commissioner's NOPA.

State the facts and law - section 89F(2)(b)

Facts

- To provide a concise statement of facts, the Commissioner must focus on the material factual matters relevant to the legal issues. This includes, for each proposed adjustment, the facts relevant to proving all arguments made in support of the adjustment including any facts that are inconsistent with any arguments that the taxpayer has previously raised.

- The Commissioner should endeavour to state all the material facts in brief, so as to avoid irrelevant detail or repetition. For example, where the parties both know the background to the disputed issues, a summary of the facts in the NOPA will suffice. Where possible, the Commissioner will refer to and/or append any documents that have previously set out the facts on which the Commissioner relies.

- Although the Commissioner will make every attempt to be concise in the NOPA, the Commissioner considers that the explanation of the material facts should be relative to the complexity of the issues.

Law

- Under section 89F(2)(b) the Commissioner must state the law concisely by including an outline of the relevant legislative provisions and principles derived from leading cases that affect the proposed adjustment.

- It is sufficient that the Commissioner explains the nature of the legal arguments without providing lengthy quotations from the relevant case law.

How the law applies to the facts - section 89F(2)(c)

- The Commissioner must apply the legal arguments to the facts to ensure that the proposed adjustment is not a statement that appears out of context. The application of the law to the facts must be stated concisely and logically support the proposed adjustment.

- The Commissioner must outline all relevant materials and arguments (including alternative arguments) on which the Commissioner intends to rely. If more than one argument supports the same or a similar outcome, the NOPA must include all the arguments.

- The evidence exclusion rule under section 138G(1) does not apply to the issues, facts, evidence and propositions of law that are raised in the Commissioner's NOPA. That is, the Commissioner is not restricted to raising the same issues, facts, evidence and propositions of law that are specified in the NOPA at the SOP phase or in challenge proceedings that the taxpayer has commenced where a disclosure notice has not been issued.

Size and length of Commissioner's NOPAs

General guidelines

- The length of a Commissioner's NOPA will necessarily vary from case to case. The maximum length of a Commissioner's NOPA is administratively capped at 30 pages. The 30-page limit excludes any discussion on shortfall penalties (if included in the same Commissioner's NOPA as the substantive issues), the last page of instructions on "What to do next", and schedules that show complicated calculations and diagrams. The application of the 30-page limit is subject to the following further restrictions:

- For disputes involving less than $5,000 of tax (excluding evasion and tax avoidance issues), the Commissioner's NOPA should not exceed five pages.

- Where the dispute concerns one issue only (for example, the imposition of shortfall penalties), the Commissioner's NOPA should not exceed ten pages.

- A longer Commissioner's NOPA may be appropriate, where the dispute concerns multiple issues or the issue is very complex and involves a substantial amount of tax.

- The Commissioner will strive to keep NOPAs as short as possible, but this will be balanced with the need to achieve the objective of issuing the NOPA, (ie sufficiently communicating to the recipient the proposed adjustments and the reasons for them). Inland Revenue officers are required to get approval before a Commissioner's NOPA can exceed the 30-page limit.

- Wherever practicable, all adjustments proposed for a particular taxpayer should be included in one NOPA. However, where new issues arise during the disputes process, the Commissioner is not precluded from commencing separate disputes for these new issues. If the parties are still in dispute after the conference phase, the proposed adjustments in multiple NOPAs may, subject to the taxpayer's agreement, be combined into one SOP. Combining multiple issues into one dispute has the benefit of reducing compliance costs and should reduce the time taken in the disputes process.

Timeframes to complete the disputes process

- If the Commissioner has commenced the disputes process by issuing a NOPA and the dispute remains unresolved, where practicable, the responsible officer must negotiate a timeframe with the taxpayer to ensure that the dispute is progressed in a timely and efficient way.

- Although not statutorily required, agreeing to a timeframe is a critical administrative requirement that requires both parties to be ready to progress the dispute in a timely manner. The parties should endeavour to meet the agreed timeframe. Where there are delays in the progress of the dispute the responsible officer will manage the delay including any relationship with internal advisers and liaise with the taxpayer.

- If the negotiated timeframe cannot be achieved, the responsible officer will enter into a continuing discussion with the taxpayer to either arrange a new timeframe or otherwise keep them advised of when the disclosure notice and SOP will be issued. This is consistent with the purpose of the disputes process which is to promote the prompt and efficient resolution of disputes. Therefore, the failure to negotiate or adhere to an agreed timeframe will not prevent a case from progressing through the disputes process in a timely manner.

- In addition to the above administrative practice, the Commissioner is bound by section 89N(2). Under that provision, if a NOPA has been issued and the parties cannot agree on the proposed adjustment, the Commissioner cannot amend an assessment without completing the disputes process unless any of the exceptions in section 89N(1)(c) apply. These exceptions are explained in paragraphs 152 to 193. If any of these exceptions apply the disputes process will end and the dispute will not go through the adjudication phase.

Section 89N - exceptions - when an assessment can be issued without completing the disputes process

- If a NOPA has been issued and the dispute is unresolved, the Commissioner can issue an assessment without completing the disputes process under the following circumstances:

Exception 1: In the course of the dispute, the Commissioner considers that the taxpayer has committed an offence under an Inland Revenue Act that has had the effect of delaying the completion of the disputes process (section 89N(1)(c)(i)).

- Section 89N(1)(c)(i) reads:

(i) the Commissioner notifies the disputant that, in the Commissioner's opinion, the disputant in the course of the dispute has committed an offence under an Inland Revenue Act that has had an effect of delaying the completion of the disputes process:

- This exception applies where the Commissioner may need to act quickly to issue an assessment because it is considered that the taxpayer has committed an offence under an Inland Revenue Act that has caused undue delay to the progress of the dispute.

- For example, in the course of a dispute a taxpayer obstructed Inland Revenue officers in obtaining information from the taxpayer's business premise under section 16. The Commissioner will advise the taxpayer in writing that it is considered that an offence has been committed under section 143H. The offence has the effect of delaying the completion of the disputes process meaning that the Commissioner does not have to complete that process and can amend the taxpayer's assessment under section 113.

- Another example of when the exception may apply is where, in the course of a dispute, a taxpayer wilfully refuses to attend an enquiry made under section 19 on the date specified in the Commissioner's notice. In these circumstances, the Commissioner will advise the taxpayer in writing that that it is considered that an offence has been committed under section 143F that has had the effect of delaying the completion of the disputes process. The Commissioner can then exercise the discretion to amend the taxpayer's assessment under section 113 without completing the disputes process.

- In order to apply this exception, Inland Revenue officers must form an opinion that is honestly and reasonably justifiable on the basis of the evidence available. The Inland Revenue officer's decision must be clearly documented and stipulate the grounds and reasoning on which it is based.

Exception 2: A taxpayer involved in a dispute, or person associated to them, may take steps to shift, relocate or dispose of the taxpayer's assets to avoid or delay the collection of tax, making the issue of an assessment urgent (section 89N(1)(c)(ii) and (iii)).

- If the Commissioner has reasonable grounds to believe that the taxpayer or a person associated with them ("associated person") intends to dispose of assets in order to avoid or defer the payment of an outstanding or pending tax liability, the Commissioner can urgently issue an assessment to the taxpayer. Section 89N(1)(c)(ii) &(iii) reads:

(ii) The Commissioner has reasonable grounds to believe that the disputant may take steps in relation to the existence or location of the disputant's assets to avoid or delay the collection of tax from the disputant:

(iii) The Commissioner has reasonable grounds to believe that a person who is an associated person of the disputant may take steps in relation to the existence or location of the disputant's assets to avoid or delay the collection of tax from the disputant:

- In order to issue an assessment on the basis of either of the above exceptions, Inland Revenue officers must record any relevant correspondence and evidence (for example, the directors' written instructions to shift the company's assets overseas, evidence of electronic wiring of funds to overseas countries, transcripts of interviews with the taxpayer, etc) or other grounds for the reasonable belief.

Exception 3: The taxpayer involved in a dispute or a person associated with them involved in another dispute involving similar issues has begun judicial review proceedings in relation to the dispute (section 89N(1)(c)(iv) and (v)).

- Section 89N(1)(c)(iv) and (v) reads:

(iv) The disputant has begun judicial review proceedings in relation to the dispute:

(v) a person who is an associated person of the disputant and is involved in another dispute with the Commissioner involving similar issues has begun judicial review proceedings in relation to the other dispute:

- These exceptions apply to any judicial review proceedings that are brought against the Commissioner. In judicial review proceedings, the parties' resources are likely to be directed away from advancing the dispute through the disputes process.

- For the purpose of section 89N(1)(c)(v), an associated person of a taxpayer may be involved in a similar issue to the taxpayer even if the issue relates to a different revenue type. For example, if the dispute between the Commissioner and taxpayer relates to PAYE issues, but the dispute between the Commissioner and person associated with the taxpayer relates to income tax the taxpayer may still be involved in similar issues to the person associated with them.

- Even if the two disputes relate to the same revenue type, section 89N(1)(c)(v) will not apply in some circumstances. For example, the dispute with the taxpayer relates to the tax treatment of entertainment expenditure, whereas the dispute with the person associated with the taxpayer relates to the capital and revenue distinction of merger expenditure. The Commissioner would not regard these two disputes as involving similar issues.

Exception 4: The taxpayer fails to comply with a statutory requirement for information relating to the dispute (section 89N(1)(c)(vi)).

- Section 89N(1)(c)(vi) reads:

(vi) During the disputes process, the disputant receives from the Commissioner a requirement under a statute for information relating to the dispute and fails to comply with the requirement within a period that is specified in the requirement:

- Generally, a taxpayer provides information to Inland Revenue voluntarily. However, when this does not occur the Commissioner can seek information from the taxpayer under a statutory provision, for example sections 17 or 19. (The Commissioner's practice regarding section 17 is currently set out in SPS 05/08: Section 17 Notices.) The requirement for statutory information will specify the period within which the information must be provided. This period will allow the taxpayer reasonable and sufficient time to comply.

- Where the taxpayer does not comply with a formal requirement for information that relates to a dispute (for example, as a tactic to delay the progress of the disputes process), the Commissioner can issue an assessment to the taxpayer without first completing the disputes process.

Exception 5: The taxpayer elects to have the dispute heard by the TRA acting in its small claims jurisdiction (section 89N(1)(c)(vii)).

- Section 89N(1)(c)(vii) reads:

(vii) the disputant elects under section 89E to have the dispute heard by a TRA acting in its small claims jurisdiction:

- A taxpayer can issue a NOPA to the Commissioner under section 89D or 89DA or a NOR rejecting a NOPA issued by the Commissioner under section 89B (See SPS 10/05: Disputes resolution process commenced by a taxpayer and any replacement SPS).

- At the same time, under section 89E(1)(a) the taxpayer can elect in their NOPA or NOR that the TRA acting in its small claims jurisdiction should hear any unresolved dispute arising from the NOPA (whether issued by the Commissioner or taxpayer), if the amount in dispute is $30,000 or less. Any such election is irrevocable, final and binding on the taxpayer. In this case, the full disputes process does not have to be followed.

Exception 6: The parties agree in writing that the dispute should be resolved by the court or TRA without completing the disputes process (section 89N(1)(c)(viii)).

- Section 89N(1)(c)(viii) reads:

(vii) the disputant and the Commissioner agree in writing that they have reached a position in which the dispute would be resolved more efficiently by being submitted to the court or TRA without completion of the disputes process:

- Under this exception, where the Commissioner or taxpayer commences the disputes process, the parties can make such an agreement in writing before either party issues their SOP. This would occur, for example, if the parties could incur excessive compliance and administrative costs in completing the full disputes process relative to the amount in dispute.

- This exception allows the taxpayer to bring challenge proceedings against the Commissioner. The parties must have exchanged a NOPA and NOR before the taxpayer can bring challenge proceedings under section 138B(1).

- The circumstances under which the Commissioner will enter into such an agreement are discussed in detail from paragraph 261 to 285. This SPS refers to this exception as opting out of the disputes process or "opt out".

Exception 7: The parties agree in writing to suspend the disputes process pending the outcome of a test case (section 89N(1)(c)(ix)).

- Section 89N(1)(c)(ix) reads:

(ix) the disputant and the Commissioner agree in writing to suspend proceedings in the dispute pending a decision in a test case referred to in section 89O.

- Section 89O(2) allows a dispute to be suspended pending the result of a test case. Pursuant to section 89O(3), the parties can agree in writing to suspend the dispute from the date of the agreement until the earliest date that:

- the court's decision is made, or

- the test case is otherwise resolved, or

- the dispute is otherwise resolved.

- If the parties agree to suspend the disputes process, any statutory time bar affecting the dispute is stayed. The Commissioner can then make an assessment that is consistent with the test case decision. (However, the taxpayer is not precluded from challenging the Commissioner's assessment under section 89D(1), even if it is consistent with the test case decision.)

- The Commissioner must issue an amended assessment or perform an action within the time limit specified in section 89O(5).

- Section 89O(5) reads:

The Commissioner must make an amended assessment, or perform an action, that is the subject of a suspended dispute by the later of the following:

(a) the day that is 60 days after the last day of the suspension:

(b) the last day of the period that -

(i) begins on the day following the day by which the Commissioner, in the absence of the suspension, would be required under the Inland Revenue Acts to make the amended assessment, or perform the action; and

(ii) contains the same number of days as does the period of the suspension. - If the statutory time bar arising under section 108 or 108A is imminent, section 89O(5) allows the Commissioner more time to complete the disputes process.

- For example, the Commissioner commences a dispute and on 1 March 2010 agrees with the taxpayer in writing to suspend the disputes proceedings pending the decision in a designated test case. The disputed issue is subject to a statutory time bar that commences after 31 March 2010 and the taxpayer does not agree to delay its application under section 108B(1)(a). A decision is reached in the test case on 31 July 2010.

- The Commissioner must make an amended assessment or perform an action that is the subject of the suspended dispute by 29 September 2010. This date is calculated as follows:

- The suspension period commences on the date of the agreement (1 March 2010) and ends on the date of the court's decision in the test case (31 July 2010). This is a period of 153 days.

- The last date that the Commissioner can make an amended assessment falls on the later of the following two dates:

- 29 September 2010, that is 60 days after the date that the suspension period ends on 31 July 2010 pursuant to section 89O(5)(a), and

- 31 August 2010, that is 153 days after the period commences on 1 April 2010 pursuant to section 89O(5)(b).

Exception 8: The Commissioner applies to the High Court for an order to allow more time to complete or dispense with the disputes process.

- Section 89N(3) reads:

... [T]he Commissioner may apply to the High Court for an order that allows more time for the completion of the disputes process, or for an order that completion of the disputes process is not required.

- The Commissioner envisages that this exception will be used if section 89N(1)(c) does not apply and there are exceptional circumstances.

- Any application made by the Commissioner under section 89N(3) must be based on reasonable grounds. Whether there are reasonable grounds will depend on considerations such as the complexity of the issues in the dispute, whether the taxpayer has caused delays; whether the dispute involves large amounts of revenue or whether there were significant matters in the dispute that were unforeseen by either party and provided a justification for the delay.

- For example, due to unusual circumstances the Commissioner does not learn about a proposed adjustment until late. Further delays by the taxpayer and the need for the Commissioner to obtain significant legal advice means that the Adjudication Unit cannot consider the dispute before the time bar applies. In these circumstances, the Commissioner may apply to the High Court for an order that allows more time for the disputes process to be completed under section 89N(3). (Note: This is only an example of a possible unforeseen situation and it is anticipated that there will be a wide variety of circumstances under which an application under section 89N(3) will be appropriate.)

- The Commissioner's application to the High Court under section 89N(3) be made before the four-year statutory time bar falls due.

- The Commissioner must also issue an amended assessment within the time limit specified in section 89N(5). Section 89N(5) reads:

If the Commissioner makes an application under subsection (3), the Commissioner must make an amended assessment by the last day of the period that -

(a) begins on the day following the day by which the Commissioner, in the absence of the suspension, would be required under the Inland Revenue Acts to make the amended assessment; and

(b) contains the total of -(i) the number of days between the date on which the Commissioner files the application in the High Court and the earliest date on which the application is decided by the High Court or the application or dispute is resolved:

(ii) the number of days allowed by an order of a court as a result of the application. - Section 89N(5) allows the Commissioner more time to complete the disputes process where the statutory time bar under section 108 or 108A is imminent.

- For example, the Commissioner commences the disputes process. On 1 March 2010 the Commissioner applies to the High Court under section 89N(3) for an order allowing more time to complete the process. The disputed issue is subject to a statutory time bar that commences after 31 March 2010 and the taxpayer does not agree to delay its application under section 108B(1)(a). On 30 June 2010, the High Court makes an order that allows the Commissioner's application and gives the Commissioner 30 further days to complete the disputes process.

- Pursuant to section 89N(5), the Commissioner must make an amended assessment by 30 August 2010. This date is calculated as follows:

- The Commissioner would have one month to make the amended assessment before the statutory time bar commences. That is, 1 March 2010 to 31 March 2010. The period during which an amended assessment must be made under section 89N(5)(a) commences on 1 April 2010.

- The period during which the assessment must be made includes 122 days, that is the period between 1 March 2010 and 30 June 2010 (the date of the decision) under section 89N(5)(b)(i) and the 30-day period allowed by the High Court order under section 89N(5)(b)(ii). This is a total of 152 days.

- The Commissioner must issue an amended assessment to the taxpayer on the date that is 152 days from 1 April 2010. That is, by 30 August 2010.

- During the period from 1 March to 30 August 2010, the parties may continue to attempt to resolve the dispute. This may include exchanging SOPs and going through the adjudication process.

- The above example indicates that the Commissioner has more time to complete the disputes process. The time bar will not commence until 30 August 2010.

- Where the Commissioner applies to the High Court under section 89N(3) for an order to truncate the disputes process, an assessment must be issued within the period as calculated under section 89N(5). Applying the same facts as in the above example, the Commissioner must issue an assessment to the taxpayer by 30 August 2010.

Application of the exceptions in section 89N(1)(c)

- The Commissioner's practice is that the parties should endeavour to resolve the dispute before or via the adjudication process. If this is not possible and any of the exceptions in section 89N(1)(c) apply the Commissioner can amend an assessment without completing the whole disputes process, that is, before the parties accept a NOPA, NOR or SOP that the other has issued, or the Commissioner has considered the taxpayer's SOP. This will conclude the disputes process and the dispute will not go through the Adjudication phase.

- In this circumstance, the taxpayer can challenge the Commissioner's assessment by filing proceedings in the TRA (either acting in its general or small claims jurisdiction) or the High Court within the applicable response period, that is, within two months starting on the date that the notice of assessment is issued.

Taxpayer's response to the commissioner's NOPA: NOR

- If a taxpayer disagrees with the Commissioner's proposed adjustment, then, under section 89G(1), they must advise the Commissioner that any or all of the proposed adjustments are rejected by issuing a NOR within the two-month response period. That is, within two months starting on the date that the Commissioner's NOPA is issued. The Commissioner interprets this as requiring Inland Revenue's receipt of the NOR within the response period.

- For example, if a NOPA is issued on 9 April 2010, the taxpayer must advise the Commissioner that it is rejected by issuing a NOR to the Commissioner for receipt on or before 8 June 2010. However, taxpayers are encouraged to issue their NOR to the Commissioner once they have completed it.